This article is the third part of a series on alternative investments. Read the first and second parts.

Alternative investments do not simply differ from traditional investments by being less liquid and offering lower correlation. Their entire makeup, portfolios, and methods of valuation are all markedly different from that of stocks and bonds. Thus, investors may find they have a bit of a learning curve as they embark on diversifying their portfolios with alternative investments. Common questions include: How do the asset types within the alternatives world work? And what features do they offer that differ from those of stocks and bonds?

Alternative assets are complex, but this article provides an overview of several different alternative asset classes. Of course, investors should always be aware that, depending on the asset class, historical information may not be readily available and its reliability might not be certain.

Private Equity

As an alternative asset class, private equity funds are the most well-known. Yet historically, access to these investments has been largely restricted to institutional and some high-net-worth investors.

Private equity can be defined quite broadly; for example, it can include equity used to finance the acquisition of companies using primary debt capital. Recently, mandates have been expanding and some private equity funds now have raised funds focused on private credit and infrastructure debt financing.

Moreover, many of the largest firms (e.g., Apollo, KKR, Blackstone, and Carlyle) have listed their management companies. The management company in each case is the top umbrella company of private equity firms which houses the senior management team. Each fund (and there can be many funds of different vintages and strategies) is a component of the management company. The listing of the management companies provides investors in the listed companies with greater transparency into the firm’s operations, fee structures, and – in particular – historical returns of the various funds. While far from perfect, the improved transparency has provided much deeper insights into the performance and risk factors associated with private equity as an alternative asset class.

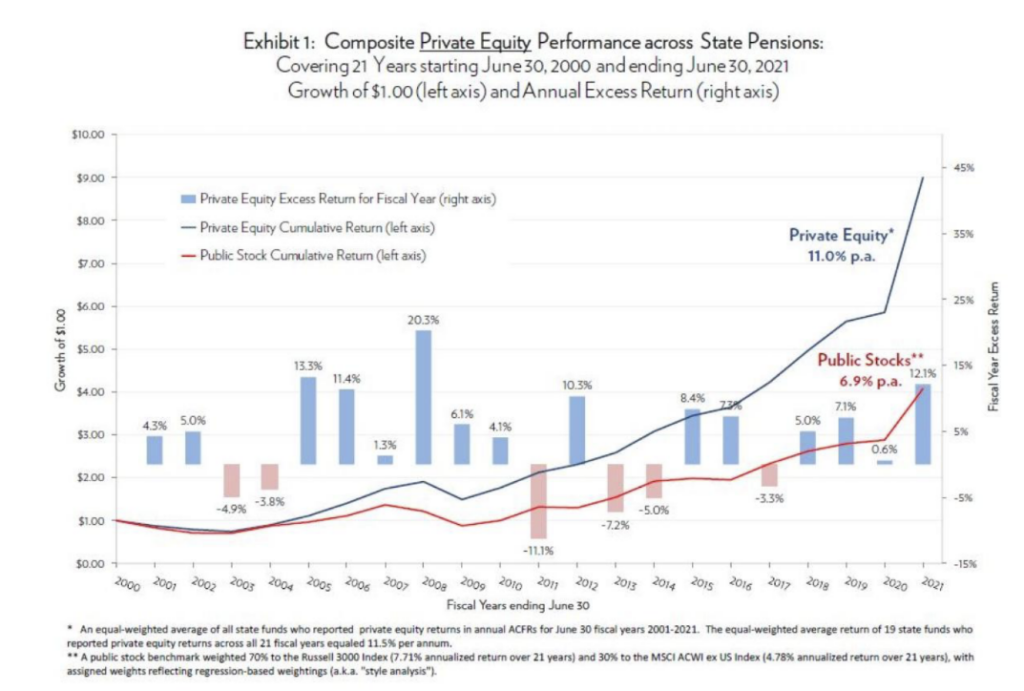

Although the transparency has improved, the calculation of historical returns in private equity is replete with inconsistencies. This not only makes it difficult to piece together a viable long-term performance record, but also makes it challenging to compare performance records from firm to firm. As depicted in an article written by Stephen L. Nesbitt, Chief Executive Officer and Chief Investment Officer of Cliffwater LLC, private equity has shown a significant uplift on annual returns vis-à-vis public equities since 2020.

Mr. Nesbitt noted that not only have private equity firms outperformed public stocks by 4.1% per annum, but also that the industry has had a lower standard deviation than public stocks, demonstrating why private equity fund investing has had such strong support from institutional investors over the years. Unfortunately, this asset class is rarely open to individual investors.

Private Credit

The growth of private credit (or private debt) funds accelerated after the financial crisis of 2008-2009 following the near systemic collapse and government rescue of the U.S. banking system. To help avoid a similar catastrophe in the future, banks were forced to increase their capital base and risk-weight their assets (mainly loans), which significantly curtailed their lending capacity.

This left a void that was filled by private credit funds active in direct lending, further disintermediating banks. These direct lending funds also provided institutional investors with an opportunity to invest indirectly in high-yield loans, a market which had previously been off-limits to them because they could not directly lend to companies.

Credit (debt) funds lend directly to middle-market companies, both on a stand-alone basis and to fund leveraged buyouts. While these direct lending funds have not been tested in a prolonged economic downturn (aside from the short pandemic-driven recession), the general belief is that the combination of stronger covenant packages and better asset coverage should allow private credit funds to withstand economic stress reasonably well.

As the investor appeal of private credit funds has increased, so too has the interest of individual investors in lending directly to small- or middle-market companies. In many cases, the borrowers are smaller companies that are relatively early in their evolution. The debt financing might be considered higher risk, but the loans normally have short maturities and can be very well secured with collateral. They may also offer attractive returns.

Importantly, these smaller high-yield loans are available now to retail accredited investors. Companies like Percent have been at the forefront of developing this market, which matches the needs of companies seeking debt financing or the fintech lenders who help fund growth, with investors seeking higher returns and diversification.

Fine Art

Most fine art is genuinely unique, as only one original exists, and the fine art world is often opaque. Although there are millions of paintings and sculptures, only a handful of artists reach cult status with works that generate lofty prices in the secondary market. Many of the most precious works of art are owned by museums, and those that are privately held are rarely (if ever) offered for sale.

Fine art is clearly a bespoke, one-off market, with auction sales from leading artists catching headlines. However, these sales are not representative of the art market more broadly. In fact, actual returns on fine art are inconsistent from one source to another although, generally speaking, it seems that some sub-segments of the fine art market (like contemporary art) have outperformed others.

Fine Wine

Fine wines can be purchased and obtained on an individual case basis, usually using futures contracts for the just harvested but not-released finest wines known as en primeur.

Similar to other passion assets, collecting wine can be rewarding and educational, but returns over time depend very much on what you choose to purchase and hold. This includes the region, vineyard, and vintage, but also factors such as the wine’s provenance or storage history. The advent of wine indices has been a welcome development for understanding performance, recognizing that liquidity and price transparency in the underlying assets is still rather imperfect. Investors who are interested in wine as an asset class but do not wish to go to the trouble of sourcing and storing individual cases can hire a company to create cellars for them. This option makes fine wine a more readily available alternative asset class for retail investors.

Other ‘Passion’ Assets

As the name suggests, passion assets have intrinsic value in terms of ownership beyond whatever they might be worth “on paper.” For individual investors, the investments are often made for intangible reasons beyond pure monetary appreciation.

It is difficult to source historical return data for passion assets like coins, stamps, sports memorabilia, vintage watches/jewelry, and classic cars. These assets – similar to precious metals, fine wine, and fine art – do not generate an income stream per se. Without reliable historical return data, it is impossible to draw conclusions about returns or understand correlations with traditional asset classes.

An Alternative Allocation

Alternative assets should be considered by investors interested in more portfolio diversification and the potential for generating higher overall portfolio returns. For individual investors, professional wealth managers often recommend that between 5 – 10% of portfolios be invested in alternative assets. However, as discussed earlier, some asset and wealth managers suggest a higher percentage of alternative assets – up to 20% – depending on the investor’s tolerance for risk and need for liquidity.

It is important to remember that alternative assets are not without risk on a stand-alone basis, as they are generally difficult to price, expensive to buy or sell, and are often illiquid, meaning an investor might have to wait months or years to sell them. For accredited investors seeking to diversify beyond the traditional world of stocks and bonds, alternative investments could be a difference-maker in long-term strategies, providing gains apart from traditional markets.

Broadening Access to Alternative Investments

Unlike some types of alternative investments, private credit transactions on the Percent marketplace have a low cost of entry and variable tenors. With an average duration of 9 months and refinancing or calls happening in as little as one month, investors maintain the flexibility to redeploy their capital as market conditions evolve. Further, many deals have a minimum participation threshold of $500; this low threshold gives investors the chance to participate in multiple deals at the same time to further diversify their portfolios.

Percent has eliminated one historical barrier to private credit investing with a marketplace that prioritizes transparency and discovery. It’s easy to find and compare transactions on the marketplace, get detailed fundamentals on borrowers and historical performance, and establish participation parameters. Once the deal has closed, performance can be monitored right on the portal, with real people available to help by email or phone if needed. That’s how Percent makes private credit markets more transparent and accessible, benefiting investors and all market participants.

Read part one of this series, An Introduction to Alternate Investments, and part two, Alternative Investments and Asset Correlation.