This article is the third and final part of a series on the history of private credit investing. For access to the first article in the series, click here.

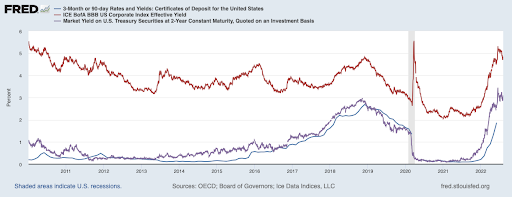

The decade of 2010-2020 was characterized by the use of unconventional monetary policy by the Federal Reserve, which resulted in interest rates remaining at record-low levels for much of the decade. As a result, investors – especially retail investors – found it difficult to find debt alternatives that offered any sort of reasonable yield unless they were able to invest for long periods or take on substantially more risk (or do both). Certificate of Deposit (or “CD”) rates remained anchored near zero, and yields on investment-grade rated corporate bond funds were rather meager, too, as you can see in the graph below from the Federal Reserve Economic Data.

This opened the door for new short-term debt alternatives to appeal to retail investors as the decade wore on.

Crowdfunding

Crowdfunding is when companies raise financing from a group of retail investors, or a “crowd”. This financing technique is essentially peer-to-peer, since a group of investors is providing equity or debt financing directly to a company. Crowdfunding in one form or another was believed to begin in the late 1990s or early 2000s, but it really didn’t come into prominence until after the Great Financial Crisis.

In 2012, President Obama signed the Jumpstart Our Business Start-ups (“JOBS”) Act into law, which made it easier for companies of different types to raise funding through crowdfunding. Some of the early equity crowdfunding platforms included Fundable, Kickstarter, Seedblink, Crowdcube, Seedrs, Republic (currently acquiring Seedrs), and CrowdStreet, among others. As crowdfunding developed into an important equity-raising alternative for early-stage companies, it also spawned other companies around the periphery that assist entrepreneurs with the important aspects of their first financing foray, including mentoring/coaching, writing pitch books, developing business plans, and hiring competent staff.

Crowdfunding had great appeal to start-up companies, so it is not surprising to see debt financing for smaller companies adopt similar methods of raising capital and investments, albeit on a different level.

Private Credit Investing

Private credit investing, the most recent iteration of the expanding private debt market, saw dedicated platforms connect smaller borrowers looking for debt financing with both retail and institutional investors seeking short term, high yielding assets. . These opportunities involve a potential borrower providing details of its business and the amount it seeks to raise on one of several recognized private credit platforms (including Percent), which would first have to approve the listing of the company and its capital raising on its platform. Once the company undergoes due diligence and a strict vetting process, it is listed on the platform, where investors are able to subscribe to the transaction if it meets their investment criteria.

Though equity crowdfunding is one of the more popular forms of alternative investing (at least in terms of mentions in financial media), a number of prominent platforms focused on private credit have also emerged that have become crucial for companies at the early stage of their evolution. These platforms include Percent, Funding Circle, Upstart, Lending Club, amongst others. The evolution of this market opened the door for smaller companies that might have either tapped out their bank financing or are not qualified for bank-based credit. Private credit investing provides early-stage companies with another non-dilutive option to traditional bank financing while providing access to retail and institutional investors (and vice-versa), especially as both investor classes seek higher yields in a volatile, inflationary, and potentially recessionary environment.

Percent is the Way Private Credit Works

Percent’s platform gives investors access to a wide variety of high-quality alternative investment opportunities, making it simple to find, evaluate, and invest in private credit transactions. Investors can easily discover and compare deals and terms while viewing borrowers’ underlying financials and illuminating information supporting each offering.

With 32 borrowers and counting, Percent offers multiple structures to diversify across borrowers and sectors. This gives investors multiple opportunities to invest in everything from asset-based notes (supported by consumer loans, SMB financing, and other asset classes) to corporate loans, which allow investors to add high-growth companies to their portfolio.

Learn more about how Percent’s private credit investments can help your portfolio today.