November was a positive month for risk markets, the second in a row. Equities closed the month strong and remain on course for the first positive quarter this year. Equally encouraging for bond investors is the fact that yields on intermediate and longer-maturity U.S. Treasury yields declined this past month for the first time since July, translating into positive returns for bond investors in November, too.

Most of the sentiment drivers in November in the U.S. can be traced to the Federal Reserve (the Fed), which continues with its hawkish policies to address inflation. The month started with an Federal Open Market Committee (FOMC) meeting1 and ended with a speech by Fed Chairman Powell at the Brookings Institute2, with various governors and regional presidents of the Federal Reserve working tirelessly in between to remind investors over and over that the principal focus of monetary policy would be to bring down inflation, even if it comes with job losses and slower economic growth.

Key drivers of sentiment in November:

- The Fed raised the Federal Funds rate at the FOMC meeting on November 1-2 by 75 bps to a range of 3-3/4% to 4%. The Bank of England also raised its overnight bank rate in November, and the European Central Bank (ECB) did the same in late October at its last meeting.

- The October jobs report showed a slight increase in the unemployment rate to 3.7%, although the U.S. labor market overall remains resilient.

- The U.S. midterm elections came and went with plenty of attention, as investors were fearing a repeat of January 6. Fortunately, the elections went smoothly, resulting in an outcome that was more or less in line with expectations. Republicans regained control of the House, and Democrats retained control of the Senate. With this division, it may be unlikely that any meaningful market-moving legislation could be proposed and signed into law during the final two years of President Biden’s term.

- Crypto exchange FTX collapsed in early November, formally filing for bankruptcy on November 11. The collateral damage into the broader cryptocurrency market was – and remains – severe, demonstrating the systemic risk that is present in this fragile, inter-connected and opaque market. Fortunately, the contagion has not significantly spread outside of the cryptocurrency ecosystem into other risk assets.

- Various economic data releases throughout November were supportive of a slow decline from peak inflation, suggesting also that U.S. economic growth is ever so slowly starting to moderate. The Fed remains extremely data dependent, and the data appears to show that tighter monetary policy is starting to yield some results as far as reducing inflation.

- Thanksgiving resulted in what was essentially a half week, but even as volumes declined into the holiday period, sentiment remained generally supportive across risk markets. Equities and bonds were more or less range bound during the latter part of November, that is until a strong, late afternoon rally occurred following Fed Chairman Powell’s presentation at the Brookings Institute on the last day of the month.

- China’s “zero-COVID policy” came under progressively greater pressure domestically from Chinese workers and other citizens as the month wore on, visible in widespread street protests in some large cities. However, the government appeared to have adopted some new and slightly more flexible COVID policies towards the end of the month that has soothed Chinese citizens for now. As the world’s second largest economy, strong growth in the Chinese economy is paramount to strong global economic growth.

Asset Class Performance

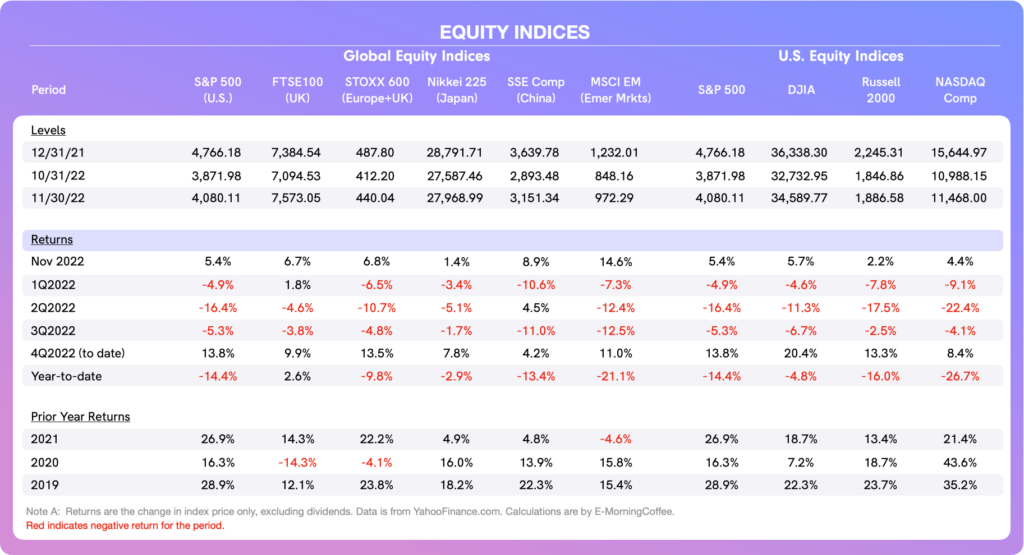

Equities: All of the global equity indices we track were positive in November for the first time this year.

- The MSCI emerging markets index was the best performer for the month, which is partially attributable to the fact that the U.S. Dollar (USD) has declined from its late third-quarter peak.

- European indices also performed very well in November. It is interesting to note that the FTSE 100, the equity index in the most troubled G7 economy (the U.K.), is the only equity index that is positive YTD. This demonstrates how investors often anticipate and value the future over the present.

- As far as U.S. equity indices, the Dow Jones Index (DJI) was the best performer in November and is the best-performing U.S. equity index YTD.

- All of the U.S. indices were positive in November, with the end-of-month rally most benefiting the NASDAQ, which is weighted towards higher volatility technology stocks.

- U.S. equity returns are positive for 4Q22, encouraging because a strong fourth quarter would at least partially offset fairly significant losses in U.S. stocks YTD.

- The tech-heavy NASDAQ remains the most troubled U.S. index, down nearly 27% YTD.

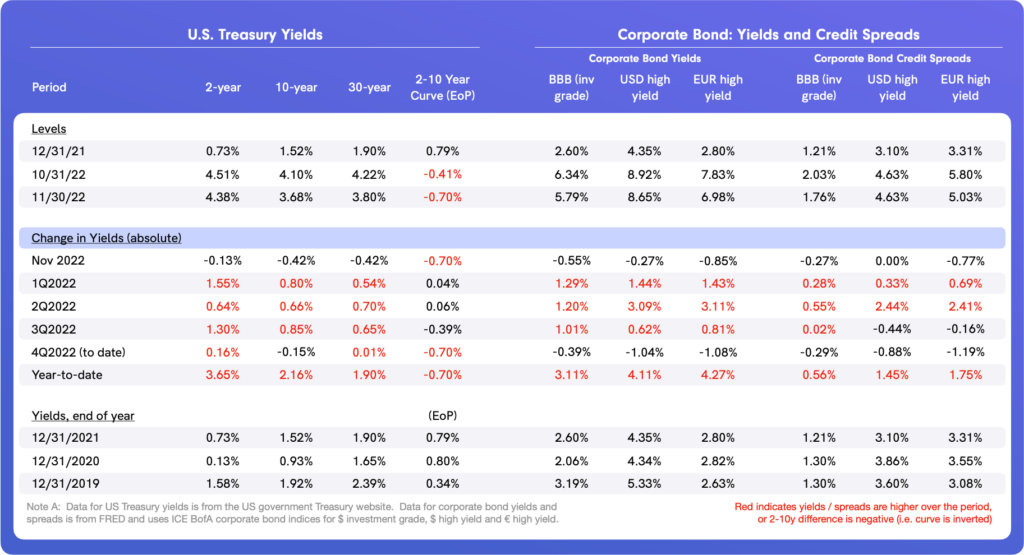

Bond Yields/Credit Spreads: U.S. treasury yields declined this month, most significantly at the intermediate and long end of the curve. Falling yields mean rising prices, discussed further below.

- The yield curve – measured by the difference between the two-year and 10-year UST yields – continues to steepen, signaling a growing risk that the U.S. will fall into a recession as the Fed continues to raise the Federal Funds rate and shrink its balance sheet.

- Yields at the shorter end of the yield curve, including the much-watched two-year UST, remain heavily influenced by the expectation of further increases in the Federal Funds rate, with a 50 bps increase for the last FOMC meeting of the year (December 13-14) largely priced in.

- Falling in line with improving sentiment in equities and lower yields on US Treasuries, corporate bonds also rallied in November.

- Concerns about a deterioration in credit quality – especially in the high-yield area – remain very much on investors’ minds as the probability of rising unemployment and a recession increase.

- Nonetheless, there is no evidence so far that credit is deteriorating as underlying fundamentals remain solid and supportive of credit assets.

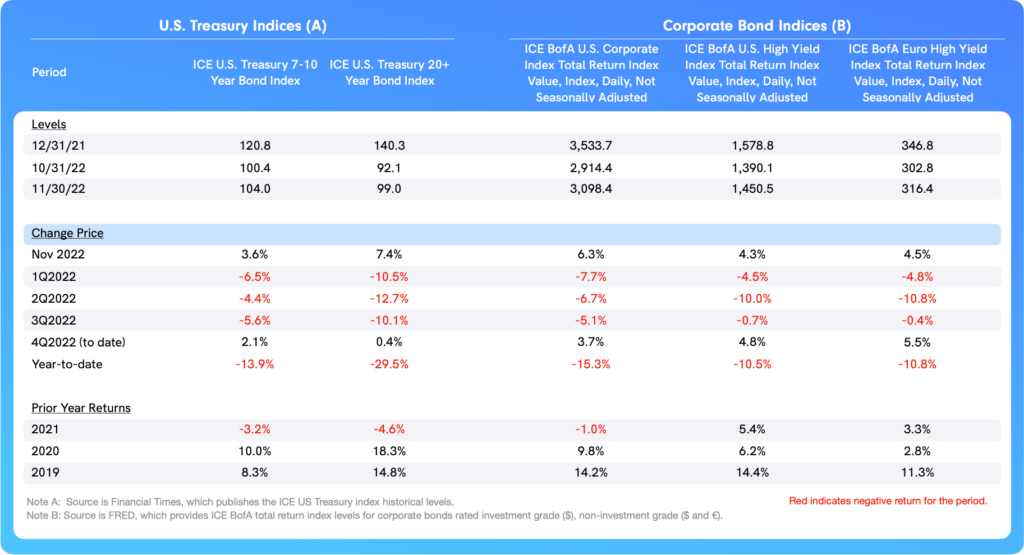

Bond Total Returns: Total returns for both U.S. Treasuries and corporate bonds were positive across the board in November.

- Considering the poor performance of U.S. Treasuries for much of the year so far, November certainly brought some welcome relief to investors.

- Even with the November rally, the total (negative) return on the 20+ year UST total return index YTD is worse than that on the NASDAQ, which in turn is the worst-performing U.S. stock index YTD.

- Corporate bonds also had a decent month, attributable to a combination of lower underlying UST yields and ongoing confidence as far as credit.

- Returns for the investment grade bond and high-yield bond indices are still down around 15% and 11%, respectively, YTD.

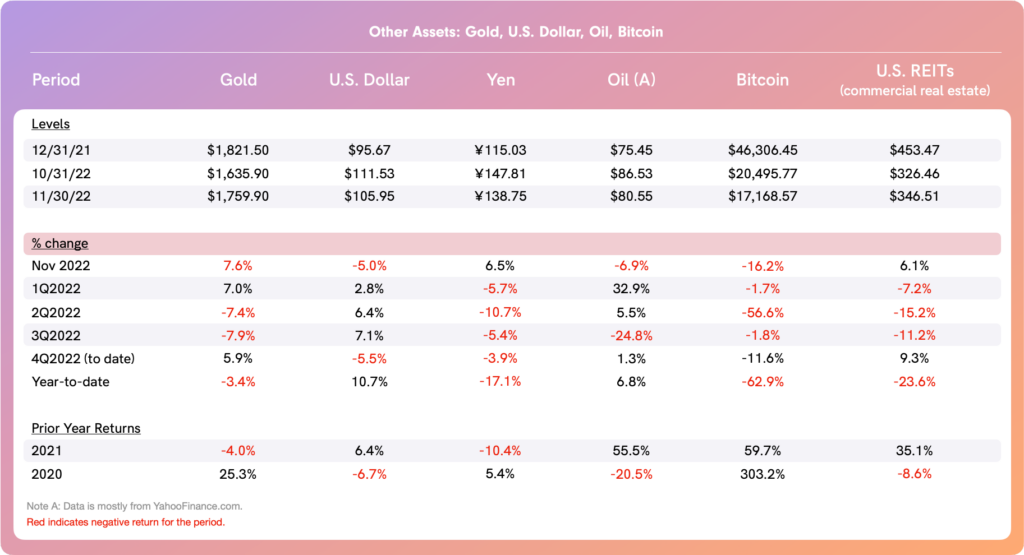

Alternative Assets and More: As far as other assets, most attention in November was on the USD, oil prices, and price of Bitcoin.

- The USD has finally moved off the peak level it reached in late September, and is now down 5.4% since then.

- Much of the decline occurred in November (-5.0% month over month). The greenback’s weakness has certainly improved some of the global market imbalances that were affecting broader markets.

- This has been most visible in the strengthening of emerging markets equities and bonds. A weaker USD should also have a positive effect on the revenues and operating margins of U.S. multinational companies, which we might begin to see in fourth-quarter earnings (to be released starting February 2023).

- Oil prices have been under intense pressure, less related to supply (which OPEC+ is trying to constrain) and more in anticipation of demand destruction as the global economy slows.

- WTI crude closed November at $80.55/bbl, down 6.9% in November following a nearly 25% decline in the third quarter.

- YTD, the price of WTI crude has fallen 17.1% in spite of Russian supply being heavily curtailed as a result of war-related sanctions.

- Bitcoin continued to get slammed in November, having never really fully recovered from issues that began to surface in April.

- The rather sudden failure of FTX reverberated throughout the broader cryptocurrency market, causing prices of all cryptocurrencies and related infrastructure companies to plummet.

- BTC was down 16% in November and is down 63% YTD.

A Look Ahead for December

All of the major central banks will meet in December, including the Federal Reserve, Bank of England, European Central Bank, and the Bank of Japan.

- Most eyes will be focused on the Federal Reserve, which is expected to raise the Fed Funds rate another 50 bps, to 4.25% – 4.50%, at the next FOMC meeting on December 13-14. As has customarily been the case, what is said after the FOMC meeting will likely be more important than the Fed’s actions.

- As far as economic data, there is expected to be growing evidence of declining inflation and a slowing U.S. economy. Risk markets seem to be in front of this as far as expectations, so unless there is a sharp surprise one way or the other, risk assets might continue to trade in a narrow range.

- A more accommodative Fed is (likely) a ways off, but there is hope that the significance of Fed tightening might moderate, even if only slightly, in the coming weeks.

- The growing risk of a recession in the U.S. does not seem to be of concern to investors at the moment, although this might change if the economic data begins to deteriorate more quickly than anticipated.

1The press release following the FOMC meeting on November 1-2 is here. Minutes from the Nov 1-2 FOMC meeting were released on November 23, and you can find them here.

2Chairman Powell addressed the Brookings Institute on November 30, and you can watch the speech and Q&A which followed here.