Risk Management for Foreign Currency Risk

As discussed in our previous posts, “Our Holistic Approach to Risk Management” and “Delivering You Consistency in Risk Management,” our robust internal risk framework is the foundation for every offering on the Percent platform. We developed our digital securitization and investment platform with a major focus on assessing the suitability of every opportunity. This includes, but is not limited to, analyzing the creditworthiness of all the counterparties that impact the cash flows; employing a proprietary risk scorecard to both quantitatively and qualitatively assess every counterparty; structuring our investment opportunities with the primary objective of protecting investment principle.

At Percent we only offer investment opportunities that pass our rigorous vetting process for our borrower partners. As part of our own due diligence process, we obtain an in-depth understanding of each borrower's credit process, understand the intrinsic risks within each loan product or segment they respectively target, and recognize the broader macroeconomic circumstances that can increase repayment risk in each region, country or jurisdiction our originators operate in.

As described in previous posts, we usually divide risk into two categories: asset performance risk and counterparty risk. The former relates to when the underlying assets contributing to the repayment of an obligation do not perform as expected. The latter deals with the risk that the performance of a note becomes de-linked from the underlying assets due to the actions of a transaction party.

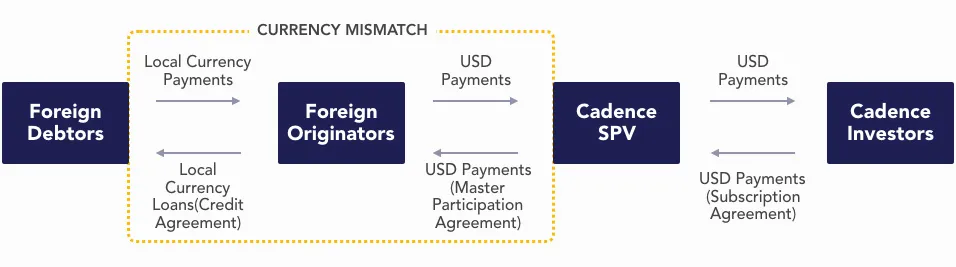

If a borrower is based in a foreign country, or has assets in a denomination different than the U.S. dollar, there is an added component to the counterparty risk, which we can call currency risk. For instance, if the underlying loans of a borrower are tied to local currency, and if during the period during which the note is outstanding, the local currency depreciates against the U.S dollar, it will make the payments from the borrower to Percent's issuing SPV more expensive, potentially resulting in a higher probability of underperforming on the interest and principal repayment to our investors. As we continue to explore international opportunities for our investors, the following are some of the main mechanisms we utilize to mitigate currency risk:

- During our assessment of international borrowers, if their country of business is going through country-specific financial distress, with either increased inflationary concerns, a quickly depreciating currency, or is overall experiencing high volatility, we would be cautious to proceed altogether with a transaction at that time, eliminating any potential risk to investors, as we would not feel comfortable onboarding a transaction to our platform until more stability can be seen in the country of operations of our borrower.

- To date, we have not worked with any entity domiciled in any country whose government currently restricts persons or entities to convert local currency to foreign currencies, including U.S. dollars, the currency in which investments are denominated in on our platform. As part of our processes, we conduct ongoing monitoring and continuously diligence the loan book performance, the broader performance of our borrower partners, and country and regulatory dynamics where they have risk exposure to, and will do our best to mitigate and communicate all relevant risks at the time we begin marketing each transaction, as well as during any subsequent note rollover or new transaction thereafter.

- For issuances involving assets from non-US borrowers, we also engage with local legal counsel, from the country where the borrower is based, during our due diligence process. We select our local counsels based on their track record and reputation in the country, while also having extensive experience with private credit and capital markets. Engaging local counsels allows us to better assess and understand all legal considerations, including any currency-related concerns, other potential risk implications, which we aim to communicate to our investors in the confidential private placement memorandum available during syndication period, and incorporate all relevant takeaways into the structure of the note, as required.

- In cases where the underlying assets of our partner borrowers are not in dollars or dollar-linked, this can lead to a currency mismatch, which, as discussed, can add a layer of risk to the overall investment. In order to mitigate this risk, some borrower partners have implemented currency hedging strategies, but that remains at the discretion of how each borrower chooses to manage their own asset and liability currency strategies, and any regulatory constraints in their respective countries of origin. Even if issuers are able to enter into cross-currency swaps to manage the risk profile associated with currency and interest rate exposure, this can also potentially lead to mark-to-market losses or margin calls that can be caused by decreases in the fair value of cross-currency swaps attributable to the appreciation of local currency against the U.S. dollar or fluctuations of interest rates in the respective countries.

- Once a note has been issued, and as we continue to monitor our transactions and diligence our borrower partners and their respective portfolios, we continue to monitor country risk and FX performance. One advantage of the Percent platform is that as we are working with short term notes, we can reassess our borrower's risk profile promptly and re-align the risk-return equation for our investors or borrowers, as recommended, at maturity date or call date of a note. We consider this feature to be a key component of our offerings because we are providing for flexibility across our short term note programs in an otherwise illiquid market.

- Percent usually also requires that borrowers absorb losses on the collateral up to a predetermined point. This acts as a credit enhancement of the investors of the notes. If any significant currency depreciation occurs during the life of the note making it harder for the borrowers to make payment on the U.S. dollar obligations, in the absence of a cross-currency swap, we have already incorporated into the deal structure a “first loss cushion” or “first loss provision.” Historically, this first loss cushion has varied between 5% and 30% of notes’ principal and interest amount.

- Borrowers also generally manage a liquid amount of U.S. dollars in cash accounts in case they need to face any unexpected capital calls or have upcoming U.S. dollar obligations due in the near future. Furthermore, many financing borrowers also have other sources of capital available and/or have established lines of credit with institutional investors, and can access them as needed.

We are careful and diligent to only bring opportunities to our platform that we are confident will perform as expected. Of course, and similar to other asset classes we are also bound to external shocks that can create more volatility and deviations in performance. With every transaction we assess, we continue to update and improve our internal risk framework, which remains at the very core of the success of our investment platform. While determining what investments fit your risk profile best, we think it is important our investors understand different risks and mitigants on our platform.

Nothing in this post should be construed as an offer to sell securities or a solicitation of an offer to buy securities. All investment involves risk and the possibility of loss, including loss of principal, and neither past performance nor forward looking information is a guarantee of future results. Any decision to invest must be based solely upon the information set forth in the offering documents, regardless of any information that may have been otherwise furnished, including in this update.