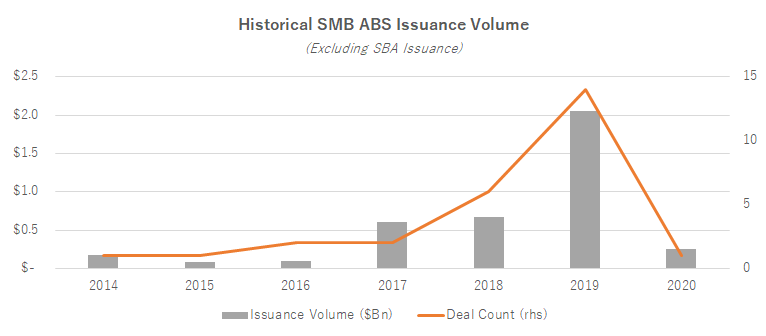

As a byproduct of traditional financial institutions taking a step back from small business lending, a cohort of new, non-bank originators arose following the global financial crisis to serve the financing needs of small and medium sized businesses (SMBs) outside the scope of the U.S. Small Business Administration. As a means to sustain this market growth, the non-SBA SMB asset-backed securitization (ABS) market has organically developed, with issuers, such as OnDeck Capital, Funding Circle, Kabbage, Kapitus and others, regularly tapping the term securitization market since 2014.

With 2019 seeing over $2 billion in issuance, 2020 was expected to be a robust year for SMB securitizations, as several newer issuers were expected to further ramp their programs and funding needs. While January saw one transaction for $252 million from Funding Circle, the landscape dramatically changed as the COVID-19 pandemic took hold towards the end of the first quarter. With the widespread shutdown of economic activity across the country accelerating in April, the small business sector experienced significant stress through forced closures, supply-chain disruptions, and employee absences.

To provide relief for the sudden economic shock experienced by businesses and their employees, Congress signed into law the CARES Act in late March 2020. The CARES Act established the Paycheck Protection Program (PPP) authorizing up to $659 billion, disbursed through the Small Business Administration, allowing businesses to fund up to eight weeks of payroll costs and ongoing operating expenses such as interest on mortgages, rent, and utilities. Through the unprecedented direct aid from the PPP, small businesses were able to keep employees on the payroll and resume their operations at a faster clip as lockdown restrictions eased in the Summer months. As of August 2020, the SBA deployed over half a trillion dollars to over 5 million businesses across the country.

Because of widespread interruption in economic activity resulting from Coronavirus, the small business sector continues to face significant headwinds. With the capital markets largely closed to new issuance and traditional capital providers reducing warehouse lending, many SMB finance lenders were forced to curtail or halt new originations in H1 2020. As a result of deterioration in performance, many increased their collection capabilities through improved technology and additional collectors, as well as retooling their origination engines and underwriting criteria, with a focus on essential businesses that fared well during the pandemic.

As result of the negative economic implications and the government mandated business closures, in March 2020, Kroll Bond Rating Agency placed all of its 10 U.S. SMB securitization transactions ($2+ billion in outstandings) on Watch Downgrade. Similar actions were taken by DBRS Morningstar. As collateral performance data began to trickle in, these actions were merited as early stage delinquencies on SMB ABS dramatically increased in April and May. Overall collateral performance worsened on outstanding securitizations, ultimately triggering early amortization events across many transactions.

To provide additional protections to bondholders, ABS structures typically employ an early amortization feature, where all collections from the underlying assets are used to repay existing notes in order of seniority, triggered upon significant deterioration in collateral performance.

In SMB ABS, these features are often pegged to the collateral pool’s average yield, excess spread, delinquency levels, and required reserves. For example, on May 7th, an early amortization event occurred with respect to OnDeck’s ABS (ODAST) as a result of an asset amount deficiency in that series. While the eventual shock of the pandemic gradually subsided and the large stimulus programs had their desired effect, a material portion of the delinquent and defaulted receivables in the ODAST transactions continued to make partial or full repayments. As the structure remained in rapid amortization, a significant amount of deleveraging occurred between April 2020 and October 2020, ultimately allowing DBRS Morningstar to remove its Under Review status for the subordinate tranches, with all notes fully repaid in December 2020.

While 2020 was certainly a challenging year for small business and the SMB finance industry, the government’s swift implementation of PPP proved a saving grace for many vulnerable businesses across the U.S. While the SMB ABS market suffered a deadening blow following the initial wave of the pandemic, the securitization structures proved durable, providing adequate protections for bondholders and the basis for the SMB market to re-emerge stronger after the pandemic subsides.