Perhaps the best thing to say about 2022 is that it’s over. Most stocks, U.S. Treasuries, and corporate bonds experienced significant depreciation during the year, with cash, stocks in a handful of sectors, and select alternative asset classes being the only respite. The S&P 500 index was down 19.4% for the year, and the 20+ year total return U.S. Treasury bond index was down 31.2 %. Most international equity markets mimicked the return of U.S. stocks, with the FTSE 100 (U.K.) being one of the only major market indices that was positive for the year. As far as December, both U.S. stocks and bonds had negative returns, although fortunately the returns were not poor enough to wipe out decent gains for the fourth quarter.

December Themes

There were three principal themes that were influential in December – one good, one bad, and one that remains uncertain.

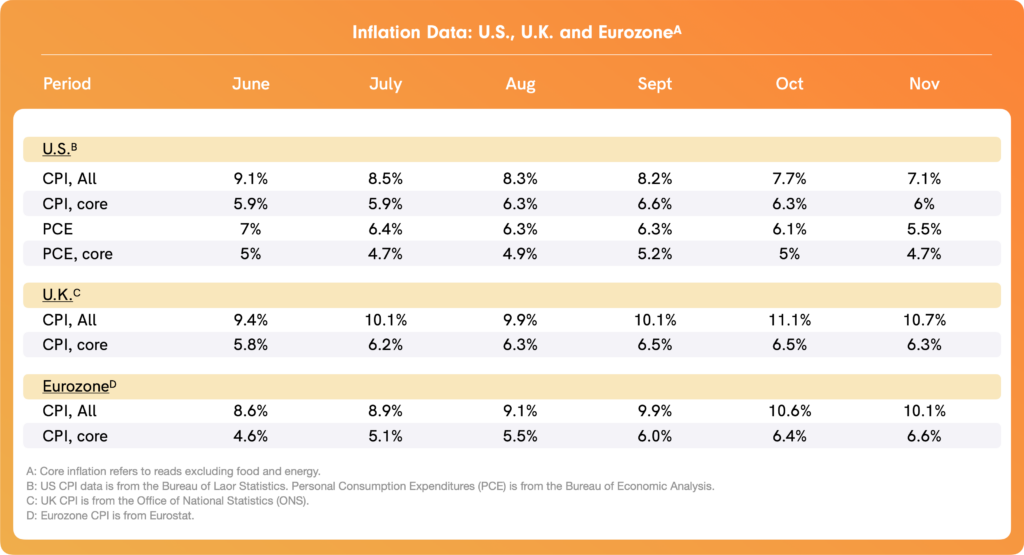

Good news: Headline inflation appears to have peaked in the U.S., the U.K., and the Eurozone.

- CPI is the most widely-reported inflation barometer, although the Federal Reserve focuses principally on Personal Consumption Expenditures, or PCE.

- CPI peaked in the U.S. in June, reaching a high of 9.1% year-over-year (YoY), and since then has steadily declined to 7.1% in November (last reported read).

- Core CPI and core PCE (meaning ex-energy, ex-food) peaked in September, and both have also declined since then.

- Inflation in the U.K. and Eurozone peaked more recently and remains significantly higher than in the US.

- Below is a summary chart for the last six months for CPI and PCE in the U.S., as well as CPI as reported in the U.K. and Eurozone.

- Slowing inflation (or “disinflation”) indicates that central bank monetary tightening is working, albeit slowly.

Bad news: The Federal Reserve, the Bank of England, and the European Central Bank (ECB) all continue on a trajectory of tighter monetary policy, accompanied by hawkish rhetoric – even if these policies lead to slower economic growth – so long as inflation remains above each bank’s target of 2%/annum.

- Bad news: The Federal Reserve, the Bank of England, and the European Central Bank (ECB) all continue on a trajectory of tighter monetary policy, accompanied by hawkish rhetoric – even if these policies lead to slower economic growth – so long as inflation remains above each bank’s target of 2%/annum.

- Although subtle on the surface, this change effectively means that the Bank of Japan has now joined other major developed economies in tightening monetary policy.

- In the U.S.:

- The Federal Reserve raised the Federal Funds rate seven times in 2022, including four increases of 75bps.

- The benchmark overnight bank borrowing rate, which started the year at a target range of 0% to 0.25%, ended the year at a target range of 4.25% to 4.50%.

- Both the Federal Reserve and the market more broadly suggest that the Fed will continue to raise the Federal Funds rate in 2023, possibly two to three more times, until a terminal rate of 5% to 5.25% is reached.

- The terminal rate could stay in place for all of 2023, with forward indicators again not suggesting a decrease in the Fed Funds rate until 2024.

- The Federal Reserve will continue to reduce the size of its balance sheet by around $95 billion/month.

- Economic projections suggest that unemployment will increase and economic growth will slow as interest rates continue to increase, risking pushing the U.S. into recession. The U.K. and Eurozone are already in recession.

Uncertain news: China has ended its zero-COVID policy, which could have short-term negative effects on the country’s economic growth.

- China is the world’s second largest economy (third if the E.U. is considered as a trading bloc), very influential as far as being a growth engine for global growth.

- The government is being fairly coy at the moment as far as disclosing disruptions stemming from ending its rigid zero-COVID policies, but there is evidence that the pandemic is spreading quickly throughout the country.

- The spread of COVID could lead to slower economic growth domestically, sporadic disruptions in manufacturing, and potential supply-chain issues, any of which could have negative knock-on effects for the global economy more broadly.

- However, the good news is that ending the zero-COVID approach should eventually completely re-open the Chinese economy following a year (2022) of disappointing growth, and the short-term costs might ultimately prove to be a small price to pay.

- It is unclear at the moment how this will play out.

Asset Class Performance

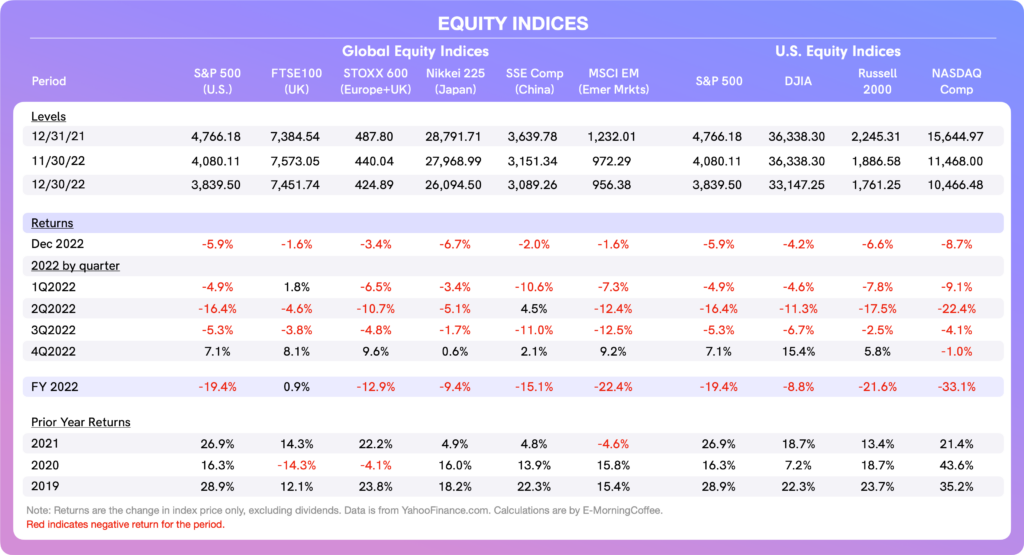

Equities: Following a strong November for stocks, December proved to be a more difficult month for most global equity indices.

- Perhaps not surprisingly given the shock announcement by the Bank of Japan to raise its yield curve control target, the Japanese equity market (Nikkei 225) was the worst performer of the month, down 6.7%.

- For the full-year, the U.K. benchmark equity index (FTSE 100) was the only positive performer, reflecting the fact that the composition of the index is skewed towards exporters, energy producers, and commodity companies, all strong performing sectors in 2022.

- In U.S. equities, a familiar theme continued in December that has been recurrent since the second quarter – underperformance by the NASDAQ Composite and overperformance by the DJIA.

- As the table above illustrates, the tech-heavy NASDAQ Composite was indeed the worst performing U.S. equity index during 2022, losing 33.1% and ending the year at a level last seen in July 2020.

- Rising interest rates continue to negatively impact interest-rate sensitive technology companies, putting downward pressure on the tech-heavy NASDAQ.

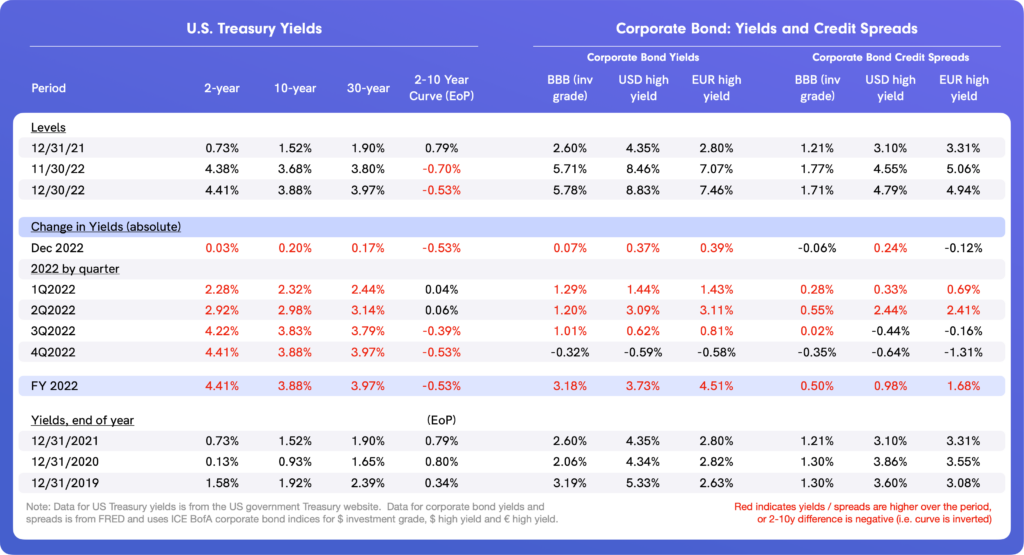

Bond Yield/Credit Spreads: U.S. treasury yields increased this month across the curve, albeit more significantly at the intermediate and longer end of the curve, reversing the trend experienced in November.

- The yield curve remains significantly inverted, although the inversion lessened slightly during December.

- As far as corporate bonds, yields increased in December in sympathy with higher yields in the underlying U.S. Treasury market.

- Credit spreads fell slightly in investment grade bonds but were higher in U.S. Dollar high yield.

- Concerns about a deterioration in credit quality, especially in the high-yield area, remain very much on investors’ minds as the probability of rising unemployment and a recession increase.

- Nonetheless, there is no evidence so far that credit is deteriorating significantly, as underlying fundamentals in non-investment grade credit remain generally supportive.

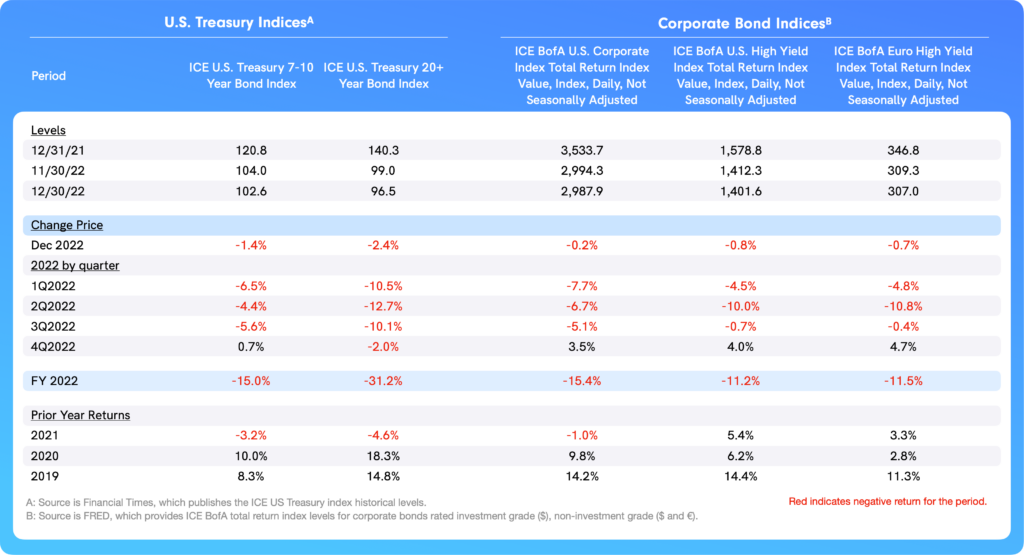

Bond Total Returns: With yields increasing, both U.S. Treasuries and corporate bonds delivered negative returns in December as might be expected.

- The principal culprit behind higher yields was ongoing fears regarding the extent of tightening that might ultimately be required by the Federal Reserve to address stubbornly high inflation.

- Although inflation is fortunately starting to slowly decline in the U.S., the employment market remains at near full capacity, and there is a continued imbalance between open jobs and available workers, most acute in select services businesses.

- Corporate bonds remain reasonably resilient given the context, although high-yield bonds showed a slight deterioration in prices in December.

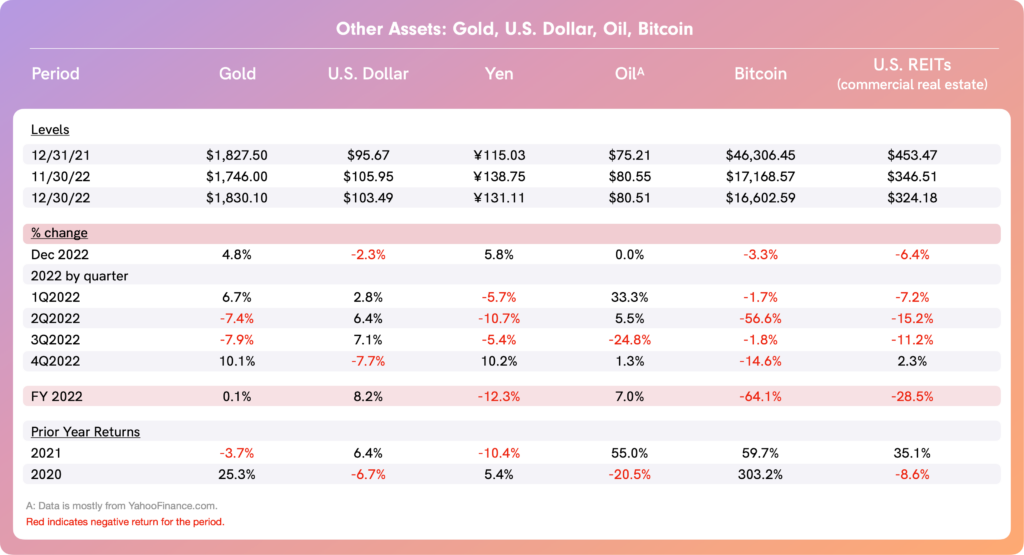

Gold, Oil, Alternative Assets & More: As far as other assets, much of the focus in December was on gold and oil, although there was significant volatility across many of these assets.

- From a currency-perspective, the Yen strengthened for the second month running, reflecting mainly the decision by the Bank of Japan to tighten its monetary policy, while the U.S. Dollar continued to back away from its highs reached at the end of the third quarter.

- Having finished marginally higher YoY, gold registered its second consecutive month of solid gains in December, resulting in a fourth quarter gain of 10.1%.

- Speculation suggests that the demand for gold has risen as central banks have sought to diversify their reserves in order to reduce their dependence on the U.S Dollar.

- Oil prices have remained under pressure, with WTI crude oil prices trading much of the month in the range of $70/bbl to $80/bbl. The low end of the range is the lowest of the year, even lower than the price before Russia’s invasion of Ukraine.

- To provide context, the price of WTI crude reached an intraday peak on March 7 of $130.50/bbl.

- Although the price has trended steadily down since March, oil did find support in mid-December, rallying off its mid-month low of $70.08/bbl to close flat on the month, ending the year at $80.51/bbl.

- Perhaps most important for Americans is that the price of “gas at the pump” has fallen from its high of $5.02/gallon on June 14 to $3.22/gallon on December 23 (last available read, from AAA’s website).

- In currencies, the Yen performed strongly in December, while the U.S. Dollar lost more ground, albeit more modestly compared to its decline in November.

- Having reached an unsustainably strong level in the third quarter, the U.S. Dollar (measured by the U.S. Dollar index, or USDX) has now declined for three consecutive months, down 7.7% in the fourth quarter.

- Bitcoin declined 3.3% in December.

- Although the return for the month was negative and capped an overall horrible year for the benchmark cryptocurrency, it was surprising the return was not even worse following the bankruptcy of FTX in November and the collateral effects across the broader cryptocurrency industry.

- For the full year, Bitcoin declined 64.1%, significantly surpassing losses in U.S. stocks and bonds.

January Outlook

Barring an unexpected change in the trajectory of inflation or Federal Reserve policy, the focus in the first several weeks of the new year will be on corporate earnings, which began in mid-January.

- The potential for earnings to surprise on the downside is more significant for fourth quarter earnings than the first three quarters of 2022.

- Valuation multiples (e.g. P/E ratios) compressed further during 2022 as the froth continued to come off risk markets generally, although multiples are still slightly elevated.

- P/E ratios in U.S. stock indices also remain elevated vis-a-vis similar indices in many international equity markets.

- U.S. stocks are a difficult call as far as 2023 expected performance at this point of the cycle.

- U.S. Treasuries may do better in 2023 than in 2022, as the slowing U.S. economy should eventually reduce the pressure on yields at the intermediate and longer end of the curve.

About the Author

Tim Hall is a writer, speaker, blogger (emorningcoffee.com), consultant, and advisor. A former banker with 29 years of experience (buy side/sell side), Hall is also a former Independent Non-Executive Director of a U.K. “challenger bank.” He currently resides in London.