2022 brought new challenges to companies raising capital in public and private markets alike. The cost of capital rose, as did execution risk, with increased market volatility. In certain industries like cryptocurrency, specific events ravaged markets. Overall, most borrowers on the Percent platform have managed the change in circumstances well; but, for good reason, many are holding their breath for what 2023 will bring.

Rising Rates – The Painful Reality of 2022

Escalating borrowing costs were the defining event in capital markets in 2022. The increase in risk-free rates reflects the stunning change in the monetary stance of central banks and their rapid action.

In the United States, the Federal Reserve increased the lower end of their target range on the Federal Funds Rate from 0.00% to 4.25%, the highest it’s been since 2007. At year-end 2021, the 2-year Treasury yield was 0.73%, increased to 2.92% by mid year, and ended 2022 at 4.41%1.

For riskier borrowing, spreads rose as well. From 1.21% at year-end 2021, BBB-rated option adjusted spreads rose to a high of 2.10% in mid-October before retreating partially to 1.72% by year-end 20222. Spreads on Single B-rated instruments rose from 3.51% to a high of 6.71% in early July, but fell back to 5.15% by year end3.

As a result, by year-end a high-yield private borrower in the U.S. would expect to pay about 5.3% more for 2-year borrowing than a year earlier, mostly driven by the increase in short-term interest rates. For non-financial corporate borrowers, whose revenues should not see any corresponding increase from interest rate hikes, these higher costs can be painful.

The objective of monetary tightening is to curtail credit and, in turn, monetary creation and inflation. These actions have inevitably led to companies (financial or non-financial) rethinking their capital markets strategies in 2022.

For example, the CFO of a non-financial corporate borrower may choose to address interest rate risk by borrowing at fixed rates rather than at variable rates or by hedging the floating rate risk. However, hedging this risk is not common for middle market borrowers, many of which rely on floating rate or short-term borrowing, and neither precaution would address refinancing risk. As Bloomberg stated, “facing the prospect of refinancing at exorbitant yields” and with interest rate hikes “threatening to push the economy into recession,” some borrowers have become distressed4.

Financial companies borrowing in private or public markets may have an easier time since their revenues are linked to interest rates, at least loosely. Yet even these companies have faced trouble or have had to curtail lending. This is particularly true for those who have been funding longer-term loans with shorter-dated liabilities or are struggling to pass on an elevated cost of capital to clients. Many underlying customers these financial firms lend to might just turn down the money if it got more expensive, potentially causing the business to shrink.

Costly Distractions

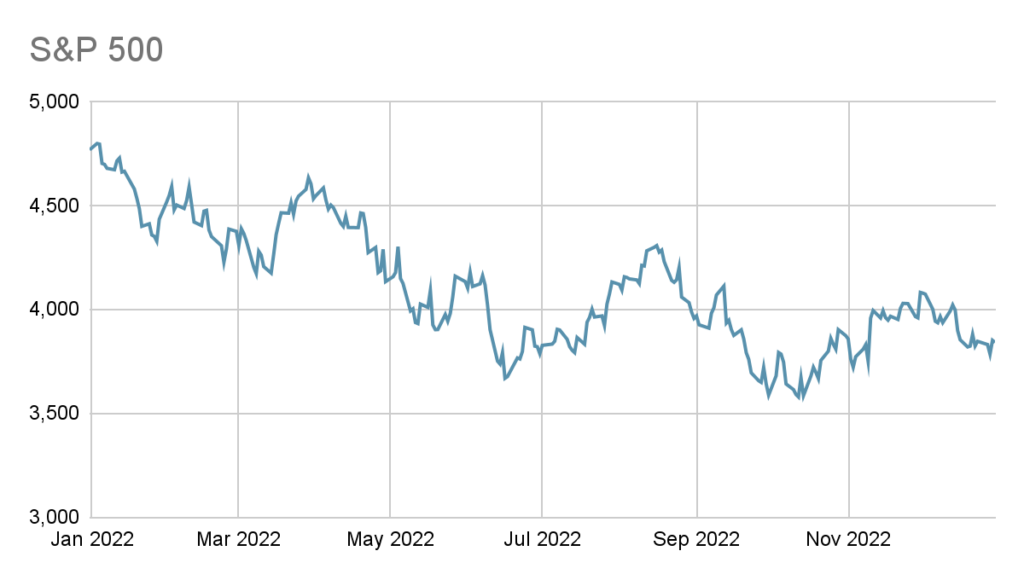

Public equity markets suffered as demonstrated by the fall of the S&P 500 from its near-peak of 4,766.18 at year-end 2021 to 3,839.50 at the end of 20225. Public debt markets have also declined as rates rose, spreads widened, and default worries sprouted6. Yet with lower prices came opportunities and, as a result, new issuances had to compete with the improved, sometimes juicy, yields available on the secondary market. Even private markets were affected as private market investors could now find appealing opportunities in public markets. Despite these headwinds, the Percent platform found new adoption last year from borrowers and investors, especially as the platform opened to borrowers outside of the specialty finance industry with new corporate loan issuances.

Events relevant to specific geographies, industries, or sectors have been dramatic, in some cases imposing consequences on borrowers in other markets. As just one example, falling prices for shares in publicly-listed software companies have impacted valuations in private venture capital markets. This, in turn, influences the venture debt market, increasing the demand for venture debt from borrowers needing capital to bridge themselves to a more favorable capital raising environment while also making some venture debt investors wary about take-out prospects. Problems in downstream markets affect borrowers and investors much further upstream. In the venture debt space specifically, Percent’s platform helps fill the void for borrowers looking to syndicate venture debt with multiple investors.

2022 also brought other special events that created isolated implications for credit in specific sectors. Borrowers in the crypto space were impacted by the sell-off in cryptocurrency markets and periodic crises like the failure of cryptocurrency exchange FTX in November. Earlier in the year, the Russia-Ukraine war affected borrowers with assets or operations in those countries; as just one example, the war caused a minor crisis among aircraft lessors and the related sector of the asset-backed securities market7. Idiosyncratic events, combined with negative trends in public markets, also derailed many firms’ capital raising plans during the year.

Performance

The past year was a challenging one for borrowers, not surprising given the quick change to monetary conditions. In the U.S., borrowers in both financial and non-financial sectors experienced financial distress. Among non-financial firms, cosmetics company Revlon was one of the largest victims, filing for bankruptcy in June8. Carvana is another business on the brink9. Indicators of financial distress generally rose in 2022 but, on the bright side, remain far below where they stood in past crises. Still, expectations for 2023 are not particularly optimistic: credit rating agencies, among other observers and participants, anticipate greater distress10 11.

Access to capital, opened to so many through the accommodative monetary policy of a prior era, may have seemed a divinely-ordained right at the beginning of 2022. It seems at risk now12, as capital is already harder to secure. As a result, borrowers with a competitive advantage in capital raising, whether intrinsic or obtained through engagement with markets such as those supported by Percent’s platform technology, may gain the upper hand in 2023.

At Percent

Percent welcomed twelve new borrowers onto its platform in 2022. Tapcheck, a California-based fintech company providing earned wage access, sold a $1 million six-month note in April at a rate of 9.50% APY. In September, they also issued a $2.4 million nine-month note at a 9.00% APY.

Other new borrowers included venture capital-backed tech firms like Singapore-based Taiger, a leading provider of artificial intelligence solutions to banks, insurers, and the legal industry. Taiger issued a $2 million venture debt note at 22.0% in September which was structured by Percent alongside AP Structured Finance, a third-party underwriter on the Percent platform that specializes in Latin American financial markets.

Multiple new specialty finance borrowers also joined Percent. These included Spain-based ID Finance, a consumer lending platform, whose inaugural issuance of $1.9 million at a 12.52% APY took place in March. After subsequent issuances, the company now has just over $4.5 million outstanding on the Percent platform. Other new specialty finance borrowers include Giggle Finance, Pulpi, Fishtail, Uplyft Capital, Prestanómico, ePesos, Leasy, and Percent itself.

Percent also opened its underwriting platform for broader participation in 2022, resulting in several transactions introduced to Percent by third-party underwriters or structuring agents. As one example, a $2 million venture debt offering for Nomad Homes, an online multiple listing service real estate platform, was issued in July 2022 and underwritten by private investment firm 8090 Partners.

In all, more than $275 million in private credit transactions were issued on the Percent platform in 2022. Beyond issuances by new borrowers, many existing clients issued new programs, often with larger notes. A $20 million offering for Wall Street Funding, an originator of cash advances to small businesses, was the largest single note offering to close on Percent’s platform to date13. The second largest offering this year was from The Smarter Merchant, another small business financing company, and was their 17th offering and the largest on the platform to date.

We also introduced numerous enhancements to the Percent Borrower platform in 2022, from improving the user experience to enhancing security with more rigorous authentication. A new pre-qualification questionnaire has jumpstarted the onboarding process while data rooms now make it simpler to manage documents and a new monitoring section provides surveillance reports and other key program data. Deal activity is now available in real time, and borrowers have greater transparency into the deal structuring and syndication processes with previews, visibility into the order book as it builds, and a view of all final allocation data.

Our technology roadmap for 2023 includes building out more granular views; adding new data and comparison functionality; providing enhanced workflow tools (enabling even better connections between borrowers and underwriters or investors); and launching additional tools to help borrowers manage their own access to and activity on the Percent platform.

As the modern private credit marketplace connecting borrowers to underwriters and investors, Percent will continue to deliver innovative capabilities and solutions to borrowers during 2023. We remain committed to helping borrowers access flexible, low cost of capital from our broad and growing network of qualified investors. Contact us to discuss how Percent can help your organization meet its capital goals, whether by issuing private debt or through structured venture debt or corporate loans.

2 https://fred.stlouisfed.org/series/BAMLC0A4CBBB

3 https://fred.stlouisfed.org/series/BAMLH0A2HYB

5 S&P Dow Jones Indices, S&P 500®

6 https://www.nytimes.com/2022/11/10/business/economy/corporate-bonds-fed-interest-rates.html

8 https://www.cnn.com/2022/06/16/investing/revlon-bankruptcy/index.html

10 https://www.nytimes.com/2022/11/10/business/economy/corporate-bonds-fed-interest-rates.html

11 KBRA Insight on Private Credit, October 20, 2022, https://www.kbra.com/documents/report/163592/private-credit-12-is-not-affordable-for-many-borrowers

12 For lending standards, see the Federal Reserve’s ‘Senior Loan Officer Opinion Survey on Bank Lending Practices’ https://www.federalreserve.gov/data/sloos/sloos-202210.htm. For financial conditions, see the Chicago Fed’s ‘National Financial Conditions Index’. Both report conditions that are tightening in more areas than they are loosening. https://www.chicagofed.org/publications/nfci/index

13 https://percent.com/blog/news-item/a-new-funding-milestone-on-percent/