January started 2023 on the right foot across nearly all asset classes as investors shut the door on a poor 2022. Stocks and bonds had positive returns in the first month of the year, with the higher-volatility NASDAQ Composite generating the best return amongst U.S. equity indices. Bonds also performed well, as ongoing uncertainty around inflation seemed to decrease and a more positive narrative seeped into markets. The question will be “is this too much, too fast?” – a question that might be answered in February as economic data trickles in and corporate earnings continue.

January Themes

As the new year started, all eyes were focused on two major things:

- Economic data: Investors were specifically looking for indications that the Federal Reserve might have managed to “thread the needle” as far as tightening monetary policy just enough to curtail record-high inflation without severely undermining the growth of the U.S. economy.

- Corporate earnings: Analysts’ consensus expectations for 4Q22 top- and bottom-line results of S&P 500 companies had been adjusted downward during the last quarter of 2022, reflecting the cocktail of persistently higher inflation (causing pressure on margins), waning growth in China, tight labour markets, and on-going supply chain disruptions.

Economic data released in January (largely related to December) was mixed but was good enough to further diminish fears of an imminent recession as inflation continues to slowly decline.

- Core CPI for December came in at 0.3% month-over-month, and 5.7% year-over-year, the third consecutive month of year-over-year declines in core CPI1.

- At the same time, the employment picture in the U.S. remained solid, suggesting that – at least so far – the Fed’s hawkish policies were not damaging growth too severely. In essence, the US is experiencing a true “Goldilocks” economy – it is neither too hot nor too cold, but just about right.

- On the international stage, the fact that energy prices have fallen more and faster than expected in Europe, mainly because of a winter that has (so far) been relatively warm, has eased concerns of a sharp economic decline in the world’s second largest economy.

- China – the world’s third-largest economy behind the U.S. and E.U. – dropped its “zero-COVID” policy in late 2022, effectively acknowledging the trade-off between COVID deaths and economic growth. A stronger-than-expected Europe and China will inevitably help the US and the global economy as we move through 2023.

As far as corporate earnings, some companies have missed analysts’ guidance, and some have beat consensus expectations. However, the dreaded “way below expectations” fear has not materialized.

- As of January 31, 2023 according to I/B/E/S data from Refinitiv2, 70.3% of the 165 S&P 500 companies that have reported earnings so far have beat analysts’ consensus expectations, compared to a historical average of 66%. This is the good news.

- However, there has been a relatively consistent dose of reality conveyed from the management teams of many companies at post-earnings analyst / investor calls about the uncertain outlook for the quarters ahead.

- Investors seem to have largely dismissed these persistent concerns, pushing the prices of risk assets like stocks higher in spite of the uncertain outlooks. This might change if earnings disappoint and/or the rather consistent message of many management teams about the challenging outlook continues, and then finally begins to resonate in the minds of investors.

January is the start of the calendar investment year, and often, investors will more aggressively try to get positioned and invested to start the year. This – along with the combination of decent economic data and in-line earnings – created a positive backdrop for January.

- As the month moved along, risk markets strengthened. This in turn drew in momentum investors which pushed stocks and bonds higher.

- There is an argument that prices of risk assets are becoming increasingly delinked with what will likely be a choppy road ahead.

- However, it is clear that this has not deterred investors, especially short-term traders chasing “easy” profits.

- It also should serve as a stark reminder as to why investors may want to incorporate alternative assets into their portfolios, which can be significantly less volatile and provide diversification.

Asset Class Performance

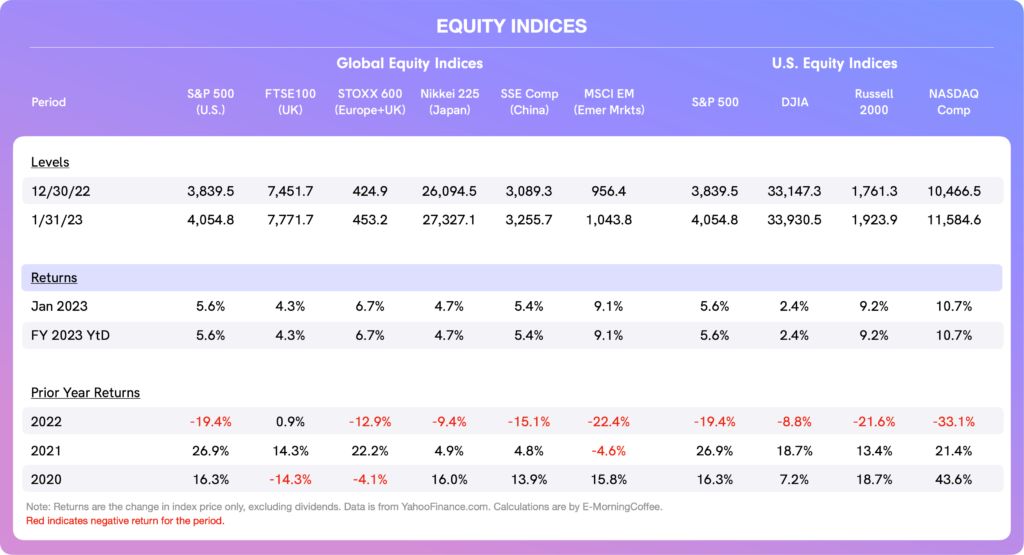

Equities: Encouragingly, January was a strong start to the year for global stocks. In fact, what might be deemed a good start for U.S. equities as measured by the return on the S&P 500 was actually surpassed by even better returns in Europe and the emerging markets, including China.

- Along with the generally favorable sentiment, the further weakening of the U.S. Dollar also provided support, especially for emerging market indices.

- It also appears that Europe might skirt a recession, even though inflation remains a major issue, albeit it is heading in the right direction (down).

- Things are different though in the U.K., the only country we track with a positive stock market performance in 2022 (i.e., the FTSE 100 index). Unlike its G7 brethren, the U.K. is likely to experience a declining economy and on-going high inflation in what will almost certainly be a very challenging year in 2023, although this did not stop solid gains for the FTSE 100 in January.

- The table below illustrates January returns for the global indices and US indices that we track.

- Focusing on the U.S. indices, the NASDAQ Composite – coming off a horrible year in 2022 – gained nearly 10% in January, a terrific start to the year. The NASDAQ tends to be the most inflation-sensitive index, so it was also the biggest beneficiary of lower interest rates as tech shares in particular rallied hard for most of the month.

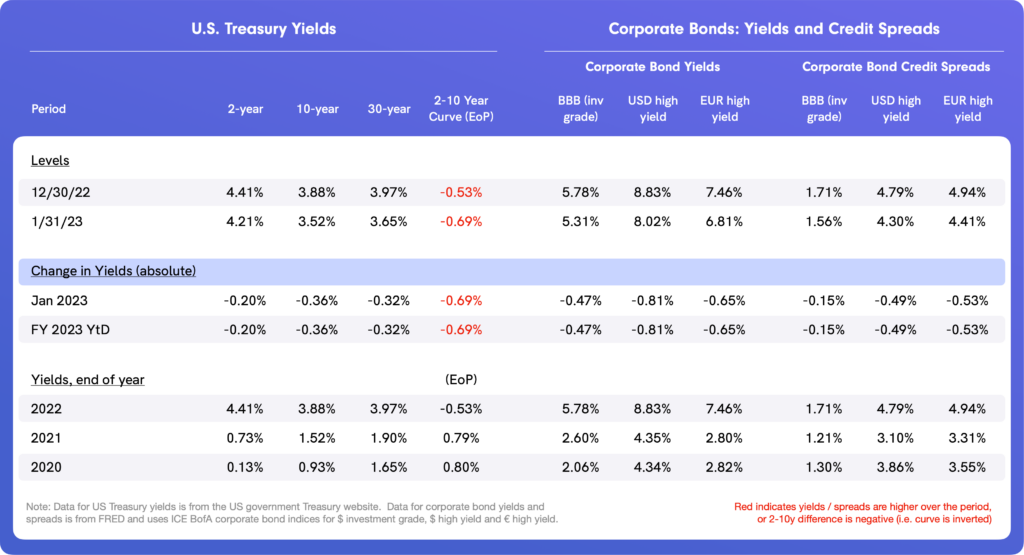

Bond Yields/Credit Spreads: “Goldilocks” economic conditions in January provided the perfect backdrop for bonds, as yields fell and prices rose across the board.

- The yield on the benchmark 10-year U.S. Treasury fell by 36bps in January and is now more than 100bps below its highest yield of 4.59% reached just over three months ago (on October 24).

- The combination of declining inflation (albeit slowly) and hopes that the Federal Reserve might reverse its hawkish approach as far as monetary policy cheered bond investors.

- There is an FOMC decision on February 1, with the Fed expected to increase the Federal Funds rate by 25bps to an indicated range of 4.50% to 4.75%. This is already priced in, although what will matter more to investors is the rhetoric that comes from Chairman Powell and other Fed officials after the FOMC monetary policy decision.

- Even as yields have fallen across the U.S. Treasury maturity curve, the 2y-10y U.S. yield difference remains significantly negative, meaning that the curve is inverted.

- Declining yields at the shorter-end of the curve suggest that investors believe the Fed might reach a lower terminal rate for the Federal Funds rate, and it might do so sooner than expected.

- Investors also are falling in line with a narrative that if inflation continues to decline, the Fed could pivot to a more dovish approach faster than had been anticipated.

- In corporate credit, there continue to be few if any signs that investors are concerned about a deterioration in credit quality, either in investment grade or high-yield credit, as credit spreads compressed across the board in January.

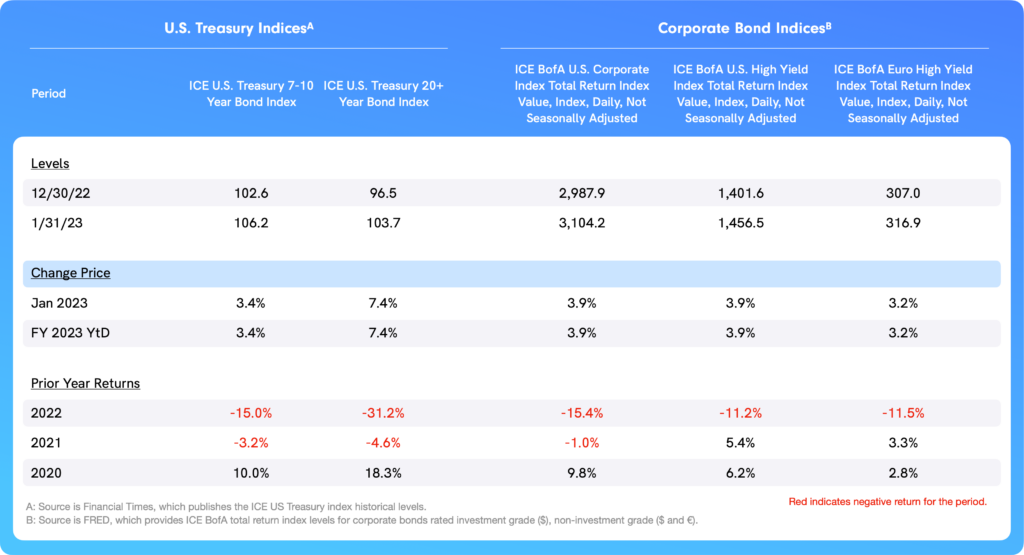

Bond Total Returns: With yields decreasing, both U.S. Treasuries and corporate bonds delivered solid returns in January following a dismal 2022.

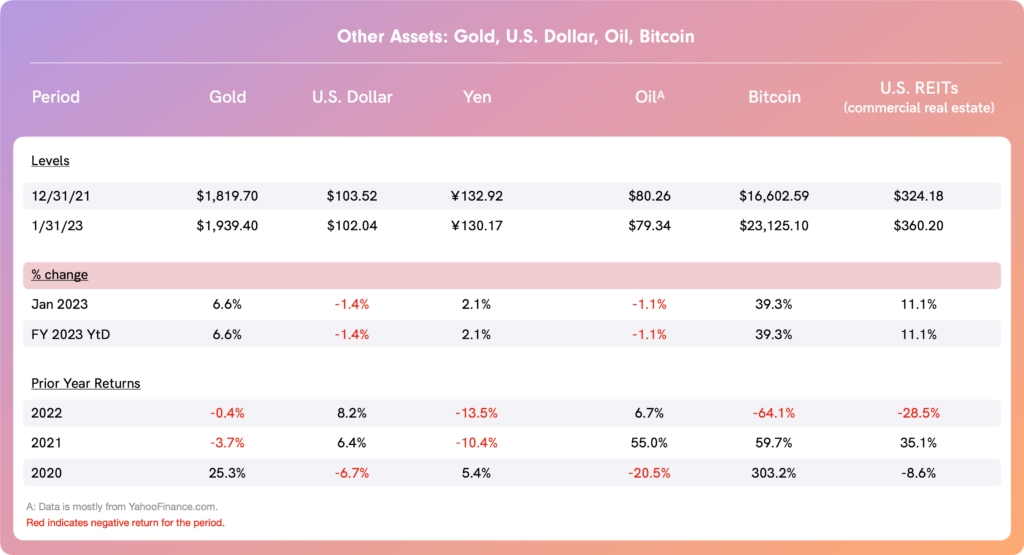

Currencies, Commodities & Alternative Assets: As far as currencies, both the U.S. Dollar and the Yen (another “safe haven” currency) stabilized in January, although the direction of travel remains the same as in December, with the U.S. Dollar continuing to slowly weaken and the Yen continuing to strengthen.

- Sterling and the Euro (not included in the table below) also strengthened in January, the Euro perhaps understandable given the improving outlook, but Sterling less so given the dire outlook for the U.K. economy.

- Following a very slight decline of 0.4% in 2022, gold started the new year strong with a solid 6.6% gain in January. This can perhaps be attributable to the ongoing objectives of many (foreign) central banks to buy gold in order to diversify their reserves and reduce their dependence on the U.S Dollar. However, it is also most certainly related to the weaker U.S. Dollar, which has had a similar effect on certain other Dollar-linked commodities and metals.

- Oil prices were little changed in January, with WTI crude trading in a narrow range of $79/bbl and $81/bbl during the second half of the month.

- After a horrible 2022, Bitcoin started the year with a gain of 38% in January as risk appetite returned to markets. Concerns following the bankruptcy of FTX and other cryptocurrency infrastructure players subsided, even as crypto-lender Genesis filed bankruptcy in January (anticipated).

February Outlook

As we start the new month, the focus will be on the first few days, during which important monetary policy decisions will be revealed from three major central banks – the Federal Reserve, the ECB (Eurozone), and the Bank of England (U.K.).

- These decisions, and importantly, the official policy statements and press conferences that follow the decisions, will be carefully watched by investors.

- While inflation seems to have peaked in all three countries, the job of central banks is far from over since inflation remains well-above the targeted 2%.

- The Fed increased the Federal Funds rate as expected by 25bps on February 1st, and the expectation is that the ECB and Bank of England will both increase their overnight bank rates by 50bps on February 2nd.

- Two-thirds of S&P 500 companies have not reported earnings yet, so this will also be closely watched.

- “Big tech” remains very influential as far as sentiment, and the first two days of February will also see earnings releases from Meta Platforms (Facebook), Alphabet (Google), Amazon, and Apple.

Investors need to carefully focus on whether or not management teams continue to express uncertainty about the future, and if so, whether or not this is negatively affecting investor sentiment (which it has not, at least so far).

About the Author

Tim Hall is a writer, speaker, blogger (emorningcoffee.com), consultant, and advisor. A former banker with 29 years of experience (buy side/sell side), Hall is also a former Independent Non-Executive Director of a U.K. “challenger bank.” He currently resides in London.

1US Bureau of Labor Statistics Consumer Price Index Summary for December, released January 12, 2023, is here.

2S&P 500 Earnings Dashboard 22Q4 | Jan. 31, 2023 provided by I/B/E/S data from Refinitiv is here.