Volatility settled down considerably in April, supporting another solid month for risk assets, including global equities and corporate bonds. U.S. Treasury yields were volatile during the month, particularly at the short end, but actually ended the month little changed.

Concerns about a bank crisis following the March failures of Silicon Valley Bank (“SVB”) and Signature Bank largely subsided, although First Republic remained the poster child for bank problems with its shares falling a further 75% in April as the bank raced towards being acquired or allowed to fail.

- On May 1, JP Morgan announced that it would take over First Republic Bank with support from the Federal Deposit Insurance Corporation (FDIC), hopefully closing the book on bank stress in the U.S. for the time being.

- Fortunately, this situation does appear isolated for the time being. Big tech earnings, announced the last week of April, were better than expected, which further buoyed risk markets. There continue to be no tangible signs of credit stress, at least in the public bond markets, as spreads across the credit spectrum ended the month a touch tighter.

The first week of May will bring decisions from the Federal Reserve and the European Central Bank (ECB), with both expected to increase their overnight borrowing rates by a further 25bps. Inflation is trending in the right direction in most G7 countries, but it is a slow burndown. In addition, economic indicators suggest a slowing U.S. economy, and perhaps even a recession in the second half of this year.

April Themes

S&P 500 earnings: S&P 500 earnings reports for the first calendar quarter kicked off in mid-April, led by banks. Investors were largely focused on deposit flows following the March mini-bank crisis. Overall, 1Q23 results for banks were largely as expected – there was a migration of deposits out of mid- and small-sized banks into “too big to fail” banks, although overall the banking system lost deposits.

- In the last week of the month, four of the five “big tech” companies (Microsoft, Meta Platforms (Facebook), Alphabet (Google), and Amazon) released earnings, and all beat analysts’ expectations, a stark contrast to the first quarter of last year when all disappointed.

- Analysts and investors are paying careful attention to what companies are saying on their post-earnings management calls, looking for signs of a slowing U.S. and global economy.

- In this respect, the outlooks have been mixed, with several companies – including Amazon – highlighting that customers were continuing to look for ways to reduce costs and this would likely undermine revenues and profitability going forward.

The debt ceiling debacle: We are drawing nearer to the day when the U.S. Treasury could run out of money, with no solution to raising the debt ceiling in sight.

- This is a recurring issue every few years that just won’t go away, unfortunately exposing the polarization of U.S. politics at the moment.

- It’s hard to say if investors take this risk seriously, but it is certainly a distraction that we don’t need at the moment.1

OPEC+ cuts supplies: OPEC+ announced on April 2 that it would introduce another round of supply reductions starting in May in order to stabilize oil prices, which had reached a 16-month low in March of below $70/bbl (WTI crude).

- This announcement by OPEC+ quickly boosted the price of oil back above $80/bbl, but prices stabilized and then fell slightly to end the month at $76.63/bbl.

- Weaker prices are related to growing concerns about an economic slowdown in the second half of the year, especially after weaker-than-expected 1Q23 real GDP in the U.S. (released last week) came in sharply below expectations.

Concerns about banks linger: First Republic was in focus for much of April as the bank continued to lose deposits and was clearly headed toward failure. Regulators saw the writing on the wall, and asked U.S. banks to bid for First Republic with support from the FDIC.

- On Monday morning (May 1st), JP Morgan and the FDIC announced the acquisition of First Republic by JP Morgan on yet-to-be-disclosed terms, but certainly with some backstop from the FDIC on First Republic’s asset book. Most investors view this as another one-off risk given the unique attributes of First Republic, and it is hoped that this transaction marks the end of U.S. bank stress.

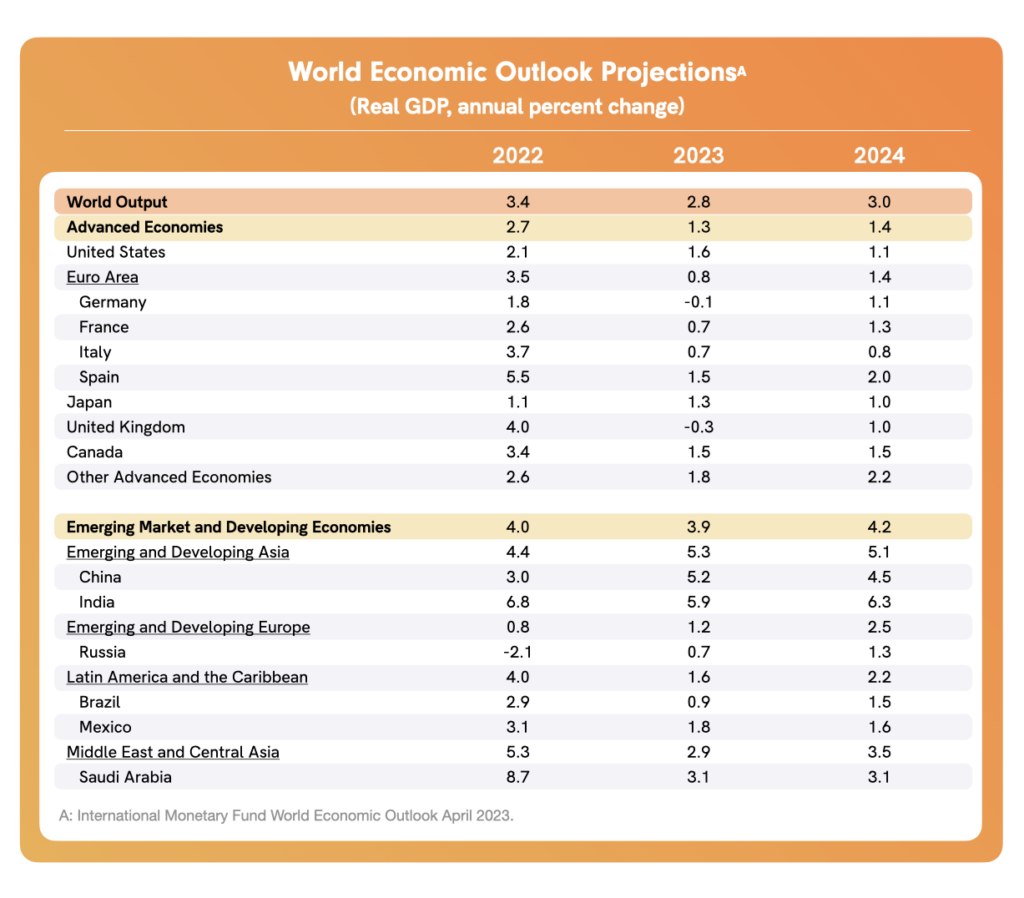

The World Economic Forum was held in mid-April, during which the International Monetary Fund (IMF) revised its global forecasts to reflect slower economic growth ahead. Below is the “Projections Table” extracted from the report,2 which provides the IMF’s views on economic growth for 2023-2025 for developed and larger developing countries.

Economic data mixed, inflation still lurking: We continue to have mixed economic news in the U.S., as investors vacillate between a so-called “soft landing” and an outright recession in the second half of 2023. Economic growth indicators remain mixed but clearly suggest a slowdown is ahead.

- 1Q2023 real GDP for the U.S. and the EU was 1.3% and 0.1%, respectively, indicating that the world’s two largest economic zones are slowing.

- Housing is also under pressure in the U.S., and forward indicators suggest that businesses are being more cautious in their outlook.

- Retail sales in March in the U.S. were reported mid-month (in April), and were lower than expected, suggesting a potential weakening in U.S. consumer demand.

- However, against this backdrop, the jobs market remains firm for now in the U.S., driven by services, and inflation is continuing to trend lower but at a pace that is not sufficiently comforting to the Federal Reserve.

Performance of asset classes

Equity market performance, April 2023

Global Equities

- Except for the emerging markets index (MSCI EM), all of the global indices we track were positive in April, and all traded within a relatively narrow range. The FTSE 100 (+3.1%) and the Nikkei 225 (+2.9%) were the best-performing indices in April.

- Japanese equities (Nikkei 225) have delivered the best return year-to-date (+10.6%), followed by European equities (STOXX 600, +9.8%). Emerging markets equities have been the weakest performer.

U.S. equities

- Although the NASDAQ Composite was flat in April, the tech-heavy index held onto its impressive YtD gains, delivering so far a sizzling 16.8% YtD. This is almost double the YtD return of the S&P 500 index and follows a dismal performance in 2022 when the NASDAQ was down 33.1%.

- The DJIA was the best-performing U.S. index in April (+2.5%), and the small-cap Russell 2000 was the worst (-1.9%).

- Volatility settled sharply in April, with the “fear index” VIX decreasing from 18.70 at the end of March to 15.78 at the end of April, its lowest level since October 2021.

Bond market performance, April 2023

Yields/credit spreads

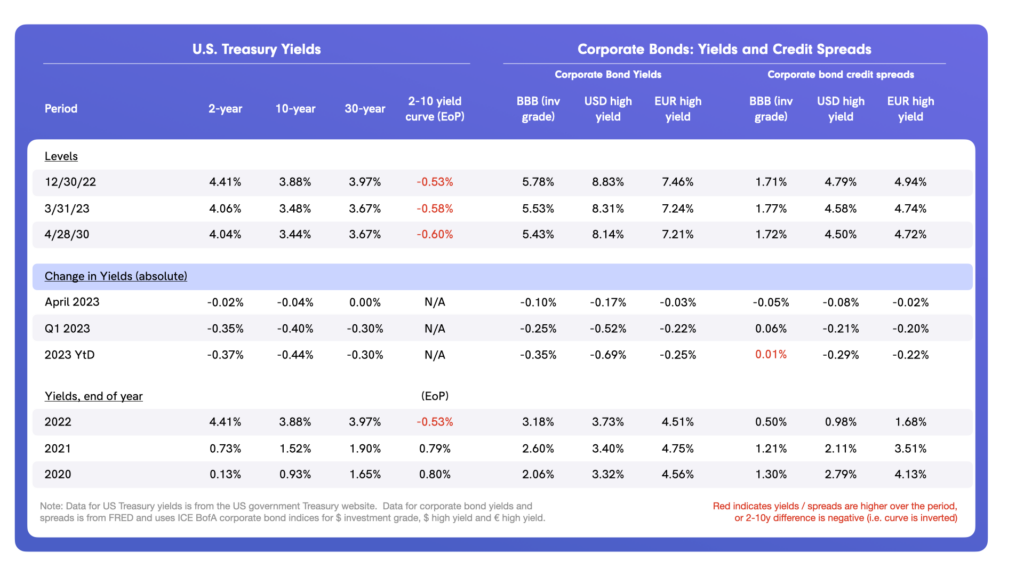

- Although there was volatility during the month, the U.S. Treasury yield curve was little changed by the end of April (vs end of March). The 2-year U.S. Treasury, which has a closer correlation with movements in the Federal Funds rate, had wide yield dispersion in April, ranging from a low of 3.79% (April 5th) and a high of 4.24% (April 19th), before closing the month at 4.04%, little changed compared to the end of March. The 2-year UST appears to be “pricing in” a 25bps increase in the Fed Funds rate on May 3rd at the conclusion of the next FOMC meeting.

- Similarly, yields were little changed at the intermediate and long end of the curve, although yields generally increased in the first half of April and have steadily decreased since then as concerns about the economy have started to gain traction.

- The index that tracks bond market volatility – MOVE – declined sharply in April but still remains elevated compared to historical levels.

- The 2yr–10yr yield curve has held its inversion at around negative 60bps (2yr vs 10yr), still suggesting an economic slowdown or recession ahead.

- The pending debt ceiling issue has distorted yields on UST Bills (less than 12 months), especially those bills that are due in the next month before the U.S. Treasury is expected to run out of money should there not be a resolution to the debt ceiling.

- Both investment grade and high-yield corporate bond credit spreads were marginally tighter in April, following widening in March after the mini-bank crisis. The tightening suggests little concern so far in the investor community about a credit crunch as banks curtail lending and the economy slows. Money supply is shrinking slowly suggesting money is continuing to leave U.S. banks. However, the stability of corporate credit spreads might reflect the fact that shadow (unregulated) lenders, like private credit funds, are increasingly keen to “fill the gap” left by banks.

Total returns

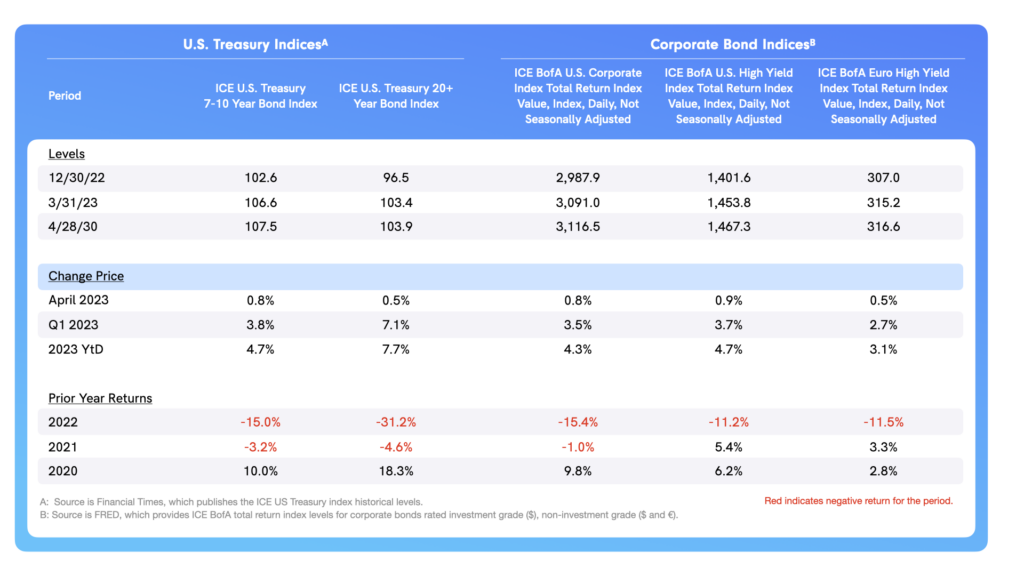

- Bonds have been a good asset class so far in 2023, especially longer-duration government bonds. Both corporate bonds (investment grade and high yield) and U.S. Treasuries registered solid gains in April.

- Long-duration U.S. Treasury bonds, as measured by the ICE UST 20-year total return bond index, have had the best return YtD as yields on 10- and 30-year U.S. Treasury bonds are significantly lower since the end of 2022.

Other Assets, Alternative Assets: Performance April 2023

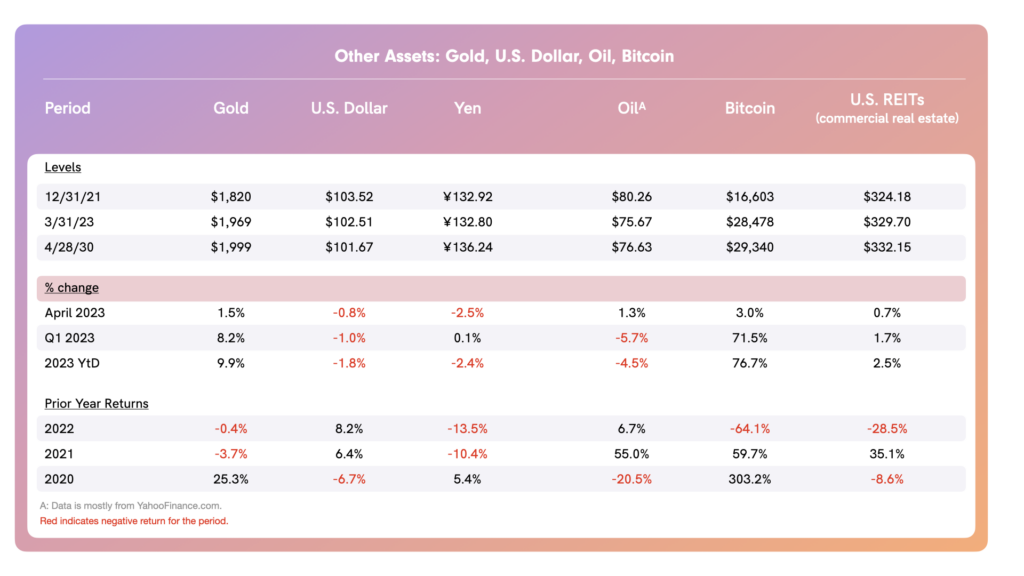

- Volatility was less pronounced in safe haven and other assets in April, too, not dissimilar to what we experienced in stocks and bonds.

- As far as currencies, the U.S. Dollar lost 0.8% against the DX-Y (currency index) in April, bringing its total loss to 1.8% YtD. The U.S. Dollar is coming off of record highs from mid-summer 2022, so to see weakness is not surprising. It certainly does not justify the extensive coverage in the financial press about the U.S. Dollar losing its reserve currency status. The Japanese Yen’s losses accelerated late in the month following the Bank of Japan’s decision last week to stick with its easy monetary policy, diverging from the (contractionary) policies of other G7 banks.

- The price of WTI crude oil increased 1.3% in April, with closing prices during the month ranging from $74.30/bbl (April 25th) to $83.26/bbl (April 12th), before settling to end the month at $76.63/bbl.

- Bitcoin’s gains moderated in April and there was heightened volatility, but the benchmark cryptocurrency still managed to gain 3.0% for the month, adding to its impressive YtD gain of 76.7%.

- Commercial real estate remains a concern for markets, especially since banks and insurance companies have a chunky allocation to this asset class. Although the year-to-date return for the U.S. REIT index trails the S&P 500, it is nevertheless positive for the year as investors do not seem to be abandoning the asset class completely.

Outlook

April was a month in which volatility settled even though it was characterized by concerns over the future direction and magnitude of economic growth, and lingering concerns over small- and mid-sized U.S. banks that have hopefully been put to bed with the acquisition of First Republic Bank.

- The first half of the earnings season for S&P 500 companies was generally supportive, at least vis-à-vis dampened expectations.

- The Federal Reserve, the ECB, and the Bank of England will all provide monetary policy decisions at meetings this week (Fed, ECB) and next (BoE), and all are expected to hike overnight bank borrowing rates by 25bps.

- Just less than half of the S&P 500 companies still have to report 1Q23 earnings, so there will be much attention focused on both actual earnings and what management teams have to say about general consumer and business sentiment as they look ahead.

1Should you wish to understand this issue more, you can read “The US debt ceiling debacle” in E-MorningCoffee.

2More detail from IMF’s recent report can be found here.

About the Author

Tim Hall is a writer, speaker, blogger (emorningcoffee.com), consultant, and advisor. A former banker with 29 years of experience (buy side/sell side), Hall is also a former Independent Non-Executive Director of a U.K. “challenger bank.