A variety of economic data for the first quarter suggests that inflation remains persistent in the U.S. and in many other developed economies. This has created a dilemma for central banks, which have been tightening monetary policy for more than a year in an attempt to reduce inflation towards 2% per annum. For the Federal Reserve, continuing to increase interest rates to meet that target could prove challenging given current fragility in the banking sector. We could be on the verge of a period of stagflation, which historically presents challenges for traditional asset classes like stocks or bonds.

Inflation and Bonds

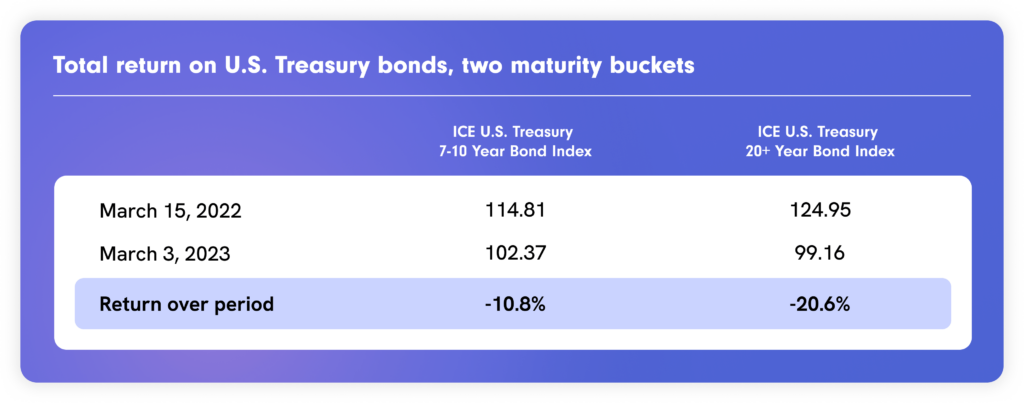

Inflation can be particularly tough on bond investors, and we have seen this since the Federal Reserve began monetary policy tightening in March 2022. Since the Fed started raising the Federal Funds rate from effectively zero on March 16, 2022, total returns on U.S. Treasuries1 (USTs) have been negative, even when taking into consideration the recent and sudden decline in yields due to a flight-to-quality related to recent difficulties at some banks.

Bond investors have been unable to successfully predict either the potential terminal rate and timing as to when the Fed might pivot. As a result, investors in intermediate- and long-term USTs continue to suffer as yields head higher.

Further, in an unexpected consequence, it appears that the inability to correctly ‘predict’ the direction of UST yields contributed to deposit flight at several prominent U.S. banks. This caused bank failures and added risk to the bank market, further complicating the Fed’s task of reining in inflation.

Inflation and Stocks

Equities (stocks), the other traditional asset class, are often considered to offer a hedge against inflation. This is only partially true:

- Companies with dominant market positions and pricing power can usually increase the prices of their goods or services to offset rising costs without eroding their operating margins and decreasing their bottom line. However, companies operating on thinner margins in highly competitive businesses generally do not have this luxury, because price increases can result in lost revenue to lower-cost providers or shrinking operating margins.

- Stocks of companies with lofty valuations based on robust expected future earnings growth – many of which might be unprofitable today – have been under severe pressure as the rate used to discount (or present value) future cash flows has increased. This phenomenon has had a significant effect on emerging technology companies over the last two years – many have seen their market value fall by 50 – 75% or even more over this period.

The impact of inflation can differ from stock to stock, with perhaps only a minority of companies having the characteristics to successfully defend their margins and valuations against rising prices.

Inflation and Alternative Assets Like Private Credit

As a rather dismal year for stocks and bonds drew to a close in 2022, the hope was that 2023 would offer a more certain trajectory as far as inflation and that the Fed’s future policy actions would be more predictable. Instead, we are in unexpected territory with continued inflation and upheaval among certain banks.

The negative effect of stubbornly high inflation on investors’ portfolios has been much-discussed over the last year or so given the poor, relatively volatile, performance of traditional asset classes. Specifically, resurgent inflation has placed the traditional stock-bond portfolio mix under increasing scrutiny, causing many investors to consider adding less-correlated assets into the mix.

Within the universe of alternative investments, private credit assets may offer significant benefits to a portfolio. Often, these assets:

- Are shorter duration, potentially reducing price volatility due to interest rate fluctuations and lessening the risk of an adverse credit event during the tenor of the transaction, given the limited holding period.

- Are often secured, providing some downside credit protection and a more attractive risk-return profile.

- Can be less correlated with traditional asset classes like stocks and bonds, improving portfolio diversification and the prospect for returns.

In brief, 2022 was a poor year for traditional asset classes, and 2023 is proving difficult for different reasons. For investors seeking diversification and less correlated returns, alternatives such as private credit may help to provide opportunity in uncertain markets.

1Indices used include the ICE U.S. Treasury 7-10 Year Bond Index and the U.S. Treasury 20 Year+ Bond Index for March