This is the first edition of Percent Market Insights, a new newsletter from Percent featuring commentary from market veteran Tim Hall of E-Morning Coffee.

Raising Rates

The Federal Reserve raised the Fed Funds rate for the first time since the pandemic in March, increasing it by 25bps (to a range of 0.25% to 0.50%), and has stopped asset purchases pursuant to its quantitative easing program. The central bank is likely to introduce a series of aggressive rate rises and begin quantitative tightening sooner than expected.

Investors React: These aggressive tightening measures spooked investors, possibly due to expectations that the Fed “had investors’ backs” and would ease off if financial assets started to deflate too rapidly.

Equities had a choppy ride since the Fed started becoming increasingly vocal about future policy moves, although sentiment reads as if investors have digested and accepted this approach for the time being.

- The U.S. and its allies anticipated the Ukraine-Russia war, but the reality of it actually happening hit financial markets hard. Investors immediately moved out of risk assets and into safe-haven assets like U.S. Treasuries, gold, and the U.S. Dollar.

- The focus on safe-haven assets faded rather quickly once investors considered potential outcomes of this unfortunate conflict.

Let’s look more closely at how various asset classes performed in March and in the first quarter of this year.

Equities Performance in Q1

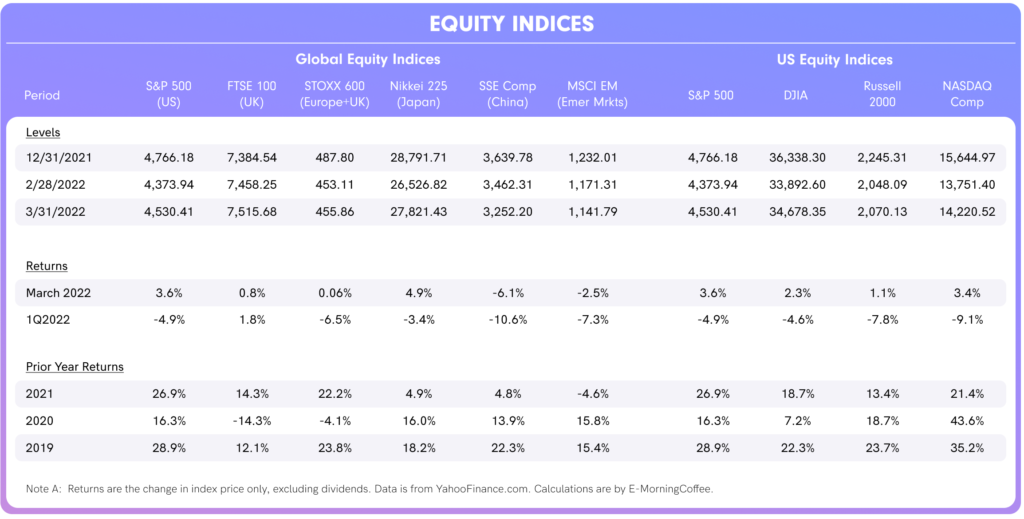

Select global equity indices and major U.S. equity market indices for March and for the Q1 2022. Note that these are changes in the index values only, excluding dividends (so they are not total return measures).

Returns in equities were generally poor in the first quarter, certainly compared to the returns in each of the prior three years. Globally, the only index with a positive Q1 return was the FTSE 100, but history has shown that this is probably an anomaly.

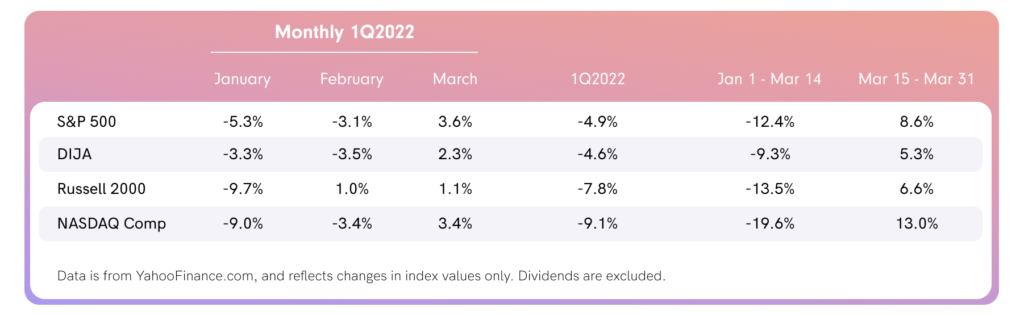

U.S. Equities: The S&P 500 was down 12.4% YtD at the close on March 14th, but gained 8.6% the rest of the month, leading to a positive return for March (+3.6%) and reducing the first quarter loss to 4.9%.

- The recovery of the NASDAQ Composite was even more pronounced, as this tech-heavy index snapped back from a loss of 19.4% YtD through March 14th to increase 13.0% since then, reducing the first quarter loss to 9.1%.

Bond Performance in Q1

Government bonds sold off in most major global markets as yields pushed higher because of inflationary pressures and concerns over the requisite tighter monetary policy ahead.

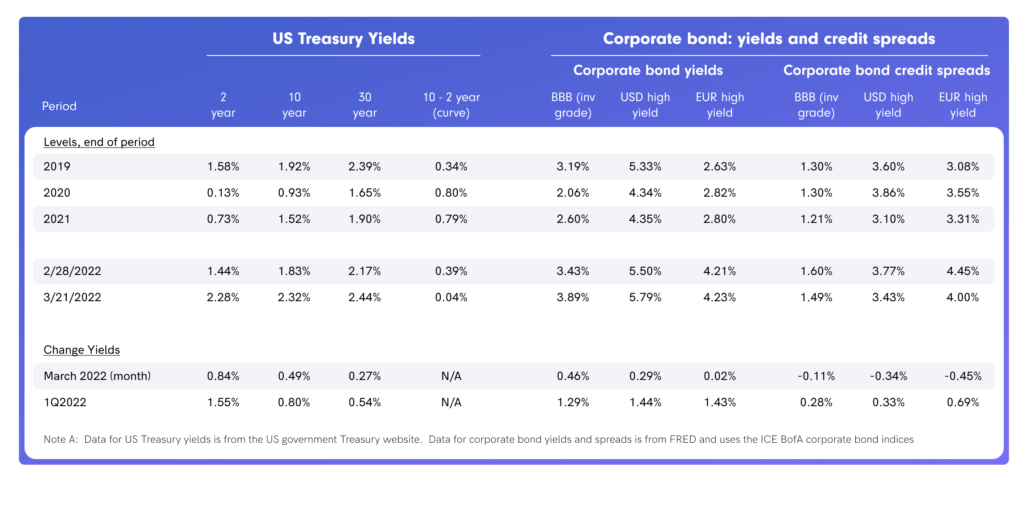

U.S Treasuries: U.S. Treasuries found a slight reprieve during the opening days of Russia’s invasion of Ukraine, with the yield on the 10-year U.S. Treasury declining from 1.99% on February 23rd (day before invasion) to 1.72% by March 1st.

- The reprieve proved to be short-lived as the 10-year U.S.T yield marched steadily higher the rest of the month, closing at 2.32% on March 31st, a nearly 60bps increase in a single month.

- The yield increase on the 10-year U.S. Treasury was dwarfed by the increase in the yield on the 2-year U.S. Treasury, which rose from 1.31% at the beginning of March to 2.28% by the end of the month a nearly 100bps increase.

- The yield curve was steadily flattening, and in fact the 2-year to 10-year yield difference inverted on April 1st, a much-discussed potential harbinger of a looming U.S. recession. U.S. Treasuries had the worst returns in decades during the 1Q2022, and March was especially harsh.

Corporate Bonds: Corporate bonds were not spared the pain of higher yields on underlying U.S. Treasury bonds, as credit spreads and yields increased on both investment-grade and high-yield corporate bonds. The effect of higher underlying U.S. Treasury yields had a more pronounced effect (than higher credit spreads) on corporate credit yields, reflecting the fact that credit fundamentals do not presently seem to be concerning investors.

- Corporate bonds will continue to suffer as yields on U.S. Treasuries increase, with investment-grade corporate bonds and the higher-quality end of non-investment grade being most at risk of price erosion.

- The table above shows 1) yield migration for the 2- 10- and 30-year U.S. Treasury securities, and the difference between the 2-year and 10-year U.S. Treasury yield; and 2) yield and spread migration for corporate bonds, both investment grade and high yield bonds denominated in U.S. dollars, and high yield bonds denominated in Euros.

- The table also shows the rather substantial increase in yields on U.S. Treasuries and corporate bonds. The table below shows what the yield increases mean to investors as far as price action.

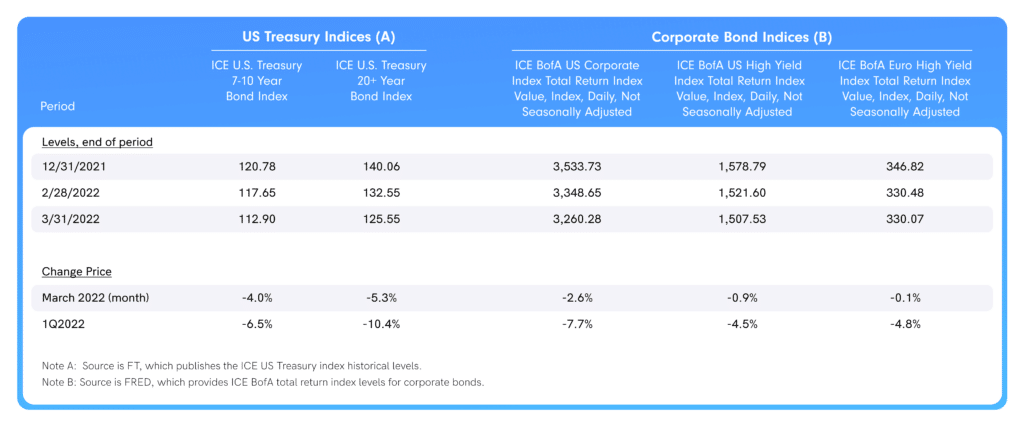

The pain in U.S. Treasuries has been most severe in longer maturity (i.e. longer duration) bonds. The ICE U.S.T 7-10 year bond index lost 4.0% in March, but the longer-maturity 20-year index lost 5.3%. U.S. Treasuries underperformed the S&P 500 in the first quarter.

- As far as corporate bonds, investment-grade bonds were the hardest hit because they have the narrowest margin in terms of a spread over U.S. Treasuries. Returns for U.S.D-denominated corporate bonds, both investment grade and high yield, and for EUR-denominated high yield bonds, were negative across the board in March.

Alternative Assets

Gold: Gold was a beneficiary at the onset of the pandemic as investors piled into safe haven assets. It recently stabilized and then gave up modest ground in 2021, ending down 4% for the year.

- The price of gold was largely range-bound in the $1,750-$1,850/oz area for much of 2021, continuing to trade in this range into January 2022. As losses began to mount in equities, investors shifted some of their assets back into gold, pushing the price above $1,900/oz by mid-February, and even briefly over $2,000/oz in early March.

- A new range of $1,925-$1,950/oz appears to be sticking for the time being. Gold ended March at $1,949.20/oz, gaining 2.6% for the month.

Cryptocurrencies: Bitcoin returned a stunning 59.7% in 2021, far outstripping the returns of nearly all other asset classes.

- Had you bought or sold Bitcoin during the year, your fortunes could have varied based on when you bought or sold Bitcoin in that the trading levels during the year ranged from a low of $29,374 (January 1st) to a high of $67,567 (November 8th). Price migration was highly volatile throughout the year. Bitcoin closed 2021 at $46,306.

- Bitcoin’s fortunes have been mixed so far in 2022, but the cryptocurrency had a solid March – delivering a 5.4% return – as other asset classes experienced sharper volatility and lower returns. Although we have not seen Bitcoin re-approach its 2021 highs, its trading range has narrowed, and the general price trend has been higher.

- In Q1, Bitcoin was down 1.7%, whilst the S&P 500 lost 4.9% and the NASDAQ Composite lost 9.1%.

Real Estate: The pandemic had dramatic and unexpected consequences on both residential and commercial real estate. Outside of metropolitan areas, the work-from-home shift caused by the pandemic, accompanied by excess liquidity and record-low mortgage rates, fueled hefty increases in residential real estate prices outside of cities. As with other risk assets, we are entering a stage now where the factors most influential in the increase in real estate prices during the pandemic are starting to reverse.

- People are rediscovering cities and returning to work (in the office), and mortgage rates are heading higher. The 30-year fixed rate mortgage started the year at 3.22% (weekly average as on January 6th, from FRED), and ended the quarter at 4.67%.

- Similar to U.S. equities, residential real estate has arguably approached bubble territory, but the hope is that pricing pressures will be reduced in a slow and orderly fashion rather than in a way that ultimately leads to a wholesale shift in sentiment as peoples’ wealth declines.

Inflation During Wartime

Investors are laser-focused on how central banks intend to address inflation before it gets out of hand and becomes entrenched. The U.S., U.K., and Eurozone are dealing with the highest inflation experienced for decades, a direct result of the excessive fiscal and monetary stimulus unleashed during the early stages of the pandemic (and exacerbated by supply chain bottlenecks).

A Momentary Distraction: Russia’s invasion of Ukraine, which began on February 24th, shifted investors’ attention away from inflation – albeit only temporarily.

- This led to a massive flight-to-quality favoring assets like U.S. Treasuries, gold and the U.S. Dollar. War concerns proved to be short-lived, as inflation returned to the forefront of investors’ minds within one week following the invasion.

U.S. equities remain richly valued based on historical levels and compared to equity markets in other countries, making them vulnerable to changes in sentiment. This confluence of macroeconomic and geopolitical factors led to disappointing results in the first quarter for equities and bonds, although the former found its legs in mid-March while the latter continued to sell off as inflation accelerated.

The U.S. Labor Market vs. Rising Prices

The U.S. jobs report for March, released April 1st, suggested the U.S. economy remains on firm footing as 431,000 new jobs were added in March and U.S. unemployment fell to 3.6%.

A Strengthening Economy: The U.S. economy is strong at the moment with an increasingly tight labor market, one of several contributors to rising inflation. These are also supply-push inflation factors putting severe pressure on prices, including ongoing supply-chain disruptions and rising commodity prices (most notably oil prices).

Oil Prices and Supply: The price of WTI crude oil increased 55.5% in 2021 and another 32.9% in the first quarter of this year, ending March at $100.28/bbl. U.S. CPI was 7.9% in February, and gasoline and oil prices rose 37.9% over the same period.

- It appears OPEC+ is experiencing difficulties in increasing oil supplies beyond the modest monthly amounts agreed to by the cartel’s members some months ago. If you then remove Russian oil and gas from global supply (circa 10% of global supply) and consider the reluctance of many U.S. independent energy companies to ramp up production because of shareholder pressure, there seems to be little relief in sight for addressing higher energy prices.

- The Biden Administration announced it would release 1 million bbls/day of oil from the U.S. Strategic Petroleum Reserve over six months to alleviate some price pressure, but this is only about 5% of daily U.S. consumption (of 20 million bbls/day).

- The White House is also applying pressure to major oil companies (attacking excess profits) and independents (reluctant to drill new wells) to get them to ramp up production.

Eurozone Inflation Woes: Inflation is not a uniquely U.S. phenomenon, as the U.K. and Eurozone are experiencing spiralling inflation, too.

- The Eurozone recently indicated that preliminary March inflation would be around 7.5%, while the U.K. had CPI in February of 6.2%.

- The Bank of England already increased its Bank Rate three times since December, the most recent at the mid-March meeting. The European Central Bank (ECB) seems more reluctant to increase short-term rates just yet, likely due to a combination of legacy moribund growth during the last decade in the Eurozone, the bloc’s greater reliance on Russian oil and gas, and the Eurozone being in closer proximity to the Ukraine-Russia conflict (and hence more at risk of the war expanding beyond Ukraine’s borders).

- Nonetheless, the tone of the ECB suggests a more hawkish approach is coming.

The Bottom Line

The Federal Reserve will have to be both right and lucky to bring down inflation without tipping the U.S. economy into a recession. At the very least, U.S. economic growth is certain to slow as the central bank embarks on a series of rate increases.

- Both the U.K. and the Eurozone face arguably even more daunting tasks in this respect. The one outlier as far as developed markets is Japan, where economic growth remains limp, and inflation does not seem to be a threat even as the Bank of Japan remains by far the most accommodative of G7 central banks. This has weighed heavily on the Yen, which has been weakening now for many months.

- In China – the world’s second largest economy – we can only hope that the recent outbreaks of the new variant of COVID in Hong Kong and now Shanghai will quickly subside.

Wild Card: The Ukraine-Russia war could worsen in ways that are impossible to predict. One would expect temporary relief rallies to fuel risk markets, although announcements regarding progress on peace talks are increasingly unreliable. There is no way to predict when or how this conflict might end.