Summary

Stubborn core inflation was the major theme that drove financial markets in June and much of the first half of this year. Persistently high inflation has meant that central banks in most developed markets have had to continue tightening monetary policy. Some – including the Bank of Canada and Reserve Bank of Australia (RBA) – stopped raising their policy rates, only to have to resume increasing them as inflation remained stubbornly high.

- For the first time since March 2022, the Federal Open Market Committee decided in June to pause its increases in the Federal Funds rate following 10 consecutive increases. However, Fed Chairman Jerome Powell was quick to point out to investors that – even after the June pause – they should expect one, and perhaps two, additional rate hikes at subsequent FOMC meetings.

- Although U.S. equities were characterized by some volatility at times during the first half of the year, many investors have gotten used to this new reality, seemingly prepared and relatively unphased – at least for now – by the likelihood of tighter monetary policy for longer.

- A resilient job market has added to the belief that the U.S. will ultimately achieve a soft landing with “manageable” effects on economic growth, trumping concerns about a pending recession. With this narrative gripping markets, equities rallied in the first half of the year, and the tech-heavy NASDAQ led the charge with a sizzling 31.7% return.

- Tighter monetary policy has brought some pain though in the bond market, particularly at the short end of the U.S. Treasury bond market where rates are much more strongly correlated with central bank policy rates. Fortunately, high coupons on newly-issued U.S. Treasuries have more than offset mark-to-market losses on the bonds, resulting in positive returns for bonds in the first half of the year.

- Investors cannot expect a repeat of this sort of performance in the second half of 2023, although the current euphoria might blind them to the risks that lie ahead. It is almost certain at some point that tighter monetary policy will bite, and when it does, it could bite hard.

June Themes

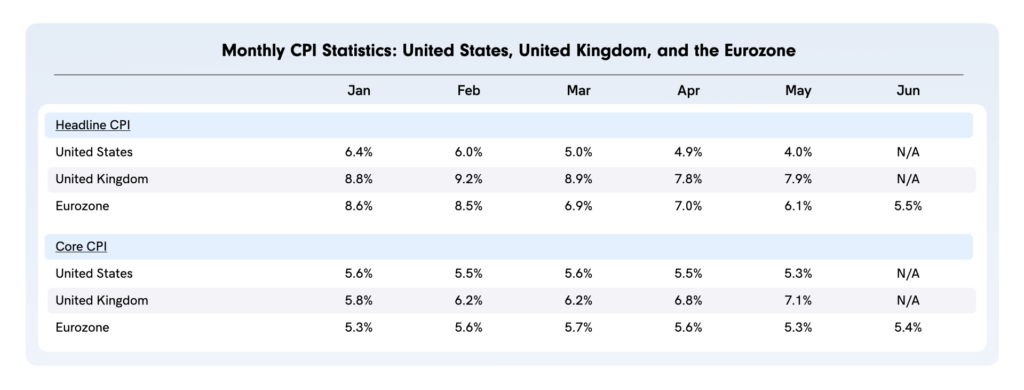

Inflation: In most developed markets, core inflation is proving difficult to rein in, a legacy of excessive monetary and fiscal stimulus during the pandemic. Although the recent trend of headline inflation has been lower in the U.S. and the Eurozone, the U.K. has not been as fortunate as inflation remains severely elevated.

- Core CPI has been trending down in the U.S. but much more slowly than the Fed desires. Even worse, core CPI ticked back up slightly in June in the Eurozone based on flash numbers released June 30, a major concern for the ECB.

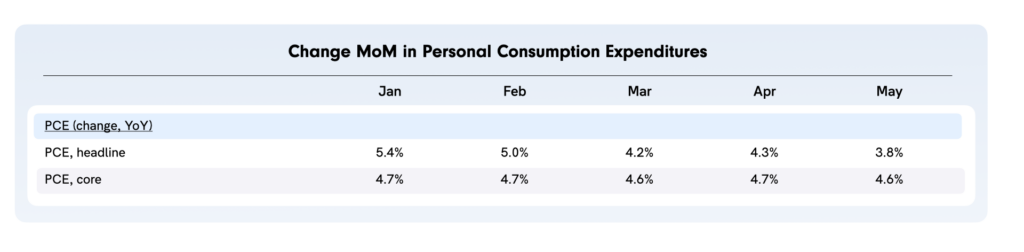

- The Fed’s preferred measure of inflation – the change in Personal Consumption Expenditures (PCE) – has also been trending lower. May headline PCE and core PCE was 3.8% and 4.6%, respectively, although as seen in the table below, the change in core PCE has been nearly stable the first five months of this year. This sort of “sticky inflation” is not what the Fed wants to see as it strives to get back to its target inflation rate of 2%/annum.

Central banks hike rates: Central banks in many developed economies raised their key overnight bank policy rates in June, even as the Federal Reserve paused. These included the Bank of England, the European Central Bank (Eurozone), the Swiss National Bank, the Reserve Bank of Australia, the Bank of Canada, the Norges Bank (Norway) and the Riksbank (Sweden).

- Fed officials were clear following their decision to pause in June that two further rate rises were likely before reaching the terminal rate, with the first such increase (of 25bps) likely to occur at the next FOMC meeting on July 26.

- The Fed is not alone, as the ECB has “penciled in” a further 25bps increase in its three key bank policy rates at its next monetary policy meeting on July 27, and the Bank of England – which remains in a very precarious position as far as inflation – will certainly raise its overnight Bank Rate by 25bps or perhaps more at its next monetary policy committee meeting on August 3.

Commercial real estate: The U.S. commercial real estate market remains under scrutiny as lenders, regulators and rating agencies prepare for the worst. The issues include:

- fewer people working in offices (and more from home), a pandemic legacy;

- higher interest rates as the Fed tightens monetary policy; and

- slower economic growth, most pronounced in the manufacturing sector at the moment.

U.S. commercial banks hold approximately 50% of all commercial real estate debt according to Moody’s Investors Service in a report it published in mid-June. The FDIC has also shared its concerns in a paper it published on June 23, Commercial Real Estate Weakness Likely to Pressure Bank Loan Portfolios.

OPEC+ curtails supply: OPEC+ announced on June 4 that it would reduce its daily supply of oil by one million barrels/day starting in July, a reduction borne solely by Saudi Arabia, in order to provide a floor under declining oil prices.

- The effect on oil prices was initially muted, but as economic data continued to suggest a resilient global economy during the rest of the month, the price of oil firmed during June and actually ended the month slightly higher.

Cryptocurrencies: Early in the month, crypto brokerage firms Binance and Coinbase both came under increased scrutiny from the SEC for trading crypto assets that – according to the SEC – should have been registered as securities.

- Bitcoin, as well as other cryptocurrencies, felt the pressure as prices declined.

- However, Blackrock announced in mid-June that it had filed a spot Bitcoin ETF with the SEC, a move soon followed by other asset management firms including Fidelity Investments. The SEC has not approved these spot ETFs, but the announcement alone by Blackrock led to a sharp rally in the benchmark cryptocurrency.

Asset Class Performance

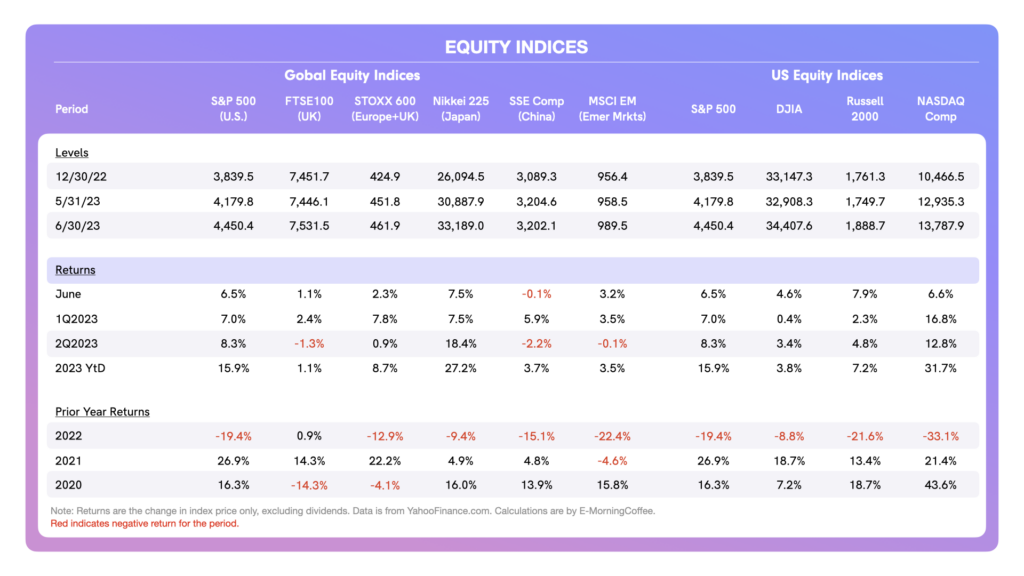

Global Equities:All of the country indices tracked were positive in June with the exception of the Shanghai Index, which posted a slight loss. All of these equity indices ended the first half of 2023 in positive territory, a sharp reversal from their dismal performance in 2022.

- Year-to-date (YtD), the best performing equity markets have been in the U.S. and Japan. The Nikkei 225 has risen a remarkable 27.2% this year, fueled by the accommodative monetary policy of the Bank of Japan. Japanese equities are also less expensive vis-à-vis equities in the U.S. and Europe using most trailing valuation metrics.

- Chinese equities have disappointed this year. As its largest component, the poor performance of Chinese equities has also negatively affected returns on the MSCI Emerging Markets Index, even though the benchmark emerging markets index has eked out a positive return YtD. The culprit in China is the economy, which seems unable to really get going.

US Equities: Stateside, the best performer this year has been the NASDAQ Composite. Following a horrific 2022 in which the index was down 33.1% for the year, the tech-heavy index has turned completely around, generating an amazing return of 31.7% in the first half of this year.

- Through the first several months of the year, the major U.S. equity indices – including the S&P 500 and the NASDAQ – were heavily (and positively) influenced by stellar returns on the so-called “magnificent seven” tech giants (Apple, Amazon, Alphabet (Google), Meta Platforms (Facebook), Nvidia, Tesla and Microsoft). However, the rally began to accelerate and broaden in June, especially towards the end of the month, to include a more diverse group of sectors and stocks.

- Volatility as measured by the VIX (the so-called “fear index”) dropped below 15 the second week of June, and has remained at a very low level since then, closing the month at 13.59. Volatility remains muted as investors embrace risk.

Bond Yields / Credit Spreads: U.S. Treasury yields increased (again) in June, more severely at the short end of the yield curve even though the Fed “paused” its increases in the Federal Funds rate at the most recent FOMC meeting. Although the Fed paused, Fed officials have made it clear that one or two additional rate increases are likely this year, with the next increase of 25bps expected at the late July FOMC meeting.

- Yields at the short end of the yield curve, much more influenced by and correlated with the Fed Funds rate, headed higher following the rhetoric on further monetary policy tightening coming from Fed officials.

- Investors now seem “comfortable” with two further increases in the Fed Funds rate, as well as with a higher terminal rate that might be in place through the end of 2024. By “comfortable”, this means that risk markets are no longer rattled by this reality and – as a result – are aggressively adding risk.

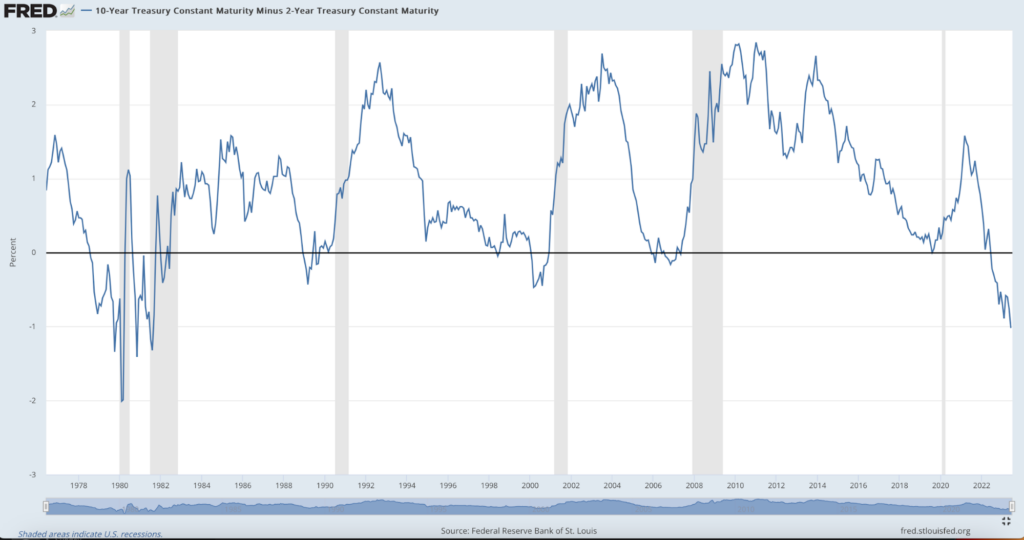

- Although comfort with monetary policy seems priced in, the yield curve inversion steepened sharply in June. The inversion suggests that slower U.S. economic growth lies ahead, but so far, this prognostication seems to be continuously pushed out and is now having limited influence on risk investors. Nonetheless, it is interesting to note that the 2yr-10yr yield difference closed the month at negative 106bps, the highest level (bar a short period in early March during the bank crisis) since the early 1980s, as you can see in the graph below from FRED.

- Corporate credit markets remain unphased by concerns over slowing economic growth, with credit spreads tightening during June in both investment grade and high yield. Even with bank lending parameters tightening and credit standards becoming more stringent following the bank crisis in March, institutional investors are increasingly comfortable with corporate credit across the investment grade-high yield spectrum.

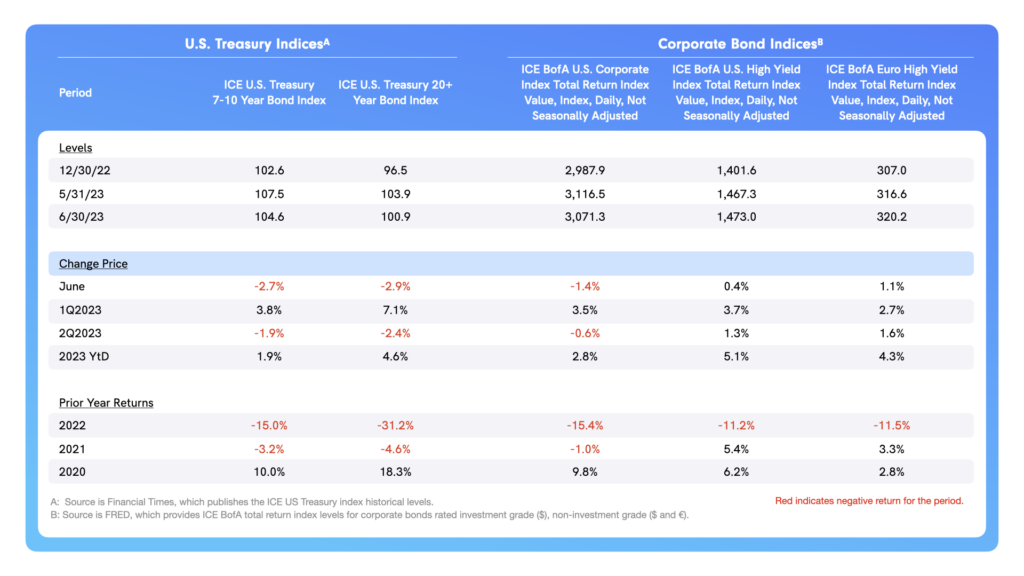

Total Returns: From a total return perspective, U.S. Treasuries lost ground again in June and were negative for the second quarter. Nonetheless, both the 7-10 year total return and the 20+ year total return indices remain positive YtD, with capital losses on bonds caused by higher yields more than offset by higher coupons on U.S. Treasury bonds.

- Total returns in the U.S. corporate high yield market are positive YtD, even with yields on underlying U.S. Treasuries heading higher.

- Investment grade bonds have lower spreads, and hence, were unable to completely absorb the higher U.S. Treasury yields in June and throughout the second quarter.

- Nonetheless, both investment grade and non-investment grade bonds have generated positive returns YtD.

Currencies, Commodities, and Alternative Assets:

- Although the U.S. Dollar weakened slightly in June, it has remained reasonably resilient through much of the year, down only marginally. Most pundits believe that the Dollar remains vulnerable vis-à-vis the Euro and Sterling, as both the ECB and Bank of England (the latter especially) remain behind the Fed as far as their tightening efforts.

- The Japanese Yen continues to weaken as the Bank of Japan stands still, even as its G7 central bank brethren have increased their policy rates to combat stubborn core inflation. As a result, the Yen is now down nearly 8% YtD and appears to be on a trajectory heading back towards ¥150/$1.00, a threshold only breached once (in October 2022) since 1990.

- The price of WTI crude oil rose in June, perhaps boosted modestly by the OPEC+ decision in early June to further curtail supply.

- Bitcoin resumed its rise in June, fueled by improved risk sentiment and – at the end of the month – announcements by Fidelity and Blackrock, among others, that they were looking to establish spot Bitcoin ETFs.

- In spite of investor and rating agency concerns about commercial real estate, the broader real estate market chalked up gains in June, largely off the back of broader gains in U.S. stocks towards the end of the month. This brings real estate into positive territory for the first half of 2023, trailing the broader equity indices but nonetheless in positive territory.

July Outlook

June was a strong month for risk assets but a more difficult month for government bonds at the short end of the yield curve.

- It appears now that investors have priced in further rate increases in the U.S., the U.K. and the Eurozone, as well as a longer period once the terminal rate is reached. This reflects the difficulty central banks are having in addressing core inflation.

- Assuming there are fewer surprises in this respect going forward, attention will not return to central bank actions until later in July, with the Fed, ECB and Bank of England all delivering their next round of monetary policy decisions starting the last week of July.

- In the meantime, investors will be focused on second quarter earnings of S&P 500 companies, which start on July 14 with the “big six” U.S. banks releasing earnings. The tech giants aside from Nvidia all release their earnings the latter half of July, and their results will undoubtedly drive sentiment as we head into the traditional summer lull and the lower-volume month of August.

About the Author

Tim Hall is a writer, speaker, blogger (emorningcoffee.com), consultant, and advisor. A former banker with 29 years of experience (buy side/sell side), Hall is also a former Independent Non-Executive Director of a U.K. “challenger bank.” He currently resides in London.