The end of September saw yet another dismal month of losses for traditional asset classes. U.S. equities, bonds, and nearly every category of risk asset saw considerable losses. By the end of the month, the S&P 500 had notched seven consecutive weeks of declines.

As of this writing, markets had pared back some of these losses, but only time will tell if this sustains. This week aside, the encouraging two-month 17.4% recovery in the S&P 500 from mid-June lows to mid-August highs now seems so long ago. The brief summer respite now looks increasingly like a classic bear-market rally, with the S&P 500 sinking to its lowest level in nearly two years to close out September.

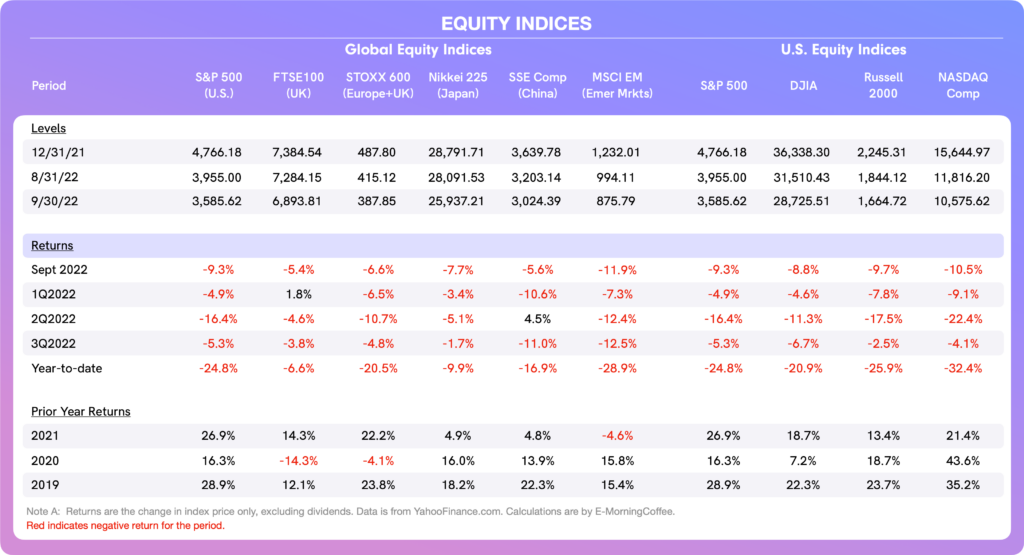

- The S&P 500 saw the third consecutive quarter of declines in 3Q22, bringing the YTD loss in the U.S. benchmark index to 24.8%.

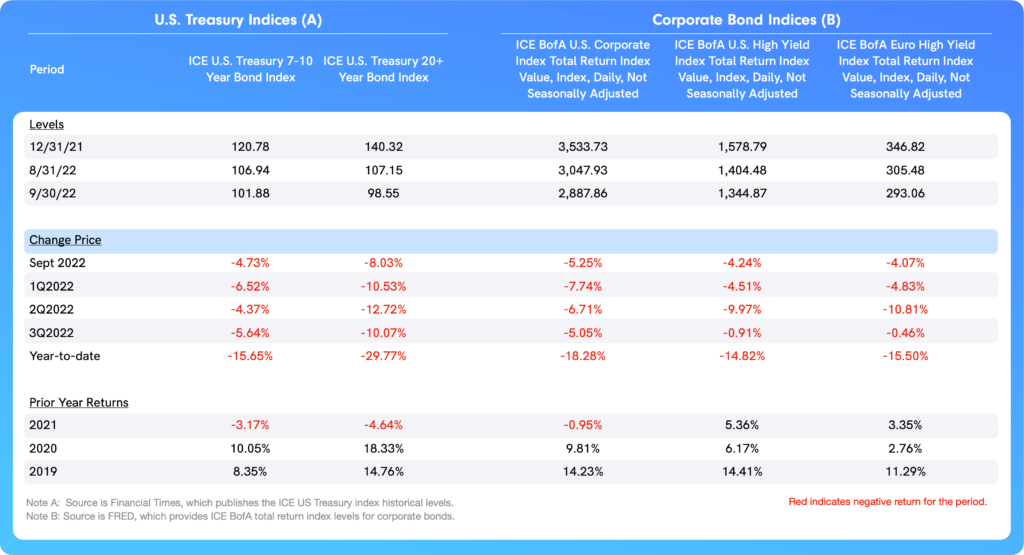

The ICE 20+ Year U.S. Treasury Total Return Bond Index is down a substantial 29.8% YTD, a more painful loss than those in the equities market.

- Corporate bonds had been reasonably stable – and in fact better bid – during the early stages of the recent equity sell-off. Yet both yields and credit spreads in the investment-grade and high yield bond markets began to widen in mid-September, and have not increased by 35bps and 100bps, respectively, since September 12th.

- Credit markets are seen by an increasing number of investors as a key catalyst worth monitoring, as the Federal Reserve is likely to show more concern about credit markets seizing up than about losses in equities.

- The U.S. Dollar strengthened during the month at the expense of most major currencies, including the Euro (month end €0.98/$100) and the Pound ($1.12/£1.00).

Causes of Poor Performance in September

The catalysts and culprits that contributed to poor asset performance in September include, but are not limited to:

- Ongoing and persistent high inflation in the U.S. and other developed economies.

- Federal Reserve (Fed) tightening via higher interest rates, quantitative tightening, and increasingly hawkish rhetoric as it tries to rein in stubbornly high inflation.

- Unsustainable valuations in equities, real estate, and other risk assets, which are slowly deflating.

- A strengthening U.S. Dollar, effectively exporting the U.S.’ inflation, exacerbating issues especially in other Dollar-linked economies (and hurting U.S.-based multinationals).

- The ongoing war in Ukraine, which has contributed to supply-chain disruptions,high energy prices, and heightened geopolitical risk

- A slowing Chinese economy, the world’s second-largest.

- Concerns about upcoming third quarter earnings which start in earnest in mid-October for S&P 500 companies; early indicators from some well-known U.S. companies like FedEx, Apple and Nike have not been encouraging.

Individual Asset Class Performance

Equities: Global stock returns were poor in September, with U.S. equities having the worst return among U.S., U.K., European, and Japanese stocks.

- Emerging market equities had the worst return in September of all indices we track, down 11.9% for the month.

- The more interest-rate sensitive and tech-heavy NASDAQ generated the most negative return of the U.S. equity indices in September, and is now down 35.2% YTD.

Bonds: U.S. Treasuries remain under pressure due to a confluence of factors, some of which may conflict.

- Various Fed officials are repeatedly emphasizing that the bank does not intend to consider a pivot to more dovish policies until inflation is under control. The bombardment of this hawkish rhetoric is a reminder to investors in equities and other risk assets that they should not bet on the proverbial “Fed put” to rescue them as asset prices fall.

- Inflation continues to run hot as various data releases in developed economies indicate. Core Personal Consumption Expenditures (PCE) for August in the U.S. – the Fed’s most-watched inflation indicator – came in red hot this past week, increasing 0.6% month-over-month (Bureau of Economic Analysis report here).

- Stubbornly persistent inflation is pushing short-term yields higher and suggesting a more severe and prolonged series of increases in the Federal Funds rate. At the same time, the fact that inflation might take longer to subdue is pushing intermediate and long-term yields higher, though there is some counter-balancing pressure that a slowing U.S. economy might ultimately cause demand destruction and a weaker U.S. economy.

- The inverted shape of the yield curve reflects the likelihood of a recession, with the 2-10 year yield difference at negative 39bps at the end of September.

- The corporate bond market is also negatively reacting, as yields and credit spreads both moved higher during the second half of September.

Bond Yields: U.S. Treasuries are not the only government bond market under pressure, as government bond yields in the U.K. and Eurozone have also widened significantly.

The U.K., which saw Gilt yields widen significantly, has a unique issue attributable to the recent change of government leadership in the U.K. Chancellor of the Exchequer Kwasi Kwarteng, under new Prime Minister Liz Truss, introduced an expansionary fiscal plan (referred to as a “mini-budget”) that investors deemed inflationary and mis-targeted, working against the objectives of the Bank of England which is tightening monetary policy to bring down inflation.

- In the ensuing days after the plan was announced, investors revolted. Yields on U.K. government bonds (Gilts) skyrocketed and Sterling’s sell-off accelerated, with both spiralling down. With concerns of pension fund losses, the Bank of England stepped in and became a buyer of longer-dated Gilts. Gilt prices have since stabilised and the Pound has strengthened.

Bond Total Returns: Losses on government bonds are continuing to mount as yields increase. U.S. Treasuries experienced negative total returns on the ICE 7-10 year UST index and the ICE 20+ year UST index.

- Returns on corporate bonds were also negative for the month across the investment-grade and high-yield spectrum, caused by both higher yields on underlying U.S. Treasuries and higher credit spreads as risk concerns increased in the market.

It is worth noting that the positive correlation between U.S. equities and U.S. Treasuries is unusual, with both traditional asset classes down sharply during 2022.

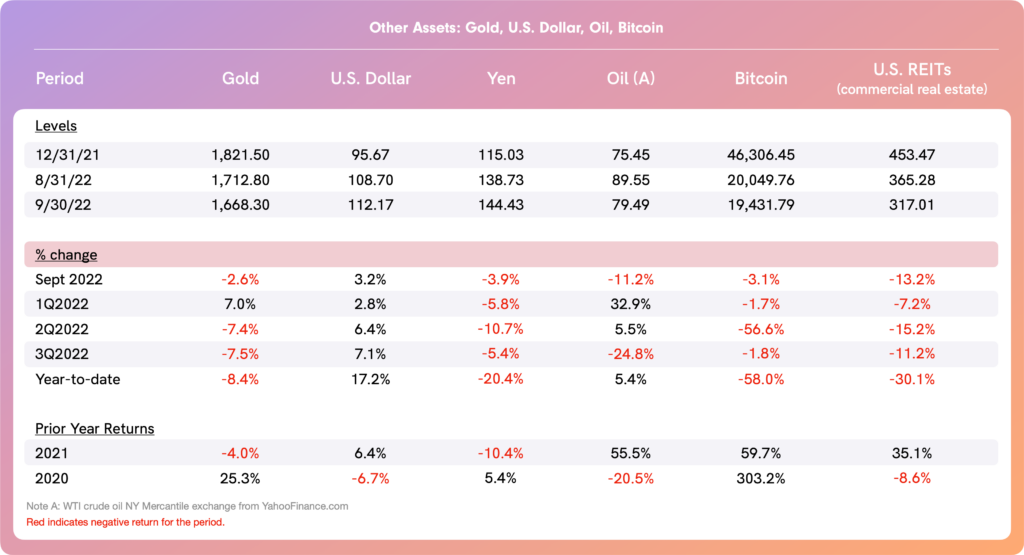

Oil: The price of WTI crude oil continued its decline (which started in mid-July), down 11.2% in September and bringing its 3Q22 loss to 24.8%.

- A new trading range for WTI crude has developed in the $75/bbl to $80/bbl range, and this range could move lower if global economic growth slows as most investors and pundits expect.

- The wild cards are ongoing supply dislocations related to the Ukraine-Russia war and potential reductions in supply quotas by OPEC+. These are difficult to predict, although waning global demand will continue to weigh heavy should global economic growth continue to slow.

U.S. Dollar: The U.S. Dollar index trended higher again in September (+3.2%), making this the fourth consecutive month of a higher USD. The unusually strong U.S. Dollar is claiming victims in other developed economies, including the U.K. (Pound) and the Eurozone (the Euro).

- The currency under the most severe pressure remains the Japanese Yen, which is weaker by 20% vis-à-vis the U.S.Dollar YTD, reflecting the Bank of Japan’s policy to maintain its ultra-dovish policies while western central banks aggressively tighten their monetary policies.

Gold: was down 2.6% in September, extending the YTD losses to 8.4% in an asset class many consider to be the ultimate store of value.

- The case can be made of gold outperforming stocks and bonds this year. Nonetheless, it appears that gold was unable to rally even as market risk concerns increased and inflation remains stubbornly high.

Bitcoin: The price of Bitcoin declined 3.1% in September to end the month at $19,432. While Bitcoin and other digital assets remain one of the worst performing asset classes YTD, this benchmark cryptocurrency held fairly firm during September, generating a better return than both equities and bonds.

- Even so, the total loss on Bitcoin YTD is 58%, more than double the losses of traditional asset classes and significantly worse than the U.S. Dollar (+17.2% YTD) and gold (–8.4% YTD).

Looking Forward

Economic data releases for September are set to release this week. The Bureau of Labor Statistics already announced a 10% drop in job openings month-over-month (July to August), with an increase in the number of hires and 2.8% decline of real earnings. This and other soon-to-be-announced data will be influential as far as investor sentiment. CPI in particular will be a major focus in the U.S., the U.K., and the Eurozone.

- It is expected that the focus will shift to 3Q22 earnings reports of S&P 500 companies, which start being released in the second week of October and continue through early November.

- Expectations about the magnitude of the next series of rate increases and other policy steps by the Federal Reserve, the European Central Bank, and the Bank of England will continue to influence investor sentiment and market performance. The European Central Bank meets in late October, and the Fed and BoE meet the first week of November.

This newsletter was written in partnership with Tim Hall of EMorningCoffee.com. For more insights and other market learnings, subscribe to E-Morning Coffee today.