How quickly things change! Having started the year with an across-the-board rally in risk assets, February delivered a stark dose of reality to investors. To be fair, the ongoing inflation issue has been at the forefront of investors’ minds in both the U.S. and the Eurozone for many months now. However, periodic reminders that we are facing “tighter monetary policy for longer” are first acknowledged by investors, and then are ignored, with sentiment shifting from euphoria to gloom, back and forth, in a cycle that seems endless at times.

The central bank trifecta – the Federal Reserve, the ECB and the Bank of England – all increased their overnight bank borrowing rates right in line with expectations to begin the month. Naturally, this soothed financial markets even though the risk-on approach that characterized January would soon end. As February progressed, the economic data releases – one after another – were generally stronger than expected, serving as a reminder that the trajectory to lower inflation would neither be fast nor occur in a straight line. To further complicate matters, corporate earnings were mixed. Perhaps even more troubling was the fact that management team after management team was cautious as far as their outlook for the quarters ahead. Markets felt increasingly fragile as the month wore on, ultimately resulting in both bonds and stocks losing ground in February. The combination of strong economic data and persistent inflation suggests that the Federal Reserve and its brethren have a lot more work to do. Upcoming monetary policy meetings for the Fed, the Bank of England and the ECB during the third week of March will be very telling.

February Themes

- The economy: The U.S. economy continues to run hot as evidenced by a slew of economic data released in February, pertaining to January.

- January had a much greater-than-expected increase in non-farm payrolls, with 517,000 new jobs added, and a decline in the unemployment rate to 3.4%1, its lowest level since 1969.

- The United States Census Bureau reported that January retail sales increased 3.0% month over month, having declined 1.1% in December2.

- Strong economic data shows just why inflation is proving more stubborn to tame than had been hoped, certainly by the Federal Reserve.

- Inflation is slowing, but the decline is slower and more sporadic than investors would like.

- Monetary policy: The Federal Open Market Committee (“FOMC”) of the Federal Reserve announced on February 1 that it would increase the Federal Funds rate by 25bps as expected, to a target range of 4.50% to 4.75%3. At the time, investors were “pricing in” two further increases of 25bps, assuming that the Federal Reserve would stop increasing rates as soon as early May (two FOMC meetings forward, one late March and one early May). Two further 25bps increases would result in a terminal Federal Funds rate of 5.00% to 5.25%.

- However, stronger-than-expected economic data and hawkish comments from a variety of Fed officials throughout February have now pushed expectations regarding future rate increases to a higher level for longer.

- Therefore, the oft-discussed “Fed pivot” (meaning when the Fed starts to lower interest rates) is now not expected until at least 2024.

- The Federal Reserve seems fully committed to do what it takes to get inflation back down to its target of 2% per annum, an objective that is stated over and over again, and at times resonates with investors and, at other times, does not.

- Corporate earnings: This cycle of earnings for S&P 500 companies is nearly complete and the results have been mixed. On one hand, earnings and revenue growth have more or less been in line with analysts’ consensus expectations. On the other hand, earnings were not overly encouraging for two reasons.

- Firstly, earnings are expected to be down 3.2% in 4Q22 year-over-year, or 7.4% if the energy sector is excluded4. These are sharp absolute declines in bottom line earnings in 4Q22, even if they were generally in line with expectations.

- Secondly and more concerning, numerous management teams lowered forward guidance during post-earnings calls with analysts, attributing the revisions to economic uncertainty for the quarters ahead. This was a fairly consistent theme, and it raises concerns about the trajectory of future earnings growth, a particularly important factor for equity market valuations.

- Other: China is also being closely watched, although expectations regarding its fast economic recovery following the ending of the country’s “zero-COVID” policies are being revised downward. It is unrealistic to expect China to pick up right where it left off, and the economy continues to have other issues. The ongoing Ukraine-Russia has also been providing noise in the background, with the outcome of this conflict highly unpredictable but very influential in terms of sentiment.

Asset Class Performance

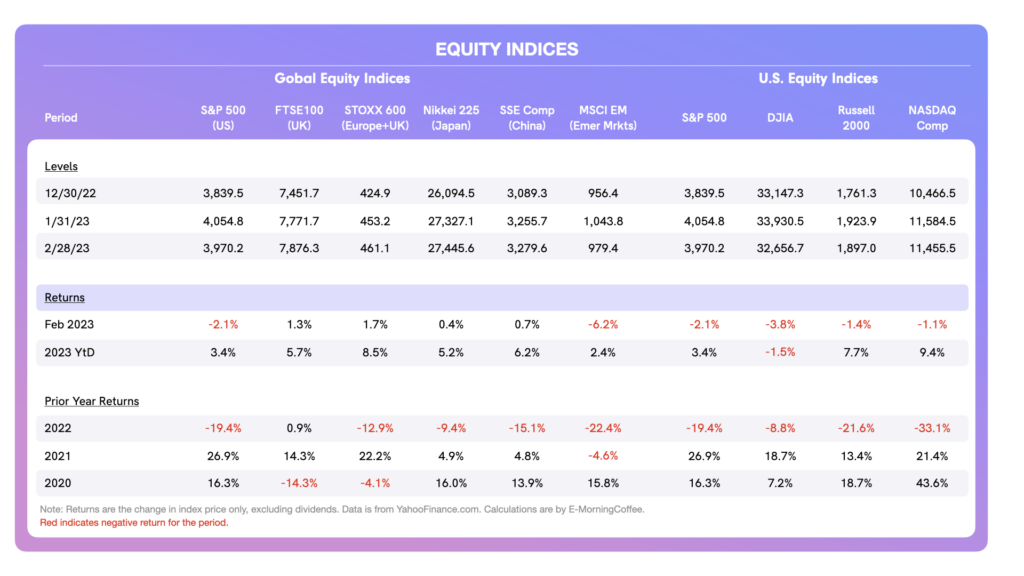

Equities: Aside from U.S. and emerging markets stocks, equity indices in Europe, the U.K., Japan and China were positive in February, although gains were less than they were in January. Performance day-to-day was also more erratic than the month before.

- The best performing equity index YTD is the STOXX 600 (Europe).

- Emerging markets equities were hit the hardest by the stabilization of the U.S. Dollar. The MSCI EM index was down 6.2% in February, sharply reducing its YTD gains.

- All of the U.S. equity indices were red in February, although all managed to hold into YTD gains aside from the large cap DJIA.

- Higher interest rates usually affect the tech-heavy NASDAQ the worst. However, following a remarkable 10.7% increase in the NASDAQ Composite in January, the index was only off 1.1% in February, preserving most of its YTD gains as it remains the top performing U.S. index for this year.

- S&P 500 earnings were mixed but largely in line with analysts’ consensus expectations. Still, earnings were lower YoY, and many companies were very cautious in their outlook for the remainder of 2023. This undermined valuations in U.S. equities.

- The VIX index (measure of market volatility) traded in the 18 to 22 area most of the month, certainly not suggesting any signs of financial market stress.

Bond Yields / Credit Spreads: The U.S. Treasury market took it on the chin in February, not surprising given the string of hot economic data and above-expectations inflation. The reality is that the tightening of monetary policy by the Fed is simply not getting the job done quickly enough.

- The effect across the yield curve was not uniform, with shorter-dated USTs paying the dearest price (as far as higher yields).

- Investors are now pricing in more than the early-February expectation of two more 25bps increases in the Fed Funds rate, as well as a higher terminal rate for longer.

- Although the effect on yields was more perverse at the shorter end of the curve, the yield curve shifted upwards across all maturities causing 2y-10y curve inversion to steepen to -0.89%, its most negative level since August 1981.

- The yield on the 10y UST ended the month at 3.88%, its highest level since early November.

- The Eurozone is facing similar dynamics, with the yield on 2y and 10y German Eurobonds (Eurozone proxy) increasing 55bps and 39bps, respectively, in February.

- Similar to the U.S. Treasury market, the 2y-10y yield difference is negative, meaning the yield curve is inverted in the Eurozone, too.

- In spite of increasing yields and a recognition that inflation will be harder to contain than thought a few weeks ago, the corporate credit markets have continued to show rather remarkable resiliency.

- In fact, although corporate credit yields were higher in February compared to January, corporate credit spreads actually were only slightly wider in investment grade and were slightly tighter in high yield.

- As of the moment, there are no visible signs of stress in the corporate bond market, in spite of tight monetary policy.

Bond Total Returns: U.S. Treasuries and corporate bonds had negative total returns in February following a generally solid performance the month before. Longer-duration bonds were the worst affected by rising yields.

- Return on investment grade corporate bonds were poorer than high yield, because investment grade bonds are more influenced than high-yield bonds by movement in underlying UST yields (which increased sharply during the month).

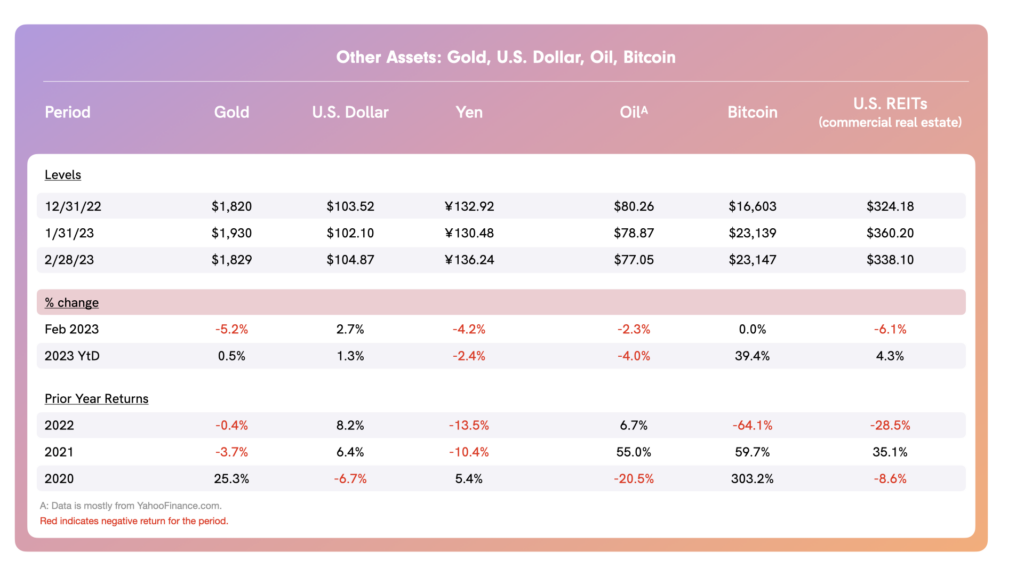

Currencies, Commodities & Alternative Assets: The U.S. Dollar continued to be a focal point in February. Having stabilized in late January, the U.S. Dollar rallied 2.7% in February, reflecting demand coming from a combination of “higher rates for longer” in the U.S. (vs. other countries) and strong economic metrics. The stronger U.S. Dollar hurt emerging markets stocks, and also played a role in lower commodity prices, perhaps most importantly the price of oil.

- WTI crude oil was down again in February, bringing its YTD price decline to 4.0%. Lower oil prices reflect a combination of an easing of supply pressures, a stronger U.S. Dollar, and perhaps anticipated demand destruction as the global economy slows.

- Bitcoin was flat in February, but more importantly held on to its strong January gains, even as risk increased in the market as the month wore on.

March Outlook

With earnings behind us, the focus will be on upcoming economic data releases to determine if tighter monetary policy is having any effect on economic growth. It’s strange because normally, strong economic data would be celebrated. However, with inflation still significantly elevated and proving difficult to subdue, investors associate good economic news as troublesome for the trajectory of future interest rates, in turn making the outlook for stocks and bonds more uncertain. Certainly, all eyes will be focused on the central bank monetary policy meetings the third week of March, as follows:

- Federal Reserve – Mar 21-22

- Bank of England – Mar 23

- ECB – Mar 23

In addition, the Bank of Japan has a policy meeting March 9-10. Expectations are that the pending leadership change at the top of the Bank of Japan in April could usher in a new path of higher interest rates in Japan, assuming that the central bank chooses to better align its monetary policy with that of other developed markets central banks.

About the Author

Tim Hall is a writer, speaker, blogger (emorningcoffee.com), consultant, and advisor. A former banker with 29 years of experience (buy side/sell side), Hall is also a former Independent Non-Executive Director of a U.K. “challenger bank.” He currently resides in London.

1 Data from the Labor Department’s Bureau of Labor Statistics

2 U.S. Census Bureau release of January retail sales

4 From The Week in Earnings/22Q4 | Feb 24, 2023 from I/B/E/S data from Refinitiv