July was a banner month for traditional financial assets following a horrendous first half of 2022. What’s perhaps most notable is how the month ended with positive momentum when equity markets surged during the last week.

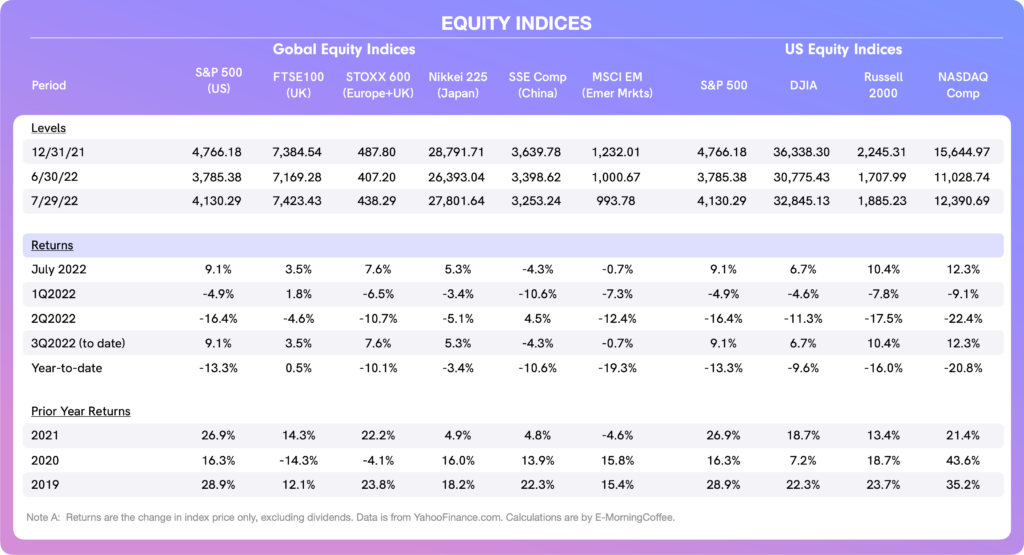

- The S&P 500 turned in a solid performance, gaining 9.1% on the month following a 20.6% decline in the first half of the year.

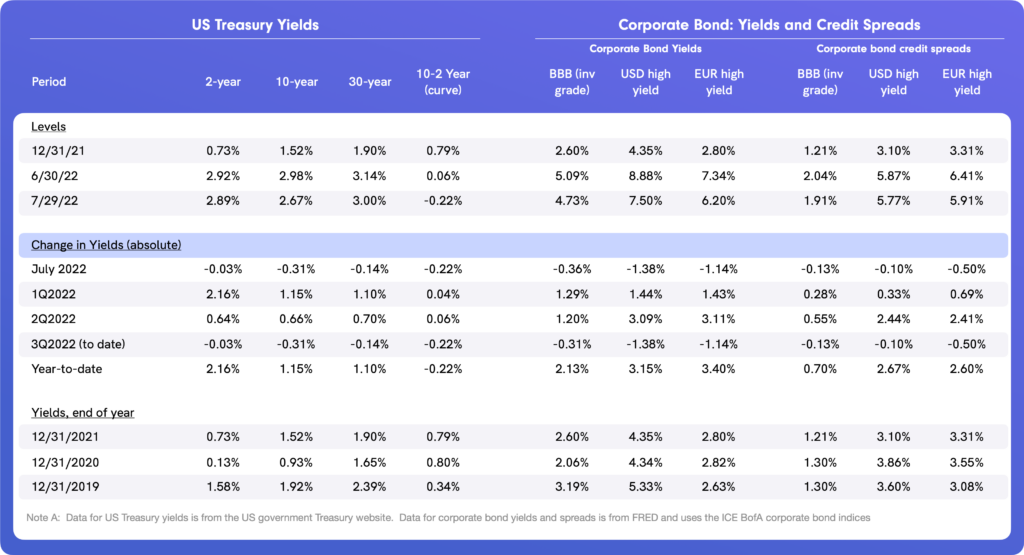

- Equally important, U.S. Treasury yields continued to decline from their June highs, with the yield on the 10-year bond closing the month at 2.67%.

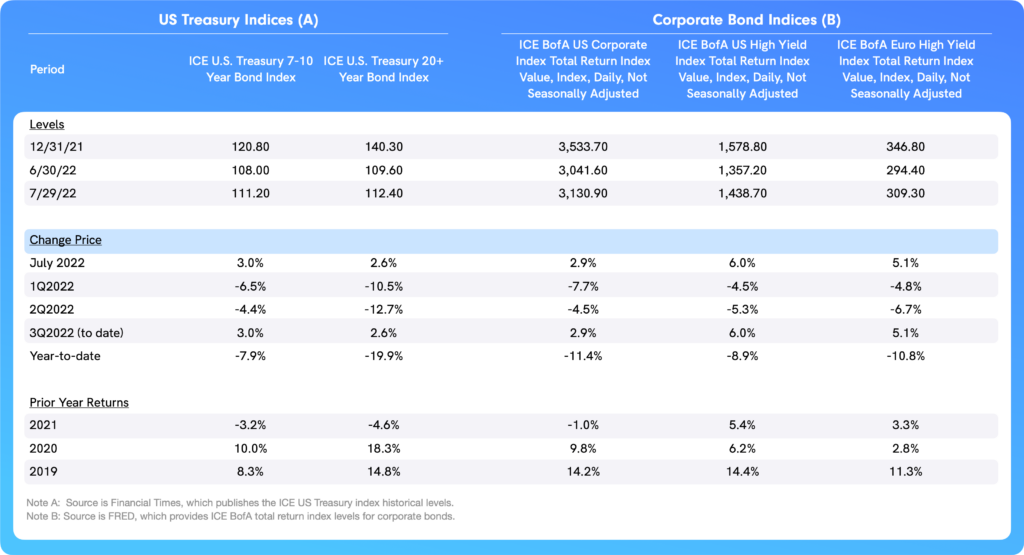

- The ICE 7-10 year UST index returned 3.0%, having lost 10.6% in the first half of 2022.

Recall that the first half of this difficult year saw stock and bond returns positively correlated (and both sharply negative), an unusual circumstance most likely resulting from global economies adjusting to unconventional levels of fiscal and monetary stimulus during the pandemic era.

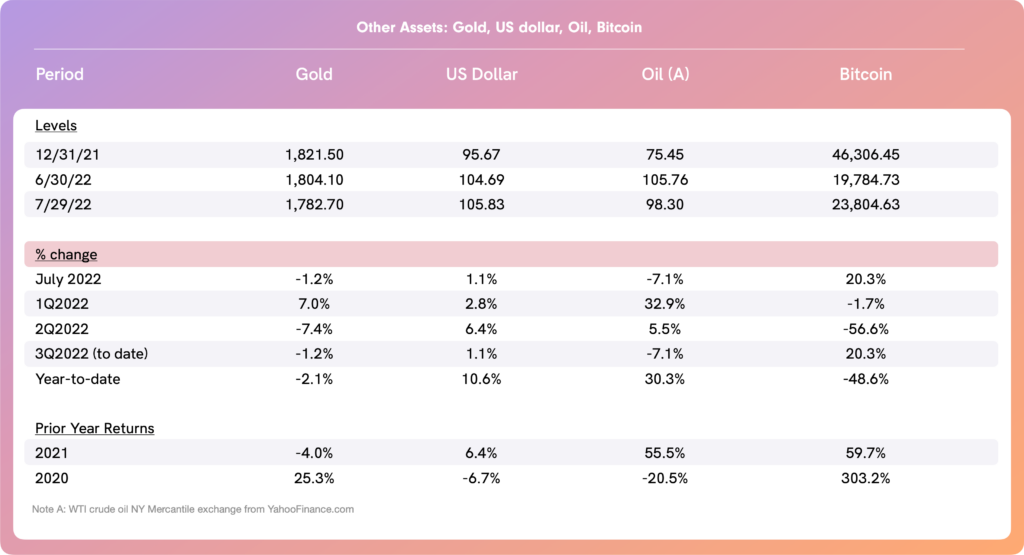

Bitcoin and its cryptocurrency brethren seem to have also bottomed out.

- Bitcoin bounced back in July with a solid return of 20.3% (through July 29th).

- The entire cryptocurrency ecosystem was under significant pressure especially in May and June, as the deleveraging of the sector caused collateral damage with crypto lenders, hedge funds, and brokers.

- There was no significant contagion into other asset classes during this difficult period, and now crypto advocates can (potentially) move forward.

- The price of WTI crude oil also declined in July for the second month running, providing some relief to consumers at the pump and companies dependent on oil or petroleum-derived products. The decline also most certainly brought relief to President Biden, although the effect of lower oil prices has not been visible yet in terms of headline inflation figures.

- The U.S. Dollar also strengthened further, although it has weakened since mid-month.

- A strong U.S. Dollar has all sorts of repercussions for the U.S. and the global economy (mostly negative).

Is it time to celebrate the end of the bear market? Likely not, as it is very difficult to find enough reasons to be optimistic compared to the magnitude of concerns.

- Inflation continues to rage in the U.S., U.K., and Eurozone, with each economic zone showing higher CPI than the month before and no clear signs of abating just yet.

- 2Q22 GDP in the U.S. was confirmed negative for the second consecutive quarter, perhaps not surprising but odd in that the U.S. labor market remains strong — even as the Fed ratchets up its tightening.

- Corporate earnings were at best mixed so far, certainly exposing headwinds like the effects of a strong U.S. Dollar and margin pressure emanating from rapidly increasing costs (especially wages) and supply-chain disruptions.

- The Fed, BoE and ECB are all tightening monetary policy aggressively, as they are stuck between a rock and a hard place with no choice but to focus on taming inflation.

- There has been no significant change as far as the Ukraine-Russia war (though there remains a continued negative influence on energy and food prices).

- Growth in China remains questionable due to periodic COVID shutdowns and potential issues in the property sector, including (but not limited to) supply-chain disruptions, growth of the Chinese economy and domestic consumer demand all under pressure.

Many indicators and factors appear largely the same at the end of June, so one could attribute this unexpected July rally to the fact that expectations were beaten down so much that the simple fact that things have not gotten worse, which could be a good enough reason for investors to become more positive.

- This, in turn, convinced investors to take on more risk and to shift back into traditional financial assets. August will most certainly be a telling month as liquidity lessens, and investors might see more volatile trading sessions as a result.

Asset Class Performance

Equities: All four of the U.S. equity indices we track were positive in July, a welcome break from sharply negative returns in June and in the first half of 2022.

- The tech-heavy, growth-oriented NASDAQ Composite and the value-focused Russell 2000 were the best performers in July.

- Equity returns were also positive in Europe, the U.K., and Japan in July, as investor risk sentiment improved throughout the month.

- The last two weeks of the month had a slew of S&P 500 companies release earnings, including the largest U.S. banks, several large integrated oil companies, and the infamous FAMAG companies. Earnings have been slightly better than analysts’ consensus expectations, although far from outstanding, but good enough for investors.

- Chinese equities, which were positive in June, were negative in July. Economic growth in China has come under increasing scrutiny because of a combination of ongoing sporadic (large) city-lockdowns due to COVID outbreaks and concerns about the Chinese property sector.

- Emerging markets equity returns were also negative, with the strengthening U.S. Dollar creating severe headwinds for many of these countries.

Bond Yields: U.S. Treasury yields in July carried on with the gradual decreases that started in mid-June. These were most pronounced in the intermediate part of the curve.

- The yield on the 10-year U.S. Treasury fell 31bps in July, with the benchmark UST closing the month yielding 2.67%. This is down significantly from the end-of-day yield on June 14th – just six weeks ago – of 3.49%.

- The short end of the curve was more erratic, as the yield on the 2-year UST was as high as 3.25% just 10 days ago, before decreasing during the final one-third of the month to end slightly lower month-over-month, at 2.89%.

- The yield on the 2-year UST moved higher than the yield on the 10-year UST, known commonly as an inversion. This occurred on July 7th, and the inversion deepened and remained throughout the month.

- Many investors view the inversion as a sign that the U.S. economy will slow or even move into a recession in the coming months.

Corporate Bonds: Corporate bond yields and spreads also reversed the trends that had characterized the difficult first half of 2022, recording solid improvement in July as both credit spreads and overall yields moved lower.

- Most of the positive yield migration in corporate bonds— both investment grade and high yield — was due to lower UST yields during July, although credit spreads improved, too — most notably in Euro-denominated high-yield bonds.

Bond Total Returns: Total returns were positive in both U.S. Treasuries and corporate bonds for July.

- July was the first month that the total return on the 20+ year bond index was positive this year, possibly ending a down run for U.S. Treasuries.

- Corporate bonds also had positive returns in July, including both investment grade and high yield (USD- and EUR-denominated).

Oil: The price of WTI crude oil declined 7.1% in July, following a 7.8% decline in June.

- Oil is increasingly signaling that global economic growth will probably slow in the coming months, reducing demand gradually in a market where supply remains fairly tight.

- As mentioned last month, the supply of Russian oil and natural gas, especially for Europe, remains a significant wild card given the ongoing conflict in Ukraine and western sanctions on Russian oil and gas.

U.S. Dollar: The U.S. Dollar soared even higher in the first half of July, peaking at $1.0854/USDX1.00 on July 14th, before easing gradually during the second half of July to end the month at $1.0583/USDX1.00 — a month-over-month increase of 1.1%.

- The U.S. Dollar still remains very strong compared to historical levels. This is creating headwinds for U.S. companies that are exporters and for countries that have their currencies or economic fortunes tied to the U.S. Dollar.

- The strong U.S. Dollar also has a role in the recent price declines in many global commodities which are quoted in U.S. Dollars.

Gold: The price of gold was down 1.2% in July. The decline could have been much worse, but gold rallied 4.9% after reaching its low for the month on July 20th, clawing back what could have been much sharper losses.

Cryptocurrencies: Bitcoin managed to find some stability early in the month, following a difficult period, and rallied during the rest of July, adding 20.3% for the month.

- This return for July was the best of all the assets we track.

- It remains far from clear if the cryptocurrency winter is over for good, although it is apparent that a significant amount of leverage and a large number of speculative investors have been weeded out, creating a more stable foundation should cryptocurrencies be on the cusp of further upside.

Key Sentiment Drivers

Inflation Spikes (and Central Banks Respond): CPI figures for June for the U.S., U.K., and Eurozone were released in early July, and all three showed month-over-month and year-over-year increases. CPI was 9.1% in June, the highest in 40 years. The Federal Reserve announced a 75bps increase in the Federal Funds rate on July 27th, its second 75bps increase in as many months.

- Recall that the Federal Reserve also began a program to reduce its balance sheet in early June (i.e. “quantitative tightening”) as it combats increasing inflation in the U.S.

- Flash CPI in the Eurozone for July was announced on July 29th, coming in at 8.9%. The ECB had acted aggressively a week before the release of the flash July CPI figure, increasing its key overnight bank rate by an unexpectedly large 50bps to 0%.

- This marks the first time that the bank deposit rate has moved out of negative territory in the common currency bloc in eight years.

Earnings: As of the end of July, more than half of S&P 500 companies had reported earnings for the April-June quarter. A number of European companies have also reported their first-half results.

- Earnings in the U.S. kicked off with the large U.S. banks, which were mixed.

- Following the banks, attention turned to the earnings of U.S. technology stocks, both large and small, with the common themes being pressure on advertising revenues as companies (and consumers) curtail their spending, and negative effects of the strong U.S. Dollar. Investors had low expectations following a disappointing round of earnings in the first quarter from the tech giants, so the second quarter results – as mixed as they were – were good enough to spark a slight “relief rally.”

- The global integrated energy companies also reported earnings, and generated record revenues and income.

Overall, the earnings season was not spectacular, but it was good enough especially since expectations have been so beaten down.

Geopolitical Issues: Pressure had been building for many weeks on Boris Johnson, who finally resigned from his position as Prime Minister of the U.K. on July 7th. Conservative party members will vote on Mr Johnson’s replacement in early September.

- There was a second political crisis in Europe in July, with the unexpected resignation of prime minister Mario Draghi in Italy, which was formalized on July 21st. The country is now in the process of trying to form its next government, cobbling together a fractious number of parties into a coalition that can lead the country forward.

U.S. Economic Growth in Q2: The Bureau of Economic Analysis released 2Q2022 GDP for the U.S., and GDP declined 0.9%, the second consecutive quarter of decline.

- 1Q22 GDP was also finalized (third reading), down 1.6% following strong 4Q21 growth. This two-consecutive quarter decline meets the technical definition of a recession, but it’s impossible to reconcile this with such a tight U.S. labor market. (Recall that unemployment in the U.S. is 3.6%.)

- The “recession or no recession” call will ultimately be made by the National Bureau of Economic Research. Personal consumption expenditures on goods fell during the quarter (-4.4%), while expenditures on services increased (+4.1%).

The circumstances of declining (real) GDP and concurrently a tight labor market is a result of highly unconventional pandemic stimulus. The economy might have slowed, but it certainly doesn’t feel like a recession to many.

This newsletter was written in partnership with Tim Hall of EMorningCoffee.com. For more insights and other market learnings, subscribe to E-Morning Coffee today.