This portfolio split is recommended for good reason, as it has consistently delivered an attractive return for investors.

The essential benefits of this strategy start with the often favorable returns delivered by both equities and fixed income over the long term. However, achieving those returns generally requires investors to absorb varying degrees of volatility in the value of their investments. Typically, an equity portfolio experiences volatility as the economy expands and contracts. Likewise, a fixed income portfolio experiences volatility as the Federal Reserve’s monetary policy becomes more restrictive or accommodative in response to those economic expansions and contractions. You can think of it in terms of physics – for every action, there is an equal and opposite reaction.

Historically, equity portfolios have increased in value during an expanding economy while fixed income returns may diminish, given the corresponding monetary contraction by the Fed that is intended to curb inflationary pressures arising from that economic expansion. However, the opposite generally occurs – as the economy goes through cooling periods, investors may experience diminished equity returns which can be offset with better fixed income performance driven by a more accommodative Fed response to those economic conditions.

Over time, the 60/40 portfolio mix has demonstrated two very attractive features. First, it takes advantage of attractive long-term returns from both the equity and fixed income markets. Second, it decreases overall volatility in aggregate portfolio value, since the respective volatility in the portfolio value of the equity and fixed income components tend to offset each other.

A change to the balancing act?

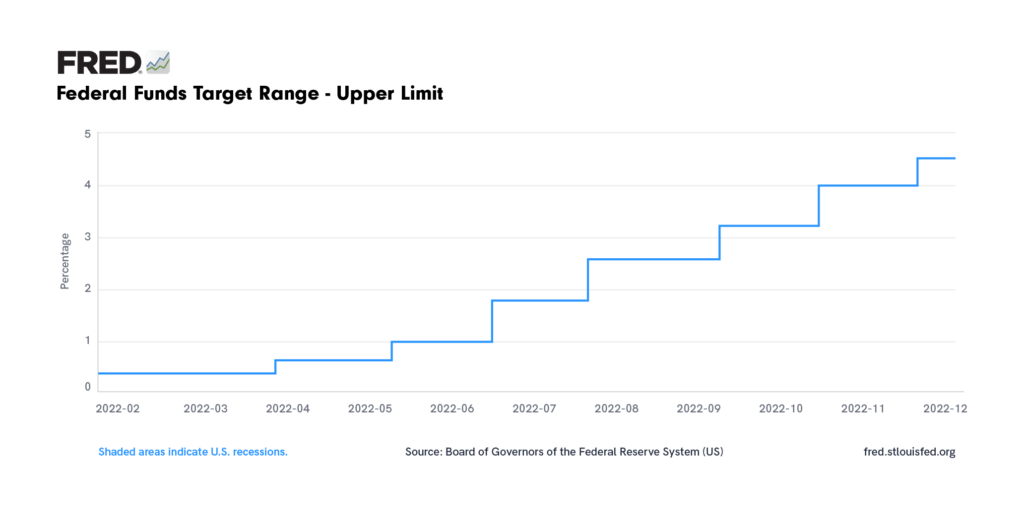

Over the past decade, a breakdown of this counterbalancing effect between equity returns and fixed income returns has occurred. Throughout most of this period, in fact, there were steady increases in value for both components of the 60/40 portfolio. This was due to an unusual combination of factors including a low inflation rate, low real interest rates (actual rates minus the inflation rate), and an extremely accommodative Fed. Entirely without precedent, for almost the entire period 2009 – 2021 the Fed maintained a so-called “zero interest rate policy” which led to steady gains in value for fixed income assets as 10-year US Treasury rates dropped from approximately 4% down to a low near one-half of 1%. These fixed income gains were coupled with equity market gains that were principally driven by modest but steady economic growth (2 – 2.5% annual GDP) and inflation rates that consistently remained within the Feds 1-2% targeted range. Investors often clearly benefited from the simultaneous improvement in both equity and fixed income returns over this period, and given the duration, may have thought those conditions would persist. However, the factors noted above have begun to unwind: The S&P 500 ended 2022 down approximately 19% from its highest point one year earlier. Concurrently, the Fed unexpectedly embarked on an aggressive rate hike program raising the Fed Funds rate by 425 basis points over the course of 2022.

https://fred.stlouisfed.org/series/DFEDTARU

Concurrent falling returns from both of these market sectors have given investors whiplash. As a result, they are questioning the validity of continuing in a 60/40 portfolio mix, or whether (and how) it might be possible to improve upon that strategy.

Are alternatives an alternative?

Alternative investments can offer an opportunity to rebalance portfolios away from the long standing 60/40 portfolio composition, while also potentially enhancing diversification. To gain a clearer picture, let’s look at the relationship between expected returns and credit risk.

- In a 60/40 portfolio, the fixed income component generally has lower credit risk than the equity component. Fixed income investments are typically a mix of U.S. government notes and bonds (considered to be ‘risk free’) and municipal and corporate bonds (generally deemed ‘investment grade’ as they are on the higher end of the credit risk rating scale)

- Equities, however, almost always have a lower priority of payment for a corporation than its fixed income notes and bonds. So, even if a corporation has an investment grade rating, its equity has higher credit risk than its fixed income obligations. For corporations with a lower than investment grade rating, the credit risk is higher than the typical fixed income investment in that portfolio.

Certain alternative investments such as private credit straddle the risk and return characteristics of the equity and fixed income markets. Like a typical fixed income investment, these alternatives have a stated interest rate and redemption date. However, their credit risk is more like an equity investment, since the priority of payments for the obligor will typically place other items ahead of the alternative investment obligation.

This nexus helps to demonstrate how alternatives can play a complementary role within a portfolio. Although they share many of the structural characteristics of traditional fixed income investments, the stated and expected return for an alternative investment is typically higher as it reflects a more equity-like credit risk profile. It is this unique combination of risk and return that can benefit investors who add alternative investments to their portfolio mix.

Further, investor understanding and acceptance of alternative investments has grown significantly. A recent industry study1 from CAIS and Mercer showed that, among the various asset classes within this market, private credit is perceived as being one of the safest choices. Further, that study indicated that a majority of investors that were polled now favor adding new products and structures into their portfolios. Nearly 9 in 10 financial advisors plan to increase alternative allocations over the next two years.

https://info.caisgroup.com/state-of-alternative-investments-in-wealth-management

Although the 60/40 portfolio has historically provided a more stable portfolio value, it historically comes at a cost. Investors have to expect that long-term portfolio returns will be reduced when fixed income investments are added to provide stabilizing benefits to the portfolio’s overall value.

However, as recent events have shown, investors can no longer be confident that equity and fixed income markets will move in opposite directions to provide expected offsets. The lack of those traditional stabilizers leaves investors searching for adjusted allocations. Interest rates for traditional fixed income assets typically have a very strong positive correlation to movements in the Fed Funds market and with movements in long-term U.S. Treasury rates. Private credit offerings, however, are generally less interest rate sensitive. These offerings typically have relatively higher stated interest rates that are more reflective of expected returns for a broad set of investment options. As such, there is a strong case for adding alternative investments; they could improve portfolio returns and offset volatility in portfolio value. Furthermore, they give investors access to a diversified set of obligors which can help to limit credit risk.

Investors may want to consider setting aside a percentage of their portfolio for private credit and other alternative investments. That percentage could increase in correlation to the growth of the private credit market vis-a-vis equity and fixed income markets, giving investors more balanced access to diversified investments while reducing correlation.

How can investors find opportunity?

The private credit markets were traditionally viewed as opaque and often off-limits to all but the biggest institutional investors. No more. Percent has brought borrowers, underwriters, and investors together in a private credit marketplace, making it easier to source, syndicate, and participate in transactions. Innovative technology and a combination of low investment minimums and exceptional transparency make it easy for institutional and retail accredited investors to view and compare transactions, fund accounts, and invest. With access to all onboarding documents and financials, plus proprietary surveillance reports, investors can stay informed about the ongoing health of a borrower and monitor their investment.

1https://info.caisgroup.com/state-of-alternative-investments-in-wealth-management