Percent was founded on a premise that we consider vital for the ongoing development of the private debt markets: transparency.

As our platform has grown and partnered with more borrowers that operate within different industries, utilize different financing instruments, and ultimately serve different market segments, the data and performance metrics that each borrower manages and monitors has increasingly varied. In an effort to help investors monitor and compare performance across different notes, we have recently introduced our Surveillance Reports.

As part of our own diligence and internal risk management framework, we were already analyzing many of the metrics included in these reports. However, the recent global events accelerated our efforts to prepare these reports for many of our borrowers. Once we saw the value these reports provided internally, we quickly made them available for investors on the platform. The structure and format of each surveillance report has been agreed upon with each borrower, and the Percent team prepares these with the periodic loan tapes that are made available to us.

Our goal is to provide surveillance reports for most, if not all, of our Short Term Note Programs (STNPs) by the end of Q2 2020. However, given the structure of some of our STNPs, due to either the frequency of payments, concentration of underlying assets, or otherwise, some surveillance reports might be less indicative of asset-level performance and more focused on portfolio-level demographics. In either case, we will strive to provide reliable information that is intuitive to grasp, comparable across similar asset types and continuously improved upon in our pursuit of full disclosure.

How to Interpret the Data

Days Past Due Analytics

- Days Past Due: Days past due defines how many days a borrower is late on their payment according to the assets’ underlying payment schedule. Days past due is calculated by first deriving the daily accrual per loan or advance, or in simpler terms, how much on average each loan or advance is supposed to pay on a daily basis. Then, the daily accrual is multiplied by the existing tenor of the loan to understand the total amount each loan or advance should have paid back by the date of the report. The total expected payment is then compared to the actual amount that has been paid back to determine if there is any shortfall. If there is a shortfall, days past due is calculated per asset by dividing the total shortfall over the expected daily payment. For example, suppose there is a loan that has a daily payment of $100 and matures in 100 days. If day 10 has just ended and the loan has paid back only $700 instead of $1,000, the underlying borrower is 3 days past due. It is important to note that the payment frequency of each underlying loan, such as daily, weekly, or monthly payments, is accounted for when calculating days past due.

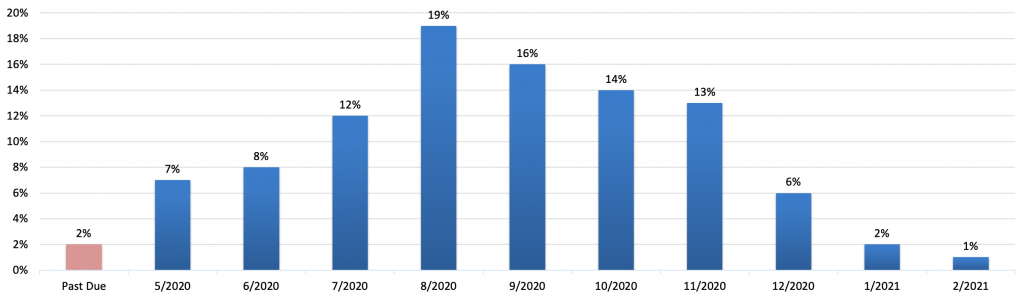

- In the above example, 91% of payments are current, or on time, while 6% are between 2 and 30 days past due with 1% of payments being between 31 and 60 days past due. Days past due analytics are provided in order to illustrate the overall health of the underlying loans of each borrower and/or note. Where applicable, each surveillance report also includes a breakdown of days past due by industry and state, province, or country. By doing so, investors can uncover any correlation between payment delinquencies and industry or geography. On a weekly basis, the report also displays a historical lookback at days past due, which is intended to provide insight into any upward or downward trends in underlying payment delinquencies.

Portfolio Concentration Analytics

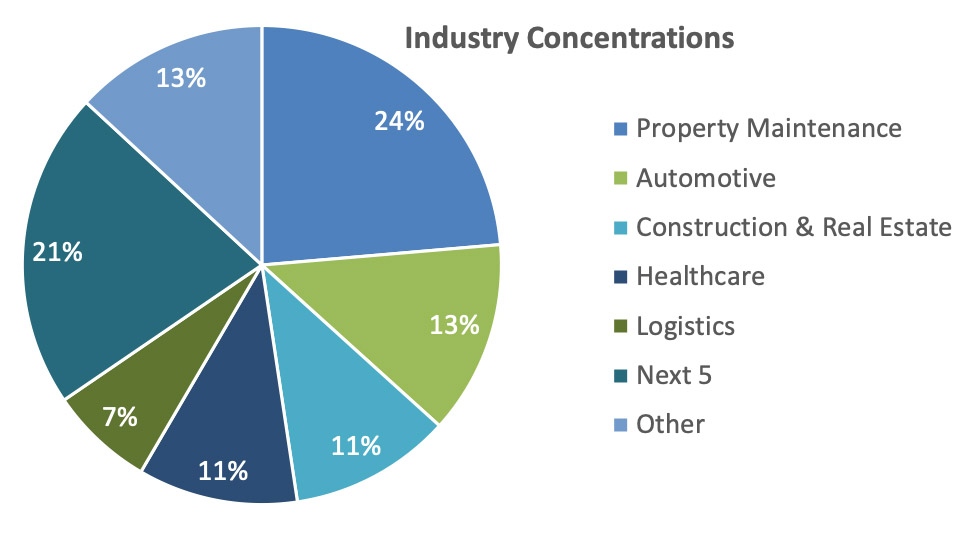

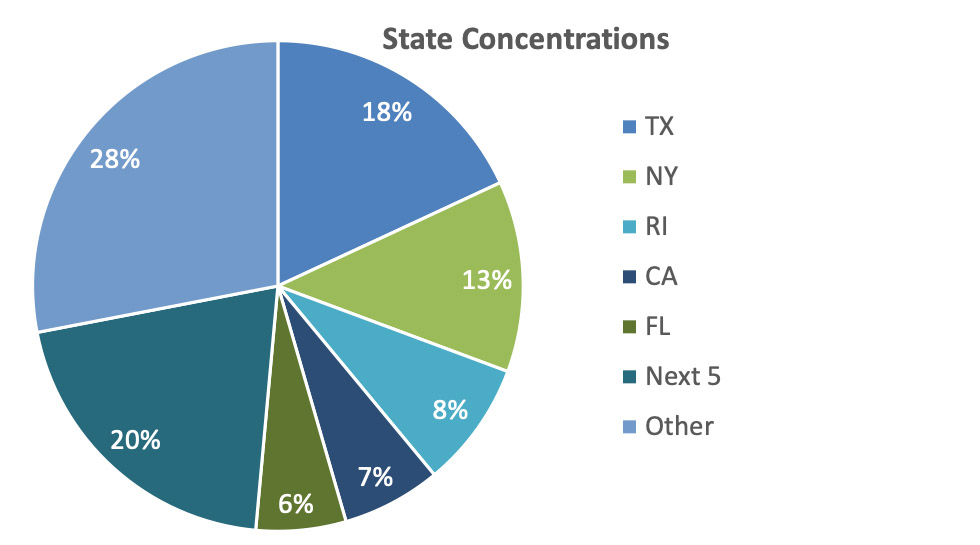

- Industry and State Concentrations: Concentrations are indicative of how much a borrower lends in each industry and state. In the above example, 24% of this borrower’s portfolio is made up of loans in the Property Maintenance industry. Additionally, 18% of the portfolio is comprised of loans in Texas. Concentrations are a useful metric to understand how a borrower is allocating their cash to underlying loans and ultimately a metric that sheds light on the portfolio diversification of each borrower. A diversified portfolio consisting of loans in many industries and states mitigates idiosyncratic risk and tends to offer more protection against highly concentrated portfolios.

Outstanding balance by anticipated payoff date

- Outstanding balance by anticipated payoff date: Payoff dates are indicative of the date in which an underlying loan is expected to be fully paid off. Where applicable, each surveillance report contains the above chart that details what percentage of the outstanding balance is expected to be paid off each month. In this example, 19% of the outstanding balance is expected to be paid off in August of 2020 with 16% expected to be paid off in September of 2020. This metric helps identify any exposure to conditions over particular time periods. For example, worsening economic conditions in the Spring of 2020 or Winter of 2021 should not affect this borrower as much as unfavorable conditions in the Summer and Autumn of 2020.

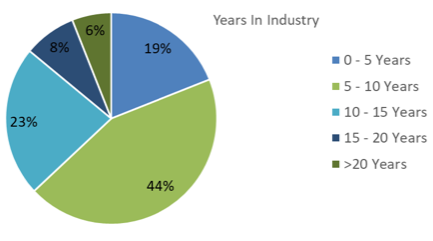

Portfolio Demographical Analytics

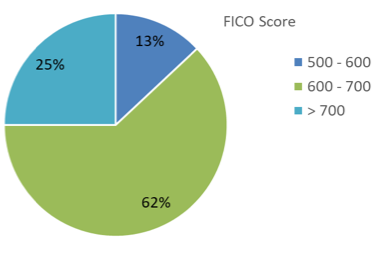

- Portfolio Demographics Analytics: Insights on the demographic composition of borrowers’ portfolios are paramount for a prudent risk-management framework. Where applicable, surveillance reports uncover these insights by showing the composition of credit quality as well as years in industry of each of the underlying borrowers receiving any advances or loans. In this example, 62% of the portfolio is comprised of loans or advances to borrowers with a FICO credit score of 600 – 700. FICO and Vantage credit scores are common measures of credit quality for the underlying borrowers. Additionally, in this example, 44% of the portfolio is exposed to borrowers with 5 – 10 years of industry experience. This metric is particularly useful to monitor for SMB lending products because of the insights it sheds on the quality and history of the underlying businesses. These two metrics together offer transparency into the credit worthiness of the underlying borrowers as well as uncover trends in underwriting standards over time.

Portfolio Origination and Collection Analytics

- Portfolio Originations and Collections: Where applicable and on a monthly basis, surveillance reports will highlight historical views on each borrower’s origination volumes and overall collections by their respective vintage. In the above example, $20.1MM was originated in November of 2019. For the vintage of November 2019, which refers to the month these loans were originated, $18.9MM has been collected by the borrower from their underlying borrowers. These analytics, over time, offer information about the historical issuance pace of each borrower as well as the historical collections on each of their assets. This transparency is provided so that investors can identify any spikes or lulls in origination volumes as well as bring to light any issues with collections of repayments.

Strengthening the Toolkit

As we strive to publish surveillance reports for all borrowers on our platform, there still may be some instances in which these do not offer insightful metrics due to the underlying term or structure of the assets. Our goal is to provide investors with understandable key investment metrics that allow them to identify trends and insights in the historically opaque private debt market. Given the historical limitations of data quality in the asset class, it is our view that investors will make better investment decisions with an enhanced toolkit at their side.

As borrowers are aware of the data being distributed and analyzed, these reports also work as a method to incentivize strong underwriting and collection practices. We’ll continue to maintain our commitment to unparalleled transparency by providing investors with access to more data, trends, and insights. It is our goal for all investors to be able to participate in this market by making well-informed implementation plans with sound data and analytics supporting those investment choices.