Disclaimer: As of February 2025, Percent has transitioned from using Annual Percentage Yield (APY) to Coupon Rate for all new investment opportunities. Any references to APY in this post now correspond to Coupon Rate.

👉 Learn more about Coupon Rate and how it impacts your investments here.

—

When transactions close and are funded by investors, Percent, Underwriters, and similar agents often continue to monitor borrowers and their activity. Throughout the entire duration of a note, it is typically important to monitor both the performance of borrowers on the platform as well as any underlying collateral that supports an offering, if applicable. To understand how the monitoring process works, please see below.

We regularly perform these important surveillance tasks to stay informed from a due diligence perspective and keep investors informed. To better understand just how thorough we are when surveying borrowers, we’ve broken down our surveillance process.

Collateral Performance

Percent routinely monitors the performance of the underlying collateral backing the notes on our platform. We do this to measure how the actual performance of the collateral aligns with the assumptions formed during the new borrower onboarding process.

This performance is then summarized in the Surveillance Reports produced by Percent’s credit team, and are based on borrower-provided portfolio data files. Depending on how frequently borrowers provide these data files, the reports are typically produced and published on a daily or weekly basis or, in some cases, monthly.

Surveillance Reports can vary in certain content based on asset class nuances and by how much information an borrower is able to provide. Below are important items found in Surveillance Reports, agnostic to asset class nuances and not borrower-specific, that we take into consideration throughout the life of a transaction:

-

- Deal Summary: The top of the surveillance report contains a summary of the transaction with key information, including the transaction’s annual percentage yield (APY), investment term, total number of assets, note size, and collateral balance.

- Days Past Due Analysis: As delinquencies precede defaulted balances that decrease the total amount of money available to pay off notes, Percent monitors the amount of underlying collateral that is delinquent. The analysis focuses on what percentage of the outstanding collateral balance is delinquent, typically broken out in the categories of current (<= 1 day past due), 2-30 days past due, 31-60 days past due, 61-90 days past due, 91-100 days past due and 121+ days past due. Seeing how those balances may change over time is important as it is an early indicator of decaying credit performance. When the data is available, reports may further breakout delinquencies by categories such as state or obligor industry.

- Portfolio Concentration Analysis: Percent typically stratifies the underlying collateral into various categories by outstanding balance to observe how the pool changes over time. Collateral pools can be stratified by various categories depending on the data provided, such as state, industry, credit scores, time in business, loan-to-value ratio, receivable seller, and modality.

- Other Credit Features: This section displays the outstanding cash reserve account balance, if any, which is a form of credit enhancement for certain Percent notes. In addition to providing notes with credit protection against losses in the underlying participation portfolio, the reserve account balance provides liquidity that can be used to meet note interest and principal payments if proceeds from the underlying assets are not enough to cover the required note payments. Furthermore, the Payment-In-Kind (PIKable) nature of a corresponding program’s note is shown under this section. PIKable interest, where applicable, is a payment structure where unpaid interest is permitted to accrue without having any negative implications, such as early amortization or event of default, for the note. PIKable notes help borrowers manage uncertainty in the cash inflows’ timing by extending the payment due dates of the required note interest payments to a later date. When PIKable interest applies to a transaction, typically a predetermined maximum number of months are allowed for the interest to PIK.

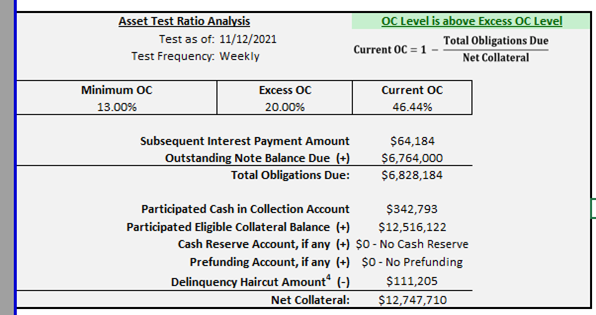

Percent also monitors the credit performance in some transactions on the platform with a tool referred to as the Asset Test Ratio. The Asset Test Ratio is a measurement of overcollateralization that tracks the amount of cash and receivables available to pay off a note’s principal and interest balances. The calculated overcollateralization (or OC) amount is confined within a minimum OC and excess OC level. When the OC amount is below the minimum OC level, cash flow from the collateral cannot be reinvested into new collateral. When the OC amount is above the excess OC level, excess cash flow can be leaked to the borrower as long as the OC level remains at or above the excess OC level after the cash leak.

The Asset Test Ratio section in surveillance reports also includes the inputs and ratio formula, which allows investors to quickly identify major driving factors of the asset test ratio performance. For instance, by monitoring the movement in the formula components such as the Participated Eligible Collateral Balance and the Delinquency Haircut Amount, investors can detect which element of the asset ratio test formula has led to the improvement/deterioration in the test performance.

We also highlight whether the asset ratio test is currently passing or failing. Please note that these inputs are also defined more thoroughly in our surveillance report data presentation guide.

Ongoing Borrower Due Diligence

Percent requires each borrower to provide updated due diligence information on a quarterly basis in the form of a questionnaire. This information includes (but is not limited to) company financial statements, updated portfolio data files, notifications of any new third party agreements, trailing twelve months defaults and net losses, and material changes within the organization (such as key management changes, updated product offerings, changes to credit scoring and underwriting, acquisitions, divestitures, joint ventures, lawsuits, regulatory changes with material business impact, and more).

Prior to beginning the quarterly review process, we confirm internally that the questionnaire includes the appropriate questions. We will periodically append questions that relate to current economic events, and will require insights from all borrowers. Our team reviews and internally documents any pending or open questions or issues as well as compares results to the prior quarter to identify any large deviations. The quarterly due diligence questionnaires provide us with important borrower information that may influence the credit performance of the underlying collateral. Any significant updates are typically disclosed in a surveillance report and/or the PPM and deal page of a roll-over issuance.

Our credit team also updates certain internal scorecards with refreshed financials and any other relevant information on an annual basis. Depending on the change in certain internal scores, our internal committee may have to reevaluate and approve, modify, or deny the transaction as well as reevaluate any automatic approval thresholds for future transactions.

This post was updated on April 8, 2022.