October, traditionally considered a challenging month for equities, turned out in fact to be a positive month — one of the few this year — for U.S., European, and Japanese markets. Unfortunately, the news was not nearly as good for investors in government bonds, including U.S. Treasuries, although corporate credit was reasonably steady even as underlying yields increased.

Key drivers of sentiment across October included (but were not limited to):

- Data showing ongoing and persistently high inflation in the U.S., the U.K., and the Eurozone, although labor markets remain in reasonably good shape and unemployment remains at or near historical lows.

- A change in political leadership in the U.K. This followed a punishing sell-off in U.K. government bonds (Gilts) and Sterling caused by former PM Liz Truss announcing a plan of fiscal stimulus measures without funding, meaning it would be debt-financed. Ms. Truss was replaced quickly by former Chancellor of the Exchequer Rishi Sunak, who immediately scrapped the fiscal plan and calmed financial markets.

- Decent 3Q22 earnings, with banks, airlines, and energy companies delivering strong profits, and technology stocks (including the FAMAG companies) underperforming.

- Central banks are tightening monetary policy to address inflation as they continue a series of rate increases and embark on quantitative tightening (in the U.S. and U.K.). Central bank rhetoric suggests that there is no end in sight yet, as curbing inflation remains a priority over likely increases in unemployment.

- President Xi of China consolidated power at the recent CPC National Congress, further unsettling markets with respect to the world’s second largest economy. Chinese equities continue to struggle.

- OPEC+ announcing a reduction of 2 million barrels per day (bbl/day) in supply to prop up prices. This seemed to stabilize prices, which fell to the high of $70/bbl in September and have now settled comfortably back in a range of $85/bbl to $90/bbl.

- The 30-year U.S. fixed-rate mortgage rate rose above 7% at the end of October (7.08% on October 27), its highest level in over 20 years. Housing data is showing fewer sales and declining prices — not surprising given the trajectory of the Fed’s rate increases.

- Ongoing U.S. Dollar strength, which is continuing to cause distortions in the global economy. A strong U.S. Dollar means the U.S. is exporting inflation, and the strong U.S. Dollar is creating headwinds for U.S.-based multinational companies by making products more expensive abroad.

Performance of asset classes

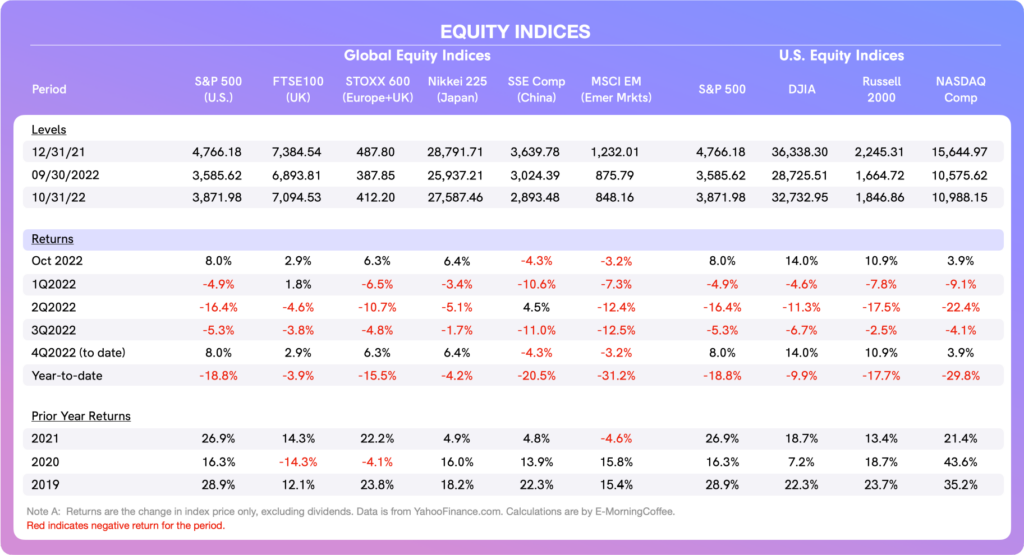

Equities: Equity markets in the U.S., U.K., Europe, and Japan all had positive returns in October — only the second positive month of 2022. Chinese and emerging markets equities slumped in October, making these equity market indices the worst performing of the year so far.

- In U.S. equity markets, the NASDAQ continued to lag other indices, with its negative return YtD (-29.8% YtD) three times worse than the DJIA (-9.9% YtD), the best performing index YtD in the U.S. High and volatile interest rates continue to negatively affect the NASDAQ because of its weighting towards technology stocks, many loss-making.

- Recently announced third quarter results for the infamous FAMAG stocks either fell short of consensus expectations or management delivered softer guidance for the quarters ahead (or in some cases, both). For these reasons, technology companies continue to get punished, and the effect is more perverse on those indices that are skewed towards this sector.

- Earnings for airlines, energy companies, and banks are powering ahead, providing more support for the DJIA, a smaller index by number of companies but one that is much more balanced as far as sector diversity.

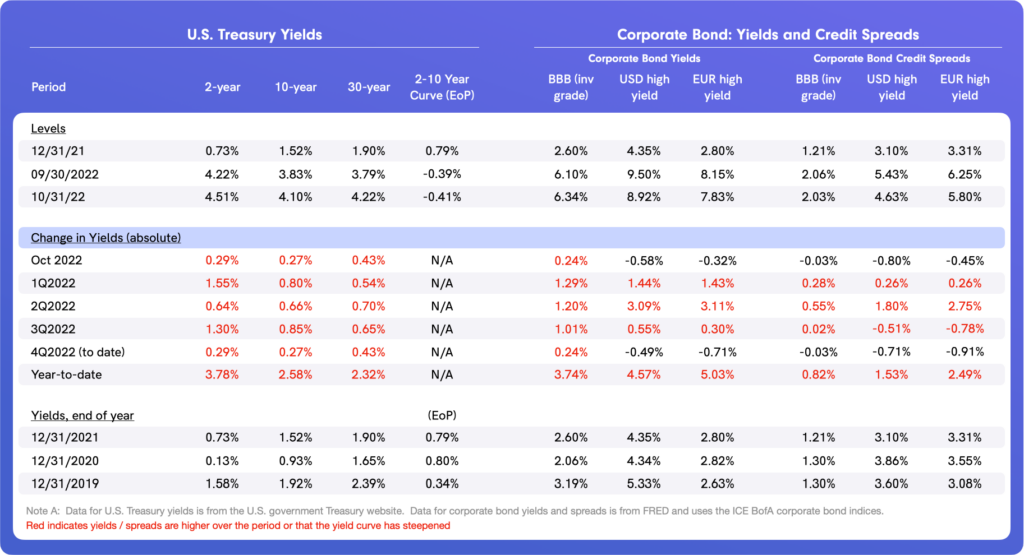

Bond Yields/Credit Spreads: U.S. Treasuries remain under pressure as the Federal Reserve ratchets up the Fed Funds rate, continues its quantitative tightening program ($95 billion/month), and sticks to its rhetoric that inflation is the number one priority — even if this approach causes the U.S. economy to slow and unemployment to increase.

- Bonds have seen declines as a sector all year. In October, the damage was more severe at longer maturities as investors are slowly realizing that inflation will likely remain elevated for some period and the trajectory down will be slower than had been expected.

- The yield curve, as measured by the 2y-10y UST yield differential, remains negative — or inverted — suggesting that a recession could be ahead.

- Corporate bond credit spreads tightened in October in both investment grade and high yield, showing that U.S. credit markets remain firm and resilient even as the economic clouds might be darkening on the horizon.

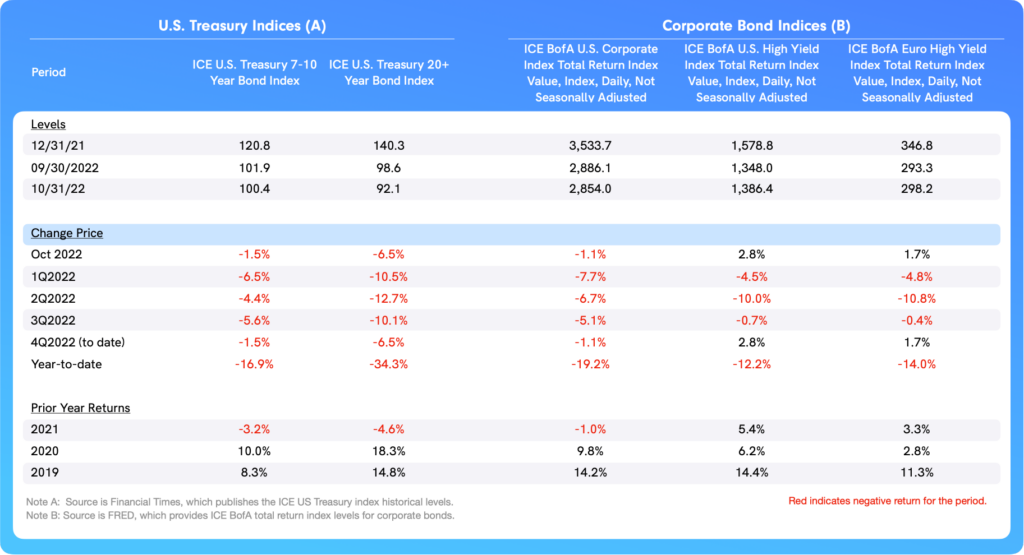

Bond Total Returns: Given the migration in yield and credit spreads discussed above, one wouldn’t be surprised to see that U.S. Treasuries lost further ground in October. The 20+ year total return index has had an abysmal and difficult-to-believe -29.8% return YtD.

- Intermediate maturities, reflected in the 7-10 year total return index, have done better than the long maturity total return index, but are still sufficiently negative to almost match the poor YtD return in the S&P 500.

- Truly, there has been nowhere to hide this year as far as traditional asset classes, with bonds and stocks remaining positively correlated but in the wrong direction.

October was fortunately a positive month for U.S. and European high-yield bonds, one of the few mainstream asset classes with positive performance YtD.

- The positive performance in October also shows that wider credit spreads — characteristic of non-investment grade bonds — provide some offset to increasing U.S. Treasury yields which are steadily pushing higher.

- This positive performance and its causes can be extrapolated into private debt, which typically has even higher credit spreads and often shorter maturities, making this asset class a potentially ideal fit for many portfolios.

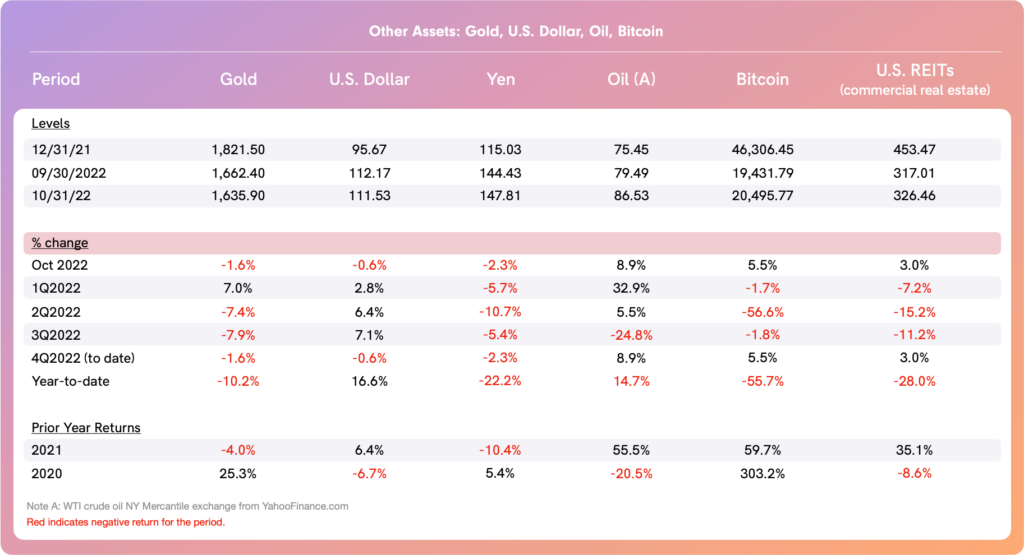

Currencies and Alternative Assets: The U.S. Dollar continues to remain at historically strong levels. The strength of the U.S. Dollar reflects a combination of investors perceiving there is less risk in the world’s most liquid reserve currency during turbulent periods, and the relatively better position of the U.S. economy vis-à-vis most other global economies.

- The Japanese Yen remains particularly vulnerable, as the Bank of Japan carries on with its overly accommodative monetary policy as the Fed, BoE, and ECB go the other direction and tighten.

- An overly strong U.S. Dollar leads to distortions in the global economy and creates particular headwinds for U.S. multinational companies as far as selling their products abroad.

- Oil also rebounded in October as OPEC+ signaled it would cut supplies, and global players served up record results in the quarter as oil prices remain elevated.

- Bitcoin continues to demonstrate resilience, having outperformed the S&P 500 and the U.S. Treasury market so far in the second half of 2022.

A Look Ahead

We are in the midst of earnings season (third quarter) for the S&P 500, with approximately one half of companies having reported and earnings generally coming in better than consensus expectations. We have several more weeks to go, although the expectation is that the trends will hold, providing some further support for risk assets as we head into November.

- The FOMC and BoE both have or will announce rate decisions this week, with expectations being that both will raise their overnight bank borrowing rates by 75bps.

- Perhaps the most significant wildcard on the table at the moment is the U.S. midterm elections. Polls seem to suggest that the House will go to the Republicans and the Senate is too close to call, but either outcome will largely smother any significant U.S. economic (fiscal) or political initiatives for the coming two years.

This newsletter was written in partnership with Tim Hall of EMorningCoffee.com. For more insights and other market learnings, subscribe to E-Morning Coffee today.