Inflation is here to stay for the time being. Central banks in economies ravished by inflation remain singularly focused on addressing this issue, and they are quite right to do so as inflation proves stubbornly hard to rein in. This is not only true for the U.S., but also in the U.K. and the Eurozone.

Inflation in Practice

Central banks like the Federal Reserve are most concerned about inflation becoming entrenched, meaning that inflation becomes part of the mindset and fabric of consumers and businesses, thus influencing their behaviors.

- Consumers tend to bring forward purchases in inflationary environments, because goods and services are cheaper in the interim, but will become more expensive if purchased later.

- Businesses often accelerate investment and inventory purchases for the same reason. Waiting until later means components or final goods become more expensive, scarcer, or perhaps both.

In both cases, persistent inflation causes consumption and investment to be brought forward, adding further pressure on prices as near-term demand increases and supply often struggles to keep pace. As prices rise and inflation becomes part of people’s mindsets, workers then demand higher wages to maintain their standards of living. Higher wages mean businesses in turn must raise prices to protect their operating margins.

This leads to a vicious circle that can only be broken when inflationary expectations are brought down through tighter monetary or fiscal policy (or both). These policy actions almost always come with pain in the form of slower economic growth and higher unemployment.

How Our Inflationary Environment Began

The foundation for today’s current inflationary environment was set during the pandemic.

- During the early stages of the pandemic (March/April 2020), central banks in many countries quickly lowered interest rates to 0% and began to buy government bonds to keep yields low and spur economic activity. [This buying of bonds is known as “quantitative easing.”]

- Governments simultaneously adopted and passed various fiscal stimulus programs to help people and businesses first weather government-imposed economic shutdowns and then periodic cycles of sporadic/partial economic re-openings followed by new restrictions caused by outbreaks of COVID variants.

- In the U.S, the largest fiscal stimulus programs were the $2.2 trillion CARES Act (March 2020, under former President Trump) and the $1.9 trillion American Rescue Plan Act of 2021 (March 2021, under President Biden). These and other measures included three rounds of direct stimulus payments that were made to every American, totalling $3,200 over 12 months.

- Government stimulus spending in the U.S. to aid businesses and consumers during the pandemic is estimated to have totaled $5.2 trillion,1 or nearly 25% of 2019 (pre-pandemic year) GDP. The U.S. was unique in terms of the magnitude of its fiscal stimulus measures as a percent of GDP during the pandemic, and in terms of making direct-to-consumer stimulus payments to every American.

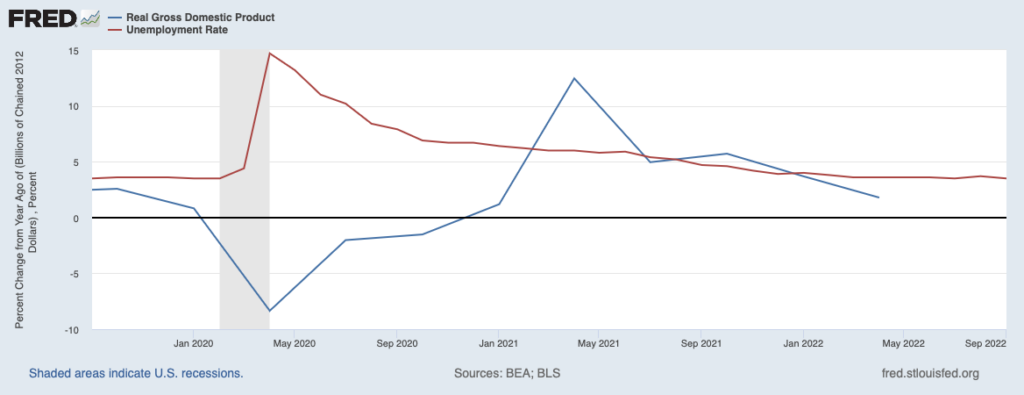

The combination of monetary and fiscal stimulus measures clearly helped restore the US economy to growth, even though the pandemic continued to be problematic until just recently. The graph below from Federal Reserve Economic Data (FRED) illustrates the dramatic slowing in economic growth and spike in unemployment that occurred starting towards the end of Q1 2020, when the pandemic was having its most direct effects on the U.S. economy and then the gradual recovery of the economy as stimulus measures played their role.

It is interesting to note that the extensive monetary and fiscal stimulus measures enabled the U.S. economy to return to its pre-pandemic real GDP level by Q1 2021, unique in retrospect given the severe effects that the pandemic had on economic activity.

How the U.S. Experienced Inflation

As recently as the autumn of 2021, the Federal Reserve was sticking to its mantra that inflation was transitory. This view was not illogical in that the Fed – like many other economies around the world that had splashed around pandemic-fuelled fiscal and monetary stimulus with near-impunity – clearly felt that inflation was principally triggered by issues specific to the pandemic, namely supply-chains disruptions, higher energy costs, and later Ukraine’s invasion by Russia. Excess consumer demand was thought to play a role, but not that influential.

In economic parlance, the Fed believed that inflation was principally supply-push rather than demand-pull.2 Since Jerome Powell and other Federal Reserve officials believed that inflation was principally caused by pandemic-driven supply side issues, it was only logical that these disruptions should end as the pandemic faded. However, it is now clear that the Fed badly underestimated the significant and ongoing increase in consumer demand that significant amounts of monetary and fiscal stimulus unleashed. Inflation did not fade as the pandemic began to wane, but rather – to the Fed’s surprise – actually worsened.

Why the Fed Changed Strategies

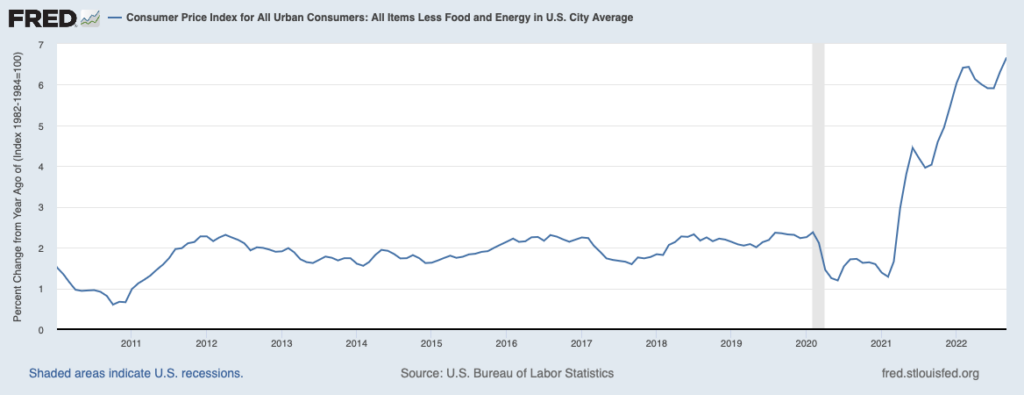

Jerome Powell and Fed officials finally acknowledged in the autumn of 2021 that inflation was perhaps less transitory and more persistent than they had hoped. Even worse, data was clearly showing that inflation was accelerating. The graph below illustrates the monthly level of core CPI (i.e. CPI less food and energy) since 2010.

Core inflation as measured by CPI remained around 2% throughout the decade following the GFC, which is the official target rate of inflation of the Federal Reserve.

CPI fell slightly as demand declined in Q1 2020 because of the pandemic, only to begin accelerating one year later during Q1 2021. CPI has continued to increase nearly every month since then until now. Core CPI (YoY) in September – the last read for the U.S. – was 6.6%, and headline CPI (all items, including food and energy) was 8.2%.3

Once the Fed completed its about-face in the autumn of 2021, they began to prepare markets for a pivot towards tighter monetary policy in the months ahead.

How Did the Fed Fight Inflation?

After signaling it would begin to tighten monetary policy in late 2021, the Fed did just that in March 2022, raising the Federal Funds rate (i.e. the overnight bank borrowing rate) by 25bps – to a range of 0.25% to 0.50% – in March. This marked the first change since rates were slashed to 0% during the opening stages of the pandemic.

Since then, the Federal Reserve raised the Fed Funds rate a further 350bps over four separate FOMC meetings. The Federal Funds rate is now 3.75% – 4.00%. Investors are anticipating another 75bps increase at the November FOMC meeting, followed by a 50bps increase at the December FOMC meeting. This means the Fed Funds rate would have increased from effectively 0% at the beginning of the year to 4.25% – 4.50% by the end of the year.

There are a variety of opinions on how much further the Fed might increase the Federal Funds rate, but current expectations are that it will not likely go above 5%. Concurrently with the rate increases, the Federal Reserve stopped refinancing bonds that were maturing on its $9 trillion balance sheet in June 2022, with a target of reducing the balance sheet by $1 trillion in 12 months. This is referred to as quantitative tightening, and was occurring simultaneously with rate increases as the Fed became extremely hawkish.

Most economists and investors believe that it will be late 2023 before the Fed will begin to think about easing or pivot towards more accommodative monetary policy. The potential trajectory could see:

- Further rate rises until there are convincing signs that inflation is slowing

- Several months of a following pause to study economic data

- Potential easing down the line based on economic conditions, especially unemployment and inflation data

The effect of tighter monetary policy has been most felt so far in financial markets rather than in the real economy. Stocks tumbled 21.3% YtD (S&P 500, through Oct 22) and longer-dated bonds are also sharply lower (20y UST index down 36.1% YtD through Oct 22).

Unemployment has hardly budged so far, and has in fact declined this year. The most recent unemployment rate for September was 3.5%, matching the lowest rate in the U.S. for the last 50 years. The good news from the perspective of the Federal Reserve is that the strong U.S. labor market provides more latitude as far as its policy actions to address what has become stubbornly persistent inflation.

In addition to raising the Fed Funds rate and embarking on quantitative tightening, the Fed also sought to make its rhetoric more convincing. Investors were conditioned since the Great Recession to expect the Fed to step in and provide monetary support at times of extreme stress, and by extrapolation, to rescue a sagging equity market. This is known as a ”Fed put.”

Investors heard some conflicting messages earlier this year from various Fed officials that, in essence, left the door towards a dovish tilt slightly ajar, suggesting if equities fell sharply, then the Fed would rescue equity investors. However, the Federal Reserve has been adamant since the summer that they do not intend to pivot towards more accommodative monetary policies until there are tangible signs that inflation is declining —even if these hawkish policies ultimately result in stocks falling precipitously. The Fed also believes that it can orchestrate a soft landing, meaning that they can bring down inflation without tipping the U.S. economy into a recession.

The late 1970s to early 1980s was the last high inflation period in the U.S., and the measures undertaken then by the Federal Reserve to bring inflation down came with a severe cost in terms of a double-dip recession in 1979-80 and 1981-82. Inflation averaged 13.5% in 1980 and unemployment reached 10.8% by the end of 1982, as stagflation set hold during a very painful period for the U.S. economy.

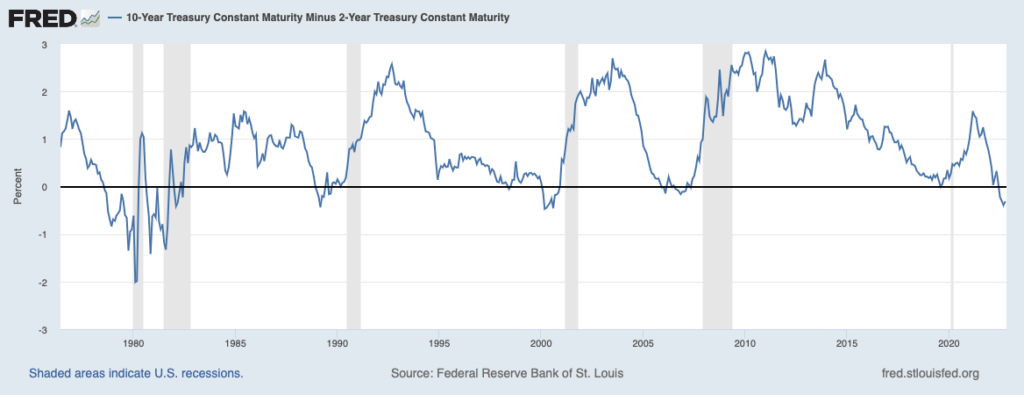

As you can see in the graph below going back to around 1975, a negative 2-10 year spread differential almost always precedes a recession (which is represented by the gray vertical bars).

One could suspect the Fed might begin to moderate its tone once there are clear, convincing signs that inflation is under control, but this could take another several months. Of course, the easing of lingering supply-chain disruptions and the calming of the conflict between Russia and Ukraine would also help, as would lower energy prices.

Investors should know that the Fed’s singular focus is on containing inflation, and the least of their worries is the performance of the U.S. stock market. The Fed was late to act since it thought inflation was transitory, but now that it has acted, the central bank seems laser-focused on addressing stubbornly high inflation.

1Source: Article in the Brookings Papers on Economic Activity entitled The fiscal policy response to the pandemic, written by Christina D. Romer and dated March 24, 2021.

2This is a topic covered in an article entitled About that transitory inflation…. which appeared in E-MorningCoffee.com on October 8, 2021.

3The U.S. Bureau of Labor Statistics’ Consumer Price Index Summary for September can be found here.