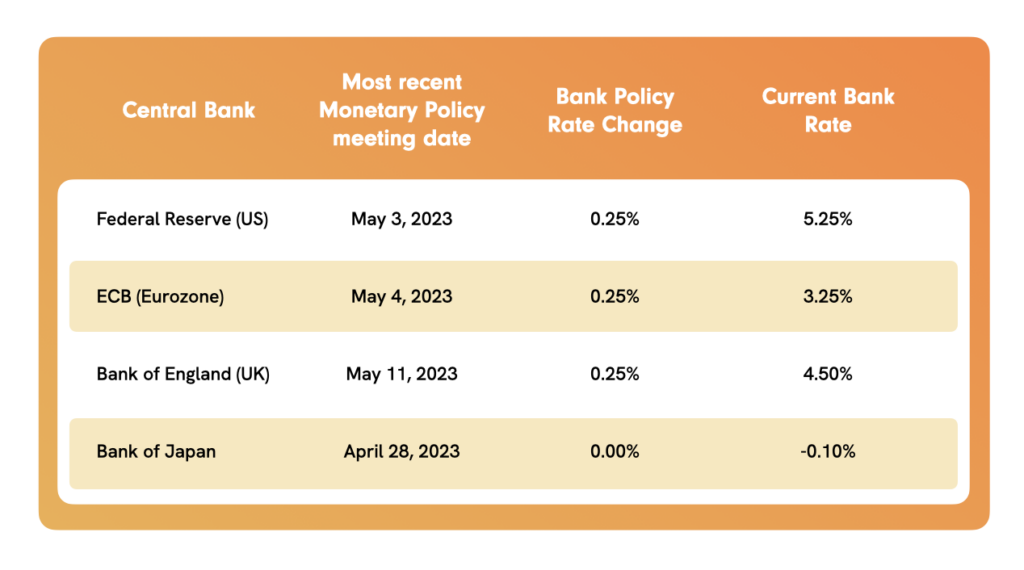

May was a month dominated by a debt ceiling standoff, along with ebbs and flows in interest rate expectations, both of which had collateral effects on risk markets more broadly. On May 3, the Federal Open Market Committee (“FOMC”) increased the Federal Funds rate for the 10th consecutive meeting by 25bps to 5.00% – 5.25%.

- The consensus view was that this would likely be the last increase in the key overnight bank rate, as data suggested that inflation was heading in the right direction.

- However, towards the end of the month, a series of economic data releases – mostly jobs-related – indicated that the U.S. economy remained more resilient than thought.

- This, in turn, threatened the trajectory of inflation back towards the 2% per annum target, a fact that was later confirmed when core inflation was shown to be sticky.

- As a result, investors reversed their expectations of a so-called interest rate pause by the Fed and instead started to price in a further 25bps increase in the Fed Funds rate at the next FOMC meeting (June 13-14).

- U.S. Treasuries sold off (meaning yields increased), and stocks became more fragile as this reality set in.

- However, this change in investor expectations spurred Fed officials into action, with various Federal Reserve governors and regional bank presidents going on the “speakers’ circuit” in the final days of the month to guide expectations back towards a potential pause at the mid-June FOMC meeting.

Throughout the month, the political theater of another debt ceiling “crisis” was ongoing, grabbing headlines but – to be fair – having virtually no effect on risk markets even as the so-called “x date” drew nearer. Even with these shifts in investor sentiment and the debt ceiling discussions, intra-month volatility across financial markets was generally milder than might have been expected.

May Themes

- Central banks hike rates: As anticipated, the Federal Reserve, the Bank of England and the European Central Bank (ECB) all raised their overnight bank policy rates by 25bps at their respective early May monetary policy meetings. The Bank of Japan, however, continued to diverge from its G7 peers, leaving its very accommodative monetary policy intact. This has largely been the catalyst for a weakening Yen and a stronger Japanese stock market this year.

- Regional bank crisis: The U.S. regional bank crisis which began in early March has stabilized for the time being. The last domino to fall was First Republic Bank, which was taken over by the FDIC on May 1 and immediately sold to JPMorgan Chase, rescuing depositors at the bank but wiping out its shareholders. Read more about this transaction in the official JPMorgan Chase press release here. For the remainder of the month, the shares of U.S. regional banks were more stable but remained significantly below mid-February levels when the first signs of a loss of confidence by investors became visible.

- U.S. economic data: Unemployment fell to 3.4% in April and more jobs were added than expected (see the Bureau of Labor Statistics report).

- JOLTS data released in late May showed that for the first time since December 2022, new job openings ticked up in April, suggesting that the employment market in the U.S. has not been adversely affected by monetary policy tightening.

- CPI data released earlier in the month was on target, an encouraging sign for inflation (read the April BLS CPI report). However, the most-monitored gauge of inflation for the Fed – the change in core Personal Consumption Expenditures (PCE) – came in well above expectations for April (per the BEA PCE report).

- The slow pace of disinflation coupled with better-than-expected employment data has increased the odds that the Federal Reserve will raise its benchmark Fed Funds rate at its next FOMC meeting in mid-June.

- Debt ceiling (nearly) resolved: An issue that has been hanging over financial markets now for several months appears to be nearly resolved, with the Biden Administration and Speaker of the House, Kevin McCarthy, having reached a compromise solution in late May to increase the debt ceiling. The legislation was approved by a non-partisan majority vote in the House of Representatives on May 31, approved by the Senate on June 2, and is now awaiting President Biden’s signature into law, which is imminent. This unfortunate and recurring saga caused FitchRatings to put the U.S. on Rating Watch Negative, signalling a potential downgrade of its current AAA rating (read the Fitch press release).

- Nvidia / artificial intelligence: Thematically in equities, the sharp increase in the S&P 500 index, and more perversely, the NASDAQ Composite year-to-date (YtD) has been driven almost exclusively by a handful of large technology companies, including the traditional giants Apple, Microsoft, Amazon and Alphabet (Google).

- Chip-designer Nvidia shocked markets in late May with the release of much stronger-than-expected earnings in its fiscal Q1 24 (ended April 30, 2023), pushing its stock higher by 24.4% the day following the announcement.

- One of the key drivers of Nvidia’s surprisingly strong results, as well as a catalyst for increases in the stock prices of many other technology companies, is optimism over artificial intelligence (AI).

- China growth: Growth in manufacturing and consumer spending in China was slower than expected in April, according to data released in late May. The PMI manufacturing index for April fell back below 50, to 49.2, according to data from the National Bureau of Statistics. As the world’s second largest economy behind the U.S. (and similar in size to the EU economy), slower growth in China undoubtedly has broader (negative) implications for the global economy.

Asset Class Performance

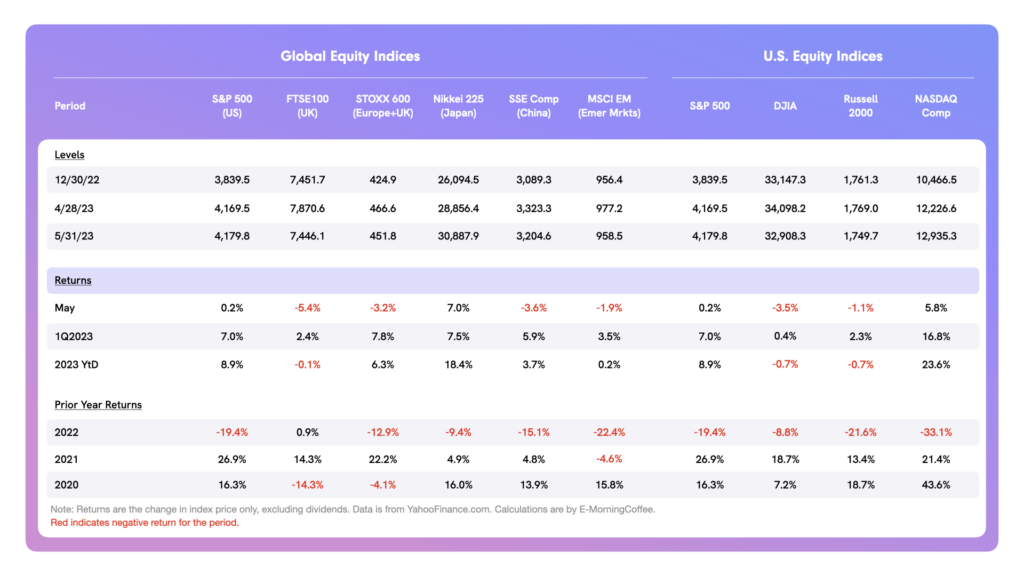

Global Equities: European and emerging stocks fell in May, while U.S. stocks (as gauged by the S&P 500) eked out a small gain. This was the third consecutive month of gains in the benchmark S&P 500 stock index, bringing the YtD return for the S&P 500 to an impressive 9.5%.

- Japanese equities (Nikkei 225) continue to deliver the best returns of the global indices. The Nikkei 225 led the charge in May with an impressive 7.0% gain for the month, bringing its YtD gain to 18.4%. The YtD return is more than double that of the S&P 500 index, as Japanese equities continue to benefit from very accommodative monetary policy.

- European stocks, measured by the STOXX 600 index, also remain positive YtD, although their performance in May (-3.2%) was poor.

U.S. Equities: In a recurring theme that has characterized much of the year, the tech-heavy NASDAQ Composite continues to be the strongest performer. Whereas the S&P 500 was barely positive in May, the NASDAQ Composite generated a return of 5.8% for the month and is now up 23.6% YtD, a sharp reversal from its 2022 loss of 33.1%.

- What is less obvious in the overall U.S. index returns is the influence of large technology companies, which have accounted for most of the gains in both the NASDAQ and the S&P 500 this year.

- The large-cap (and concentrated) DJIA and the value-oriented Russell 2000 have had poorer returns this year than the broader indices, with both negative in May and year-to-date.

- Volatility as measured by the VIX (the so-called “fear index”) was range bound much of May, fluctuating between 16 and 20, an encouraging sign especially in light of the uncertainty caused by the debt ceiling discussions that dominated the narrative for much of the month.

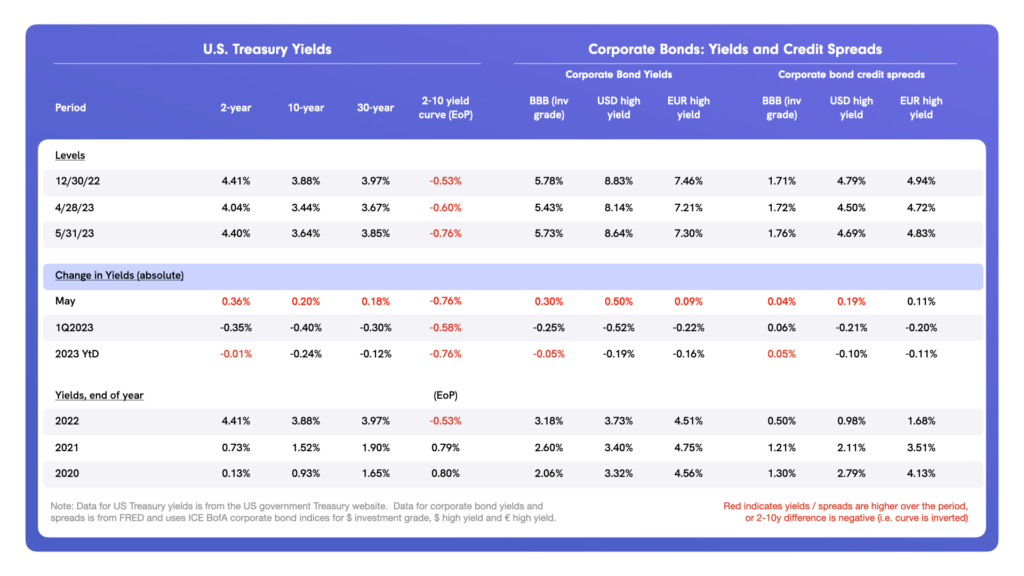

Bond Yields / Credit Spreads: U.S. Treasury yields rose during May, more severely at the short end as expectations changed throughout the month in terms of the next move by the Federal Reserve.

- The month started with expectations that – following the early May increase in the Fed Funds rate – the Fed would pause and even begin to lower its benchmark rate before year-end.

- However, economic and inflation data released throughout the month caused expectations to drift towards another potential 25bps increase in the Fed Funds rate at the next FOMC meeting in mid-June, pushing UST yields higher.

- The yield on the 2yr UST ranged from 3.75% (May 4 close) to 4.54% (May 26 close), before settling at 4.40% to end the month, a sharp 40bps increase vis-à-vis the end of April. The 2yr UST yield is more responsive to a potential change in the Federal Funds rate.

- The 2yr–10yr yield curve inversion steepened in May by 16bps, ending the month at –76 bps, its most inverted since early March and potentially signalling a higher risk of an economic slowdown or even a recession ahead.

- Both USD-denominated investment grade and high-yield corporate bond credit spreads widened in May, albeit rather modestly given the gyrations in expectations as to the direction of near-term monetary policy.

- Yields overall were wider across the credit spectrum, reflecting the increase in underlying U.S. Treasury yields during the month.

- There continues to be limited signs of a potential credit crisis at least as far as the direction of corporate credit spreads in the public debt markets, even as banks tighten their credit standards.

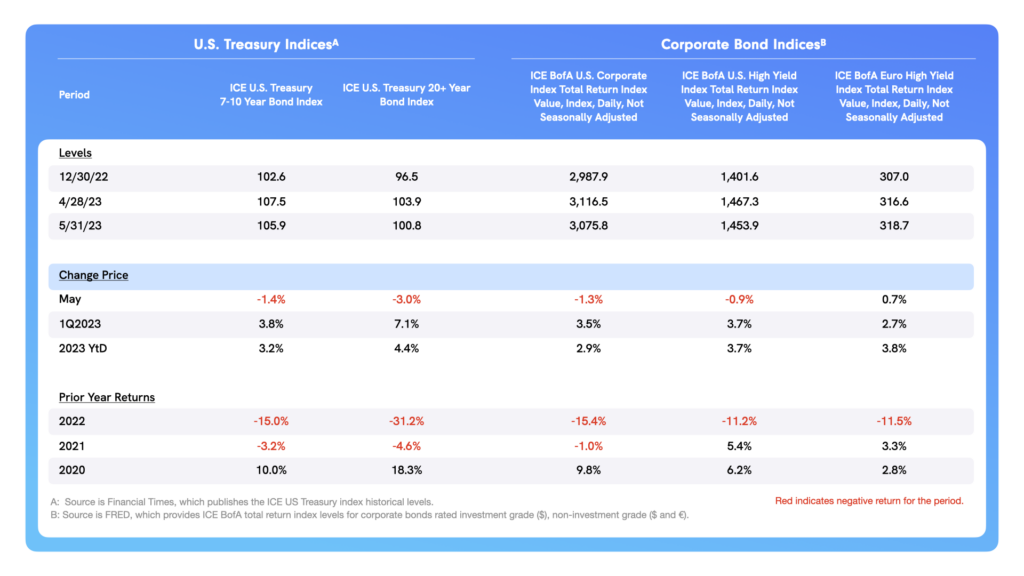

Total Returns: From a total return perspective, U.S. Treasuries lost ground in May, although both the 7-10 year total return and the 20+ year total return indices remain positive YtD following sharp losses in 2022.

- Total returns in the U.S. corporate bond market also remain positive YtD, although higher underlying U.S. Treasury yields drove modest losses in both investment grade and high-yield bonds in May.

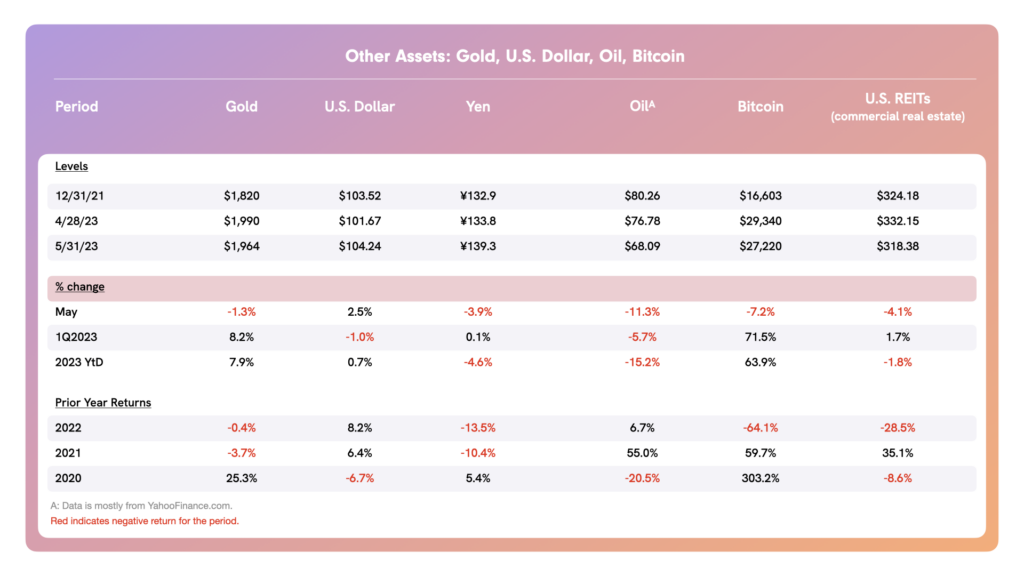

Currencies, Commodities and Alternative Assets: The U.S. Dollar gained ground in May, up 2.5% and now slightly positive YtD. The bid for U.S. Dollars has come despite uncertainties caused by debt ceiling negotiations that largely stole headlines (and not in a positive way) throughout much of the month.

- As might be expected given the diverging monetary approach of the Bank of Japan vis-à-vis other G7 banks, the Japanese Yen has continued to back off of its highs of mid-January, re-approaching ¥140/US$1.00.

- Both the Euro and the Pound also weakened in May vis-à-vis the U.S. Dollar.

- The price of WTI crude oil fell sharply in May, another potential indication that global economic growth is slowing. The price of WTI crude fell below $70/barrel for the first time since the regional bank crisis in early March.

- Bitcoin lost ground in May, not dis-similar to the direction of travel of other risk assets. Even with a disappointing month, holders of Bitcoin are sitting on an impressive 63.9% gain in the benchmark cryptocurrency YtD.

- Commercial real estate as gauged by a tracked commercial real estate ETF had a poor May, down 4.1%, continuing to reflect concerns more broadly with the U.S. commercial real estate market.

June Outlook

May brought the end of earnings for S&P 500 companies, with no significant deviations from expectations but an emerging theme built around the future influence of AI. This will continue to be a market focal point. The three key central banks – the Federal Reserve, the Bank of England and the European Central Bank – all have monetary policy meetings in early June.

- According to the CME FedWatch Tool, around one-third of market participants now expect the Federal Reserve to increase the Federal Funds rate by a further 25bps on June 14.

- This is down sharply from two or three days ago as Fed officials debate publicly the next move.

- The reality of the Fed not raising its key interest rate further is starting to better connect with the driver of such a decision, which would be slower U.S. economic growth as we move forward.

- Declining oil prices and slower growth in China are two factors that could influence near-term monetary policy.

It is unclear now exactly what the Federal Reserve might do next at the next FOMC meeting, although the probability that the Bank of England (June 22) and the ECB (decision June 15) will raise their respective key bank rates remains higher than that of the Fed, at least for now. Focus will continue to be on economic data in the U.S., Europe and China – the three economies of the world which collectively account for roughly 60% of global GDP.

About the Author

Tim Hall is a writer, speaker, blogger (emorningcoffee.com), consultant, and advisor. A former banker with 29 years of experience (buy side/sell side), Hall is also a former Independent Non-Executive Director of a U.K. “challenger bank.