This year has been different than most analysts were forecasting eight months ago, with U.S. economic growth – supported by a resilient labor market – remaining firm even as the Federal Reserve has continued to tighten monetary policy to address inflation.

With the anticipated economic slowdown or recession yet to materialize, confidence is growing that an economic downturn might be avoided. Better-than-expected economic performance has in turn delivered returns for stock investors that have already surpassed expected year-end levels. Investors in U.S. Treasuries have had a more difficult time, with persistent core inflation forcing the Federal Reserve to stick to its restrictive monetary policies. The effect has been most perverse on the policy-correlated short-end of the U.S. Treasury curve, pushing yields higher.

The unexpected mini-bank crisis in mid-March involving the failures of Silicon Valley Bank and Signature Bank only temporarily halted the risk-on sentiment that characterized the first half of 2023. Although the expectation was that banks might tighten their lending standards following the bank problems, thereby reducing the availability of credit and jeopardizing corporate growth, credit spreads in the public debt markets have continued to grind tighter. The fact that the credit markets remained relatively robust, even as banks pulled back, reflected the ready availability of debt financing from other sources such as the public bond markets and private credit funds.

July provided a positive start to the second half of the year, with expectations improving that the U.S. would avoid a recession and might instead experience a so-called soft landing. August proved to be more mixed for financial markets, but economic data continues to suggest that the U.S. is “threading the needle” as far as the resiliency of the jobs market and disinflation.

Monetary Policy

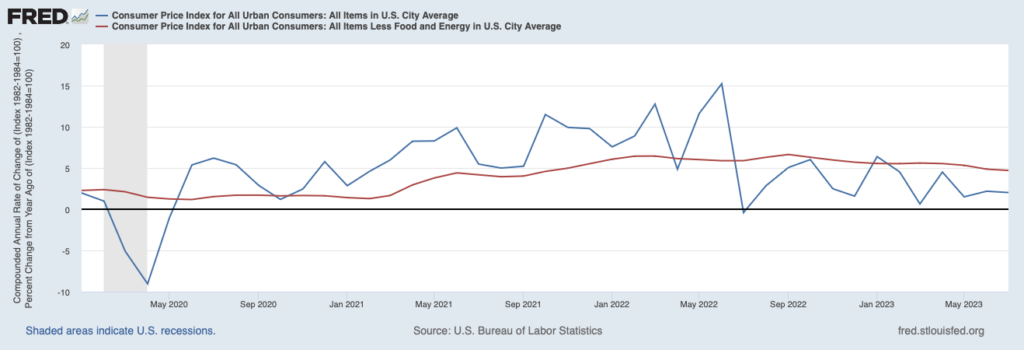

Monetary policy in the second half of the year will continue to be dependent on the magnitude and “direction-of-travel” of core inflation. The graph below illustrates year-over-year (“YoY”) headline and core inflation since January 1, 2020, the year that the pandemic began and the Federal Reserve first abruptly moved an accommodative stance (March 2020).

Year-over-year headline CPI peaked in June 2022 at 8.9%/annum, and year-over-year core inflation peaked three months later at 6.6%/annum. Since then, CPI has been improving, albeit sporadically, with headline CPI reaching 3.3%/annum in July and core CPI falling to 4.7%/annum.

Disinflation is clearly occurring, but core inflation remains significantly above the Federal Reserve’s target of 2%/annum. In other words, inflation is proving to be “sticky”, which likely means that the Fed will remain restrictive for many months even if it pauses increases in the Federal Funds rate increases in September. The CME FedWatch Tool shows a nearly 90% probability that the Fed will pause its rate hikes (as it did in June) at the September FOMC meeting, holding the Fed Funds rate at 5-1/4% to 5-1/2%. Interestingly, the probability of an additional 25bps increase at subsequent FOMC meetings in November and December appears to be very much on the table although not the highest probability scenarios.

Realistically, the probability of a reduction in the Fed Funds rate does not look to be in the cards until early in the second quarter of 2024. Once the peak rate is achieved – whether it is the current level of Fed Funds or 25bps higher – the expectation is that the Federal Reserve will likely maintain this peak level until it is comfortable that core inflation is back at or near the 2%/annum target.

Economic Outlook

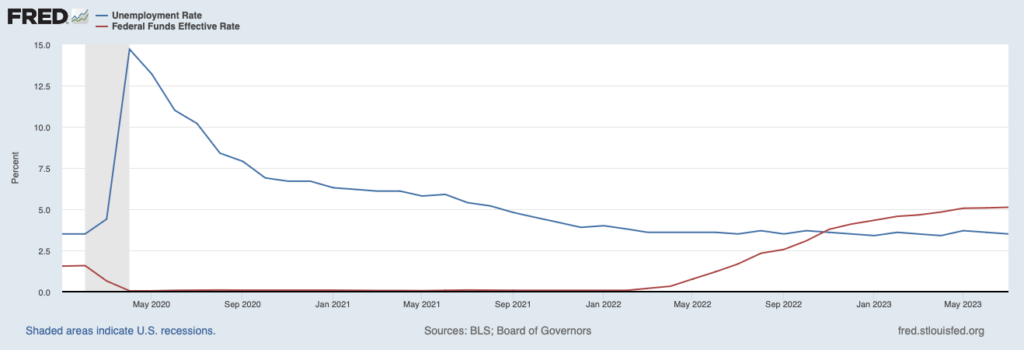

Even as the Federal Reserve continued to tighten monetary policy in the first half of the year, the U.S. economy remained on solid footing. 2Q2023 GDP was above expectations, coming in at 2.4%, following 2.0% growth in the first quarter. Resiliency in the jobs market and solid economic growth has caused most economists and investors to revise their growth expectations for the U.S. economy. Many have pushed back the timing of a (mild) recession to late 2023 / early 2024 or have even concluded that there will be no recession at all. The so-called “soft landing” scenario, in which growth slows but the economy does not slip into a recession, has been the Federal Reserve’s goal all along, but is now gaining broader support as a potential path forward. The most surprising attribute of the U.S. economy has been the very resilient jobs market. The graph below, showing the unemployment rate (blue line) and the Federal Funds rate (red line), illustrates just how low and stable the unemployment rate has remained throughout the tightening period by the Federal Reserve.

The most recent unemployment figure was 3.5% for July, hovering right at historical lows. The U.S. labor market has remained robust with no signs that employment is being negatively affected by higher interest rates, at least not yet. It is the tight labor market that seems to most concern Fed officials and investors because it suggests that monetary policy will need to stay tighter for longer in order for inflation to be brought down to the target rate.

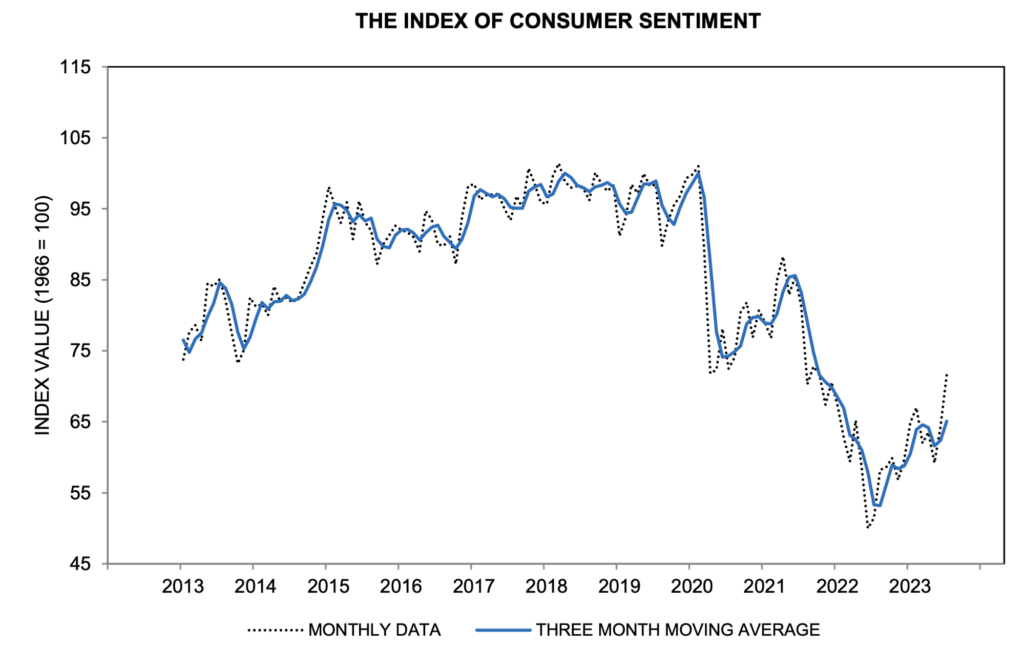

One final indicator of the resilient U.S. economy has been consumer confidence. Readings in June and July from the University of Michigan Consumer Sentiment Index1 suggest that consumers are becoming more confident about the future, reversing a trend of declining confidence that has largely characterized the post-pandemic period. The most recent reading in July was the highest since October 2021, as shown in the graph below.

In addition, the most recent survey suggested that consumers’ expectations regarding future inflation are moderating, which is good news for the Federal Reserve.

Lastly, it should be noted that corporate revenues and earnings have been slightly better than analysts’ consensus expectations in the most recent quarter. According to the most recent I/B/E/S data from Refinitiv (for week ended August 4, 2023), year-over-year revenue and earnings growth of S&P 500 companies for the quarter just ended are expected to be +0.2% and -4.2%, respectively. Even though these are not good headline figures in isolation, the fact is that better-than-expected results generally have proven supportive of rather elevated levels of stock prices, which – as a reminder – are already well in excess of Street forecasts from the beginning of the year.

Credit Markets

As the year started, there was an expectation of a shallow recession in the U.S. in 2023, most likely beginning in the third quarter. The crisis that engulfed several U.S. banks, leading to the FDIC take-over of Silicon Valley Bank and Signature Bank in March, made the likelihood of a potential credit meltdown even higher. Since that time, the spotlight has been focused on mid-tier U.S. banks and the quality of their assets, a concern that has continued into the second half of the year.

However, with the much-anticipated U.S. recession has not occurred and the economic signals currently suggest that an economic downturn is by no means certain, and in any event, is certainly not imminent. This has buoyed risk assets broadly, including credit assets, which time and time again have shrugged off concerns about tighter bank credit, higher costs of borrowing, and rising default rates.

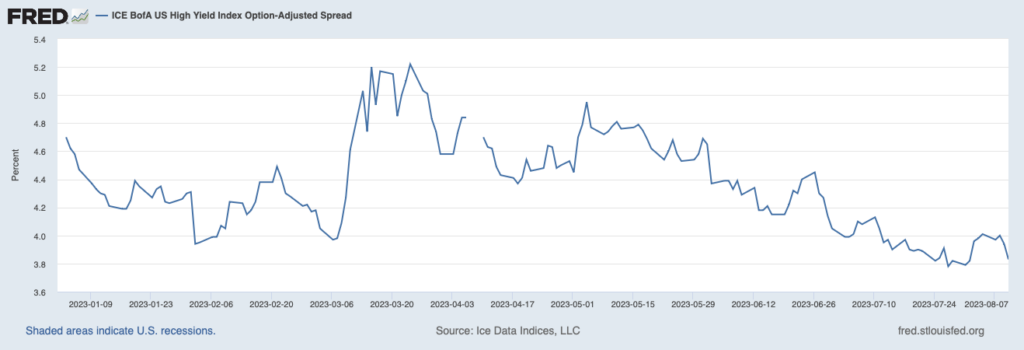

The reality is that corporate bonds have offered decent returns this year even as underlying yields were increasing, eroding value. Total returns for investment grade (more sensitive to underlying increases in Treasury yields) and high yield (thought to be under duress), have been reasonably decent, returning 3.2% and 5.4%, respectively in 1H20232. Credit spreads ratcheted tighter in both investment grade and high yield during the period, a trend certainly not anticipated by analysts and investors at the beginning of this year.

Going forward, the lag effects of tighter monetary policy and the diminution of (pandemic-related) positive fiscal policy – coupled with tighter bank lending standards – will likely push credit spreads for the riskier end of speculative grade bonds higher.

Other Markets

Other asset prices that were watched carefully in the first half of 2023 included the U.S. Dollar and oil. The expectation was that the U.S. Dollar would weaken during 2023 since the Federal Reserve would probably be the first central bank to get a grip on inflation and then pivot to a less restrictive posture. In fact, inflation has proven persistent in the U.S. and most other G7 countries, as central banks – except for the Bank of Japan – have remained in a restrictive mode. As a result, the U.S. Dollar has weakened against the DXY index, but not as significantly as was expected.

Oil has been the other surprise, with prices proving highly volatile but most recently increasing, which the IEA attributes to the fact that “world oil demand is scaling record highs, boosted by strong summer air travel, increased oil use in power generation and surging Chinese petrochemical activity.”3 Analysts at the beginning of the year, anticipating a global recession by summer, had thought oil prices would settle and decline. However, a combination of strong demand – as highlighted by the IEA – and tight control by OPEC+ of the supply of oil on the market, has instead boosted prices as the expected recession has been deferred or possibly avoided altogether.

As far as other geographic markets, eyes remain focused on the world’s second largest economy, China. China is facing a host of domestic issues, including declining consumer demand, potential deflation, and a troubled property sector. The global economy needs a strong China, and this now looks far less likely than it did at the beginning of the year, when an economic recovery was expected.

Private Credit

Private credit was arguably, and perhaps counter-intuitively, given a boost by the mid-March mini-bank crisis in the U.S. Although tighter bank lending standards following this crisis will continue to make bank credit more challenging, the combination of the public capital markets remaining readily open (albeit perhaps more selective) and the availability of the growing pool of private capital has filled the void rather quickly. Lenders of all types obviously need to remain attentive to worsening economic conditions, but the expectation of a rapid increase in corporate defaults – although often discussed – has simply not occurred.

For the second year running for fixed-income investors, intermediate and long-dated U.S. Treasuries appear the place not to be within a fixed-income bucket. Increasing yields have more than offset higher coupons, pushing UST bond total return indices into negative territory.

UST bills remain attractive, as do short-dated private credit assets, since inflation has not yet been fully brought under control and these assets are much less rate-sensitive. These are opposite ends of the risk spectrum, but private credit assets can offer a substantially higher return (estimated at double) of risk-free UST bills of similar short duration. So far, private credit assets appear to have been as resilient as public high-yield bonds, with no visible signs of credit stress.

Outlook

The remainder of 2023 will be different from the first half of the year in which risk-assets, including most global equity markets, rallied hard. As much as conviction is growing in a soft landing, the reality is that higher interest rates will soon bite and will potentially bite hard once the lag effects pass. Ongoing quantitative tightening by the Federal Reserve, coupled with strong new issue supply coming from the U.S. Treasury, are likely to keep pressure on the intermediate and long end of the UST curve. In this context, UST bonds will continue to be under yield pressure, and equities will likely consolidate as the reality of higher yields for longer takes hold, even if slow disinflation continues. Credit assets remain a “go to” asset class, and private credit in particular can often provide structural and covenant protection, and shorter duration, than riskier unsecured or subordinated high-yield bonds.

1Survey of Consumers from the University of Michigan, Preliminary Results for August 2023

2Source: ICE BofA Total Return Indices for investment grade/BBB bonds and for U.S. high-yield bonds

3Source: International Energy Agency (IEA) Oil Market Report – August